PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044164

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044164

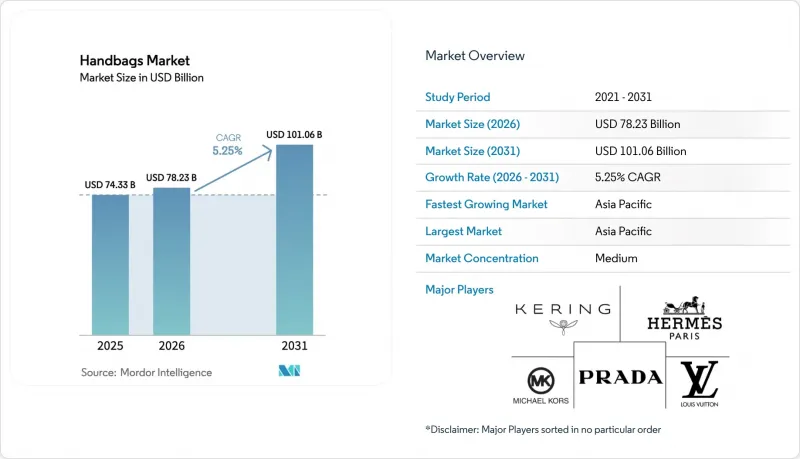

Handbags - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Handbags Market size was valued at USD 74.33 billion in 2025 and estimated to grow from USD 78.23 billion in 2026 to reach USD 101.06 billion by 2031, at a CAGR of 5.25% during the forecast period (2026 to 2031), confirming steady global demand and brand diversification.

The trajectory suggests pricing power has plateaued, prompting brands to shift their focus to volume growth, experiential selling, and material innovation to maintain margins. Totes remain the anchor product, social commerce accelerates discovery, and regulatory pressure on materials nudges companies toward bio-fabricated leather and a circular economy. Cross-border purchasing, particularly by Chinese travelers, creates geographic arbitrage that influences inventory allocation, while the resale channel compresses primary-market pricing and highlights provenance. Competitive intensity is rising as direct-to-consumer entrants leverage influencer marketing and agile supply chains to capture market share in the handbags market.

Global Handbags Market Trends and Insights

Increase in outstation and leisure travel

The growing popularity of outstation and leisure travel is significantly boosting the demand for handbags, particularly those that are travel-friendly and stylish. According to the World Travel and Tourism Council (WTTC), in 2024, the Travel and Tourism sector contributed 10% to the global economy, amounting to USD 10.9 trillion. The WTTC forecasts that by 2035, tourism will inject USD 16.5 trillion into the global economy, accounting for 11.5% of global GDP. This increase in tourism, supported by relaxed travel restrictions and the availability of budget airlines, is encouraging consumers to invest in luggage and leather goods, including handbags, for weekend getaways and vacations. To meet travelers' needs, brands are introducing innovative products. For example, Dagne Dover launched its Petra Convertible Tote, a sleek hybrid tote-backpack featuring a padded laptop compartment, trolley sleeve, and multiple organizational pockets designed specifically for professionals who balance travel and work demands.

Rising female workforce participation

As more women enter the workforce, the demand for handbags that are both stylish and functional is increasing. Women now seek bags that can carry essentials like laptops, documents, and personal items while complementing their professional attire. According to the World Bank, the global female labor force participation rate reached 40.2% in 2024, reflecting this growing trend . Office-friendly handbags, such as structured totes, satchels, and laptop-compatible crossbody bags, are becoming more popular because they combine practicality with fashion. To cater to these needs, brands are designing bags with features like multiple compartments for better organization and convenience. For example, Michael Kors launched the Jet Set Travel Large Logo Tote in 2024, which offers a spacious and organized interior, making it ideal for working women. This shift shows how handbags are no longer just fashion statements but have become essential tools for modern working women, balancing style and functionality to meet their daily needs.

Counterfeit proliferation and brand dilution

Counterfeit handbags not only flood the market but also undermine brand equity, compromise pricing integrity, and erode consumer trust. In 2024, U.S. Customs and Border Protection seized over USD 380 million worth of counterfeit handbags, wallets, and accessories, underscoring the prominence of the category in intellectual property violations. Online marketplaces have become the primary distribution channel for these counterfeits. Yet, algorithmic detection struggles against astute sellers who rotate listings, use obfuscated brand names, and exploit cross-border shipping loopholes. The emergence of high-quality "superfakes" that closely mimic stitching, hardware, and even serial numbers has made authentication challenging for consumers. This difficulty has led some buyers to authorized resale platforms like The RealReal and Vestiaire Collective, which offer third-party verification. As the market becomes saturated with counterfeits, the aspirational value of owning an authentic item diminishes, resulting in brand dilution. In response, brands are adopting advanced anti-counterfeiting technologies, such as blockchain-based provenance tracking, Near Field Communication (NFC)-embedded tags, and forensic-grade material markers.

Other drivers and restraints analyzed in the detailed report include:

- Changing fashion trends and consumer preferences

- Product innovation and sustainability trends

- Regulatory hurdles and compliance issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, tote bags held a 41.21% market share, reflecting their versatility across work, travel, and everyday use. Bucket bags are projected to grow at a 5.49% rate through 2031, driven by demand for hands-free, minimalist designs favored by younger consumers. While satchels retain a niche following, their growth has stalled amid the shift to hybrid work, leading to reduced demand for structured, office-centric styles. Clutches continue to lose relevance as social settings become more casual, whereas niche formats such as hobo, saddle, and belt bags remain trend-driven, with belt bags seeing renewed momentum in 2024-2025 due to their integration into athleisure and festival wear.

In the men's segment, leather shoulder bags and weekender styles are gaining traction as functional alternatives to traditional briefcases, while nylon bags are being replaced by more durable and resale-friendly materials, such as leather and canvas. From a pricing perspective, totes priced between USD 250 and USD 500 led unit sales in 2024, while volumes softened for bags above USD 1,000, indicating growing price sensitivity. Brands are responding by offering entry-level totes with simplified designs to preserve volume, while limiting exotic materials and limited editions to ultra-high-net-worth consumers.

The mass segment accounted for 63.57% of market share in 2025; however, the premium category is projected to expand at a CAGR of 5.91% through 2031, signaling a strategic shift by brands toward protecting margins rather than pursuing volume growth. Mass-market handbags, typically priced below USD 250, cater to entry-level consumers and fast-fashion shoppers who value affordability and rapid trend turnover. Despite its scale, this segment faces increasing margin pressure from rising production costs, heightened promotional activity, and competition from resale platforms that offer lightly used premium bags at comparable price points. Premium handbags, generally priced between USD 500 and USD 2,000, occupy a strategic middle ground where brand heritage, superior materials, and craftsmanship support price premiums without the deterrent effect associated with ultra-luxury pricing. Brands such as Coach, Michael Kors, and Kate Spade have refined their product and distribution strategies by limiting outlet exposure and prioritizing full-price sell-through, acknowledging that persistent discounting weakens brand equity and conditions consumers to delay purchases.

The premium segment also benefits from a resale-driven halo effect, as strong secondary-market liquidity reinforces perceived value and lowers the entry barrier for first-time luxury buyers. Meanwhile, the mass segment's durability depends on capturing impulse purchases, gifting occasions, and replacement demand, areas increasingly challenged by direct-to-consumer brands that exploit social commerce and influencer-led marketing to avoid traditional wholesale margins. To reinforce value propositions, premium brands are investing in experiential retail formats such as pop-ups, trunk shows, and customization services, strengthening customer engagement beyond simple transactions. This segmentation also mirrors regional consumption patterns: North America favors accessible luxury, with most handbag units priced between USD 250 and USD 500, while Asia-Pacific demonstrates stronger demand for entry-level offerings, particularly handbags priced below USD 250.

The Handbags Market Report is Segmented by Product Type (Satchel, Bucket Bag, Clutch, and More), Category (Mass and Premium), End User (Women and Men), Distribution Channel (Offline Retail Stores and Online Retail Stores), and Geography (North America, Europe, Asia-Pacific, South America, and the Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 43.06% of the global market in 2025 and is expected to grow at a 6.23% CAGR through 2031, though performance varies significantly across the region. China's luxury market contracted 18%-20% in 2024, with LVMH's fashion and leather goods division posting a 5% organic revenue decline in Q3 amid property-sector challenges and rising youth unemployment. In contrast, India is experiencing rapid expansion, driven by urbanization, increasing female workforce participation, and growth in organized retail. Japan continues to benefit from inbound tourism, while Southeast Asia's rising middle class is fueling demand despite infrastructure limitations and regulatory complexities.

North America remains a key profit center due to high per-capita spending and a mature e-commerce ecosystem. US apparel and accessories e-commerce reached USD 134.5 billion in 2024 and is projected to grow to USD 219.3 billion by 2029, with handbags performing particularly well due to standardized sizing and lower return rates (US Census Bureau). Buy-now-pay-later solutions have increased average transaction values, while the USD 250-500 price range captured the majority of handbag unit sales in 2024. Canada and Mexico provide additional volume, with Mexico benefiting from nearshoring trends, and the robust US resale market pressures primary sales, prompting brands to emphasize exclusivity, personalization, and post-purchase services.

Europe, the Middle East, South America, and Africa present a diverse set of opportunities. Europe faces structural challenges, with luxury conglomerates losing USD 240 billion in market capitalization since March 2024, although imports and exports remain strong (European Commission), and ultra-luxury brands such as Hermes continue to perform well through controlled distribution. The Middle East, led by the UAE and Saudi Arabia, is a high-margin growth market, with the GCC luxury sector projected to reach USD 15 billion by 2027 (Chalhoub Group), supported by high-net-worth inflows and tourism. South America faces volatility and elevated import costs, while Africa, particularly South Africa, represents an emerging but fast-growing market, with handbag e-commerce showing strong potential.

- LVMH Moet Hennessy Louis Vuitton SE

- Kering SA

- Tapestry Inc.

- Michael Kors, L.L.C.

- Hermes International SA

- Chanel SA

- Prada SpA

- Burberry Group PLC

- Longchamp SAS

- Mulberry Group PLC

- Tory Burch LLC

- Braun Buffel GmbH & Co. KG

- Salvatore Ferragamo S.p.A

- PVH Corp.

- Furla SpA

- Charles & Keith Group

- Dagne Dover Inc.

- Maison Goyard

- MCM Worldwide

- VF Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase in outstation and leisure travel

- 4.2.2 Rising female workforce and purchasing power

- 4.2.3 Changing fashion trends and consumer preferences

- 4.2.4 Product innovation and sustainability trends

- 4.2.5 Social-media and influencer-led brand discovery

- 4.2.6 Product innovation in terms of raw material and design

- 4.3 Market Restraints

- 4.3.1 Counterfeit proliferation and brand dilution

- 4.3.2 Regulatory hurdles and compliance issues

- 4.3.3 Environmental concerns regarding materials

- 4.3.4 Volatile hide prices and supply shocks

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Satchel

- 5.1.2 Bucket Bag

- 5.1.3 Clutch

- 5.1.4 Tote Bag

- 5.1.5 Other Product Types

- 5.2 By Category

- 5.2.1 Mass

- 5.2.2 Premium

- 5.3 By End User

- 5.3.1 Women

- 5.3.2 Men

- 5.4 By Distribution Channel

- 5.4.1 Offline Retail Stores

- 5.4.2 Online Retail Stores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Positioning Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 LVMH Moet Hennessy Louis Vuitton SE

- 6.4.2 Kering SA

- 6.4.3 Tapestry Inc.

- 6.4.4 Michael Kors, L.L.C.

- 6.4.5 Hermes International SA

- 6.4.6 Chanel SA

- 6.4.7 Prada SpA

- 6.4.8 Burberry Group PLC

- 6.4.9 Longchamp SAS

- 6.4.10 Mulberry Group PLC

- 6.4.11 Tory Burch LLC

- 6.4.12 Braun Buffel GmbH & Co. KG

- 6.4.13 Salvatore Ferragamo S.p.A

- 6.4.14 PVH Corp.

- 6.4.15 Furla SpA

- 6.4.16 Charles & Keith Group

- 6.4.17 Dagne Dover Inc.

- 6.4.18 Maison Goyard

- 6.4.19 MCM Worldwide

- 6.4.20 VF Corporation

7 MARKET OPPORTUNITIES AND FUTURE TRENDS