PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044160

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044160

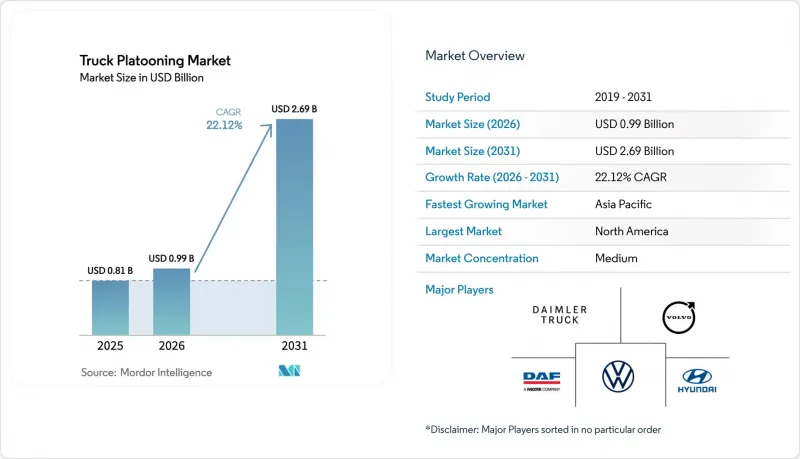

Truck Platooning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The truck platooning market size was valued at USD 0.81 billion in 2025 and estimated to grow from USD 0.99 billion in 2026 to reach USD 2.69 billion by 2031, at a CAGR of 22.12% during the forecast period (2026-2031).

Fleet operators are accelerating deployment because regulatory penalties on greenhouse-gas (GHG) emissions now exceed the payback period for the aerodynamic fuel savings that platooning delivers. With the roll-out of fifth-generation C-V2X along United States interstates, Europe's TEN-T corridors, and China's Beijing-Shanghai expressway, latency constraints have been eliminated. This advancement facilitates vehicle-to-vehicle signaling in minimal time and with tighter following gaps, significantly boosting fuel economy. Concurrently, original-equipment manufacturers (OEMs) are transitioning to subscription pricing. This shift transforms capital expenditures into operating costs, thereby attracting mid-sized carriers - typically operating a moderate number of tractors - into the potential customer fold. Shippers are further bolstering adoption by incorporating platooning clauses in long-term freight contracts. This strategy not only ensures verifiable Scope-3 emission reductions but also redefines platooning from a mere cost-saving tool to a crucial revenue-protection measure.

Global Truck Platooning Market Trends and Insights

Stringent Global GHG Mandates and Fuel-Economy Standards

Heavy-duty emission rules are toughening faster than typical replacement cycles, forcing carriers to search for near-term compliance tools. The European Union requires a 45% reduction in truck CO2 by 2030 relative to 2019 baselines, with non-compliance fines per required kilometer . California's Advanced Clean Fleets rule obliges high-priority carriers to make a significant share of new Class 8 purchases zero- or near-zero-emission from 2027. China's Stage VI standards, effective since July 2024, impose stricter nitrogen-oxide limits, magnifying the economic benefit of the fuel savings typical of tight-gap convoys. Penalty frameworks now make platooning not merely an efficiency upgrade but a regulatory hedge.

Commercial Launch of 5G-C-V2X Enabling Sub-50 ms Latency

Standalone 5G cores now blanket the bulk of United States interstates, achieving end-to-end network latencies below 30 milliseconds and enabling safe inter-vehicle gaps of 10-15 meters at highway speeds. China Mobile's 5G-Advanced build-out on the Beijing-Shanghai corridor supports synchronized braking across five-truck platoons. Release 17 of the 3GPP standard introduced direct sidelink, letting trucks maintain cohesion even in rural coverage gaps . Semiconductor volume shipments confirm scale: NXP delivered a significant volume of C-V2X chipsets in 2025, a notable jump year-on-year.

Freight-Cycle Downturn Curbing Cap-Ex by For-Hire Fleets

In 2025, freight rates and volumes significantly declined, reducing the discretionary cash that for-hire fleets typically allocate for technology upgrades. United States truckload spot rates dropped below the break-even point for numerous carriers, forcing many to divert limited funds towards servicing debts rather than investing in platooning retrofits. In Europe, road-freight tonnage experienced a year-over-year decline in Q3 2025, marking the fourth consecutive quarterly drop. This trend further diminished revenues and postponed equipment orders. Capital expenditures among for-hire carriers decreased in 2025, as high financing costs made the math for new-technology paybacks less appealing. An overcapacity issue exacerbated the situation, with the United States truck-to-load ratio becoming imbalanced. This imbalance not only depressed asset utilization but also extended payback periods for platooning hardware.

Other drivers and restraints analyzed in the detailed report include:

- Government-Funded Multi-State/Trans-EU Pilot Corridors

- Rising Diesel Prices Widening ROI Gap vs. Conventional Convoys

- High Retrofit and Sensor-Suite Cost per Truck

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, driver-assistive configurations are expected to dominate the truck platooning market with a significant 62.15% share, highlighting regulators' preference for Level 2 systems that ensure human oversight remains integral to operations. This dominance reflects the comfort of regulatory bodies with systems that keep drivers actively involved, maintaining a balance between technological advancement and safety. At the same time, autonomous platooning is anticipated to grow at a strong 23.54% CAGR as lawmakers work on drafting comprehensive Level 4 highway regulations and as insurance frameworks become more sophisticated. If the current adoption trends continue, the market size for autonomous truck platooning is likely to experience substantial growth by 2031, driven by advancements in technology and supportive regulatory developments.

At present, fleets predominantly opt for driver-assistive platoons, as these systems ensure that drivers remain responsible for vehicle operations. This approach aligns well with existing commercial-license regulations, making it easier for insurers to underwrite policies for such systems. However, as cross-border liability agreements are finalized and become more standardized, the adoption of autonomous operations is expected to accelerate. Autonomous systems offer significant advantages, including superior fuel savings and enhanced labor efficiencies, which are likely to drive their increasing market share in truck platooning steadily throughout the forecast period.

Adaptive cruise control, which accounts for 33.25% of 2025 revenues, has established itself as the foundational layer for every commercially deployed platoon. Insurance underwriters are increasingly advocating for redundant braking systems in fleets, which is driving active brake assist to achieve a robust forecast CAGR of 26.11%. This trend is further reinforced by the European Union's mandate requiring automated emergency braking systems in all new trucks, set to take effect in November 2024, ensuring widespread adoption across the region.

OEMs are progressively integrating sensor-fusion architectures into their factory builds to enhance vehicle safety and performance. These architectures combine radar's long-range detection capabilities, lidar's high precision, and the advanced object classification features of cameras. While these systems introduce incremental production costs, they significantly lower accident probabilities, emphasizing the industry's growing focus on leveraging scale advantages to improve safety and operational efficiency.

In 2025, vehicle-to-vehicle links generated 50.13% of total revenue, primarily due to their ability to operate without relying on fixed roadside assets. This capability allows fleets to form ad-hoc platoons whenever compatible trucks converge, offering significant flexibility and cost efficiency. The absence of infrastructure dependency makes this connectivity model particularly appealing for fleet operators aiming to optimize operations in dynamic environments. Meanwhile, vehicle-to-infrastructure connectivity is projected to grow at a strong 22.87% CAGR, driven by substantial federal investments in roadside-unit deployments across the United States and major freight corridors in the European Union. This growth underscores the increasing emphasis on infrastructure enhancements to support advanced connectivity solutions.

Highway agencies are actively adopting V2I technology as a strategic tool to improve lane utilization, reduce congestion, and collect detailed freight data for better decision-making. Additionally, converged chipsets like NXP's RoadLINK, which integrate both vehicle-to-vehicle and vehicle-to-infrastructure protocols, are minimizing hardware differentiation. These chipsets also enable software updates, allowing the introduction of new services and functionalities, further enhancing the value proposition of connected vehicle technologies.

The Truck Platooning Market Report is Segmented by Platooning Type (Driver-Assistive Truck Platooning and Autonomous Truck Platooning), Technology Type (Adaptive Cruise Control, and More), Infrastructure Connectivity (Vehicle-To-Vehicle (V2V), and More), Truck Class (Class 8 and More), Fleet Type (Private and More), Application, Ownership/Business Model, and Geography. Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounts for 43.15% of the 2025 revenue, driven by a well-connected interstate network, extensive 5G coverage, and supportive federal grants. Yet state-level rule divergence still forces carriers to alter platoon configurations, trimming efficiency when crossing borders between California, Arizona, and Texas. Annual adoption, nevertheless, is set to quicken as the Infrastructure Investment and Jobs Act funds more connected-vehicle projects.

Europe ranked second, underpinned by stringent CO2 caps and the TEN-T modernization program, but cross-border liability gaps and economic stagnation in Germany moderate near-term expansion. Harmonized UNECE regulations under discussion could unlock multi-country platoons, erasing current fragmentation penalties.

Asia-Pacific shows the fastest trajectory at 25.56% CAGR, propelled by China's freight-digitization roadmap that mandates Level 2 automation on a significant share of new trucks sold from 2026. Japan's Society 5.0 program offers a notable share of toll rebates for certified platoons, while India's Golden Quadrilateral upgrade earmarks high costs for V2I pilots. Remaining infrastructure gaps and regulatory inconsistencies mean ramp-up will vary by nation, but upside potential is significant.

- Daimler Truck AG

- AB Volvo

- Paccar Inc (DAF Trucks)

- Volkswagen Group

- Hyundai Motor Company

- Iveco Group

- ZF Friedrichshafen AG

- Continental AG

- Robert Bosch GmbH

- Knorr-Bremse AG

- NXP Semiconductors N.V.

- Einride AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Global GHG Mandates and Fuel-Economy Standards

- 4.2.2 Commercial Launch of 5G-C-V2X Enabling Sub-50 ms Latency

- 4.2.3 Government-Funded Multi-State/Trans-EU Pilot Corridors

- 4.2.4 Rising Diesel Prices Widening ROI Gap vs. Conventional Convoys

- 4.2.5 OEM Platooning-as-a-Service Subscription Models

- 4.2.6 Scope-3 Decarbonization Credits Demanded by Shippers

- 4.3 Market Restraints

- 4.3.1 Freight-Cycle Downturn Curbing Cap-Ex by For-Hire Fleets

- 4.3.2 High Retrofit and Sensor-Suite Cost per Truck

- 4.3.3 Cross-Border Liability and Data-Ownership Uncertainty

- 4.3.4 Cyber-Attack Exposure Driving Insurance Premium Spikes

- 4.4 Value/Supply-Chain Analysis

- 4.5 Technological Roadmap

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Platooning Type

- 5.1.1 Driver-Assistive Truck Platooning (DATP)

- 5.1.2 Autonomous Truck Platooning

- 5.2 By Technology Type

- 5.2.1 Adaptive Cruise Control

- 5.2.2 Forward Collision Warning

- 5.2.3 Automated Emergency Braking

- 5.2.4 Active Brake Assist

- 5.2.5 Lane Keep Assist

- 5.2.6 Other ADAS (Blind-Spot Warning, etc.)

- 5.3 By Infrastructure Connectivity

- 5.3.1 Vehicle-to-Vehicle (V2V)

- 5.3.2 Vehicle-to-Infrastructure (V2I)

- 5.3.3 Global Positioning System (GPS)

- 5.4 By Truck Class

- 5.4.1 Class 8 (Heavy-Duty)

- 5.4.2 Class 6-7 (Medium-Duty)

- 5.5 By Fleet Type

- 5.5.1 Private/Dedicated Fleets

- 5.5.2 For-Hire Common Carriers

- 5.6 By Application

- 5.6.1 Long-Haul Line-haul

- 5.6.2 Regional / Hub-to-Hub

- 5.6.3 Port and Intermodal Drayage

- 5.7 By Ownership / Business Model

- 5.7.1 OEM-Integrated Subscription

- 5.7.2 Third-Party Technology Provider

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Rest of North America

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 United Kingdom

- 5.8.3.3 France

- 5.8.3.4 Spain

- 5.8.3.5 Italy

- 5.8.3.6 Russia

- 5.8.3.7 Rest of Europe

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 Japan

- 5.8.4.3 India

- 5.8.4.4 South Korea

- 5.8.4.5 Rest of Asia-Pacific

- 5.8.5 Middle East and Africa

- 5.8.5.1 United Arab Emirates

- 5.8.5.2 Saudi Arabia

- 5.8.5.3 Egypt

- 5.8.5.4 Turkey

- 5.8.5.5 South Africa

- 5.8.5.6 Rest of the Middle East and Africa

- 5.8.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Daimler Truck AG

- 6.4.2 AB Volvo

- 6.4.3 Paccar Inc (DAF Trucks)

- 6.4.4 Volkswagen Group

- 6.4.5 Hyundai Motor Company

- 6.4.6 Iveco Group

- 6.4.7 ZF Friedrichshafen AG

- 6.4.8 Continental AG

- 6.4.9 Robert Bosch GmbH

- 6.4.10 Knorr-Bremse AG

- 6.4.11 NXP Semiconductors N.V.

- 6.4.12 Einride AB

7 Market Opportunities and Future Outlook