PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044166

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044166

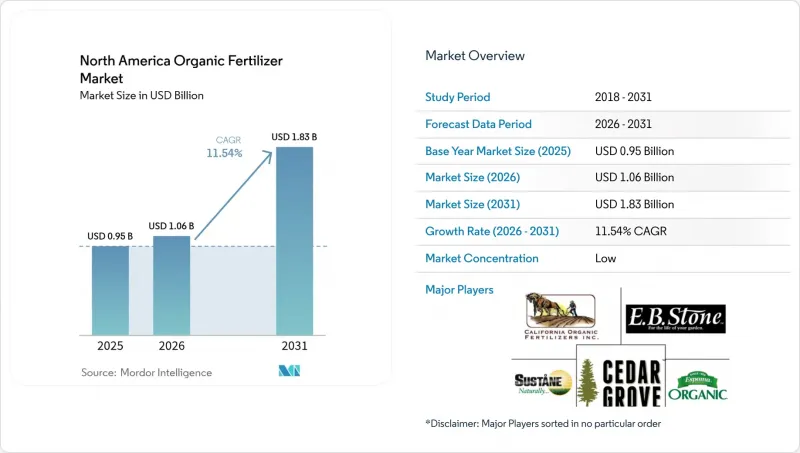

North America Organic Fertilizer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The North America organic fertilizer market size is expected to grow from USD 0.95 billion in 2025 to USD 1.06 billion in 2026 and is forecast to reach USD 1.83 billion by 2031 at 11.54% CAGR over 2026-2031.

Growth is fueled by expanding certified organic acreage, wider use of precision-ag liquid applicators, and federal carbon-credit programs that reward manure conversion projects. Rapid scale-up of controlled-environment farms, local food-waste digestate mandates, and the launch of biopolymer-coated granules that pair humic acids with algae extracts are further improving nutrient-use efficiency and driving uptake. Investments from both government grants and private capital shorten payback periods for new composting and bio-processing facilities, which strengthens regional supply chains and keeps freight costs contained. These converging factors sustain a robust demand outlook for the North America organic fertilizer market through the decade.

North America Organic Fertilizer Market Trends and Insights

Expanding Certified Organic Acreage

Certified organic farmland keeps growing as farmers switch from synthetics to inputs approved under the United States Department of Agriculture National Organic Program. California leads with more than 2.13 million certified acres that generated USD 14.0 billion in organic sales during 2024. Mexico now counts 48,874 certified operators spanning all 32 states and benefits from an equivalence agreement with Canada that remains in force until 2027. Every new acre needs Organic Materials Review Institute-listed nutrients, and that requirement funnels predictable demand toward North America organic fertilizer market suppliers. Structured standards also shield compliant producers from lower-grade imports, supporting premium pricing.

Precision-ag Liquid Application Systems Boost Adoption of Low-viscosity Organics

Variable-rate sprayers, satellite guidance, and cloud-based decision tools are used on more than 60% of North American row-crop acres. These platforms work best with low-viscosity organic liquids that move through nozzles without clogging. Real-time soil testing data guide exact placement, which raises nutrient-use efficiency and lowers cost per harvested acre. Because the equipment is already on farms, growers can switch to compatible organics without large capital outlays, accelerating usage within the North America organic fertilizer market.

Inconsistent Nutrient Analysis Across Batches

Organic fertilizers often show variable nitrogen, phosphorus, and potassium content because feedstock composition changes with season and processing method. This inconsistency complicates precision application, slows regulatory approvals, and forces extra laboratory tests that small producers cannot always afford. Without harmonized quality metrics across federal and state lines, manufacturers face fragmented compliance requirements that delay product launches and limit scalable growth for the North America organic fertilizer market.

Other drivers and restraints analyzed in the detailed report include:

- USDA Carbon-credit Pilots Rewarding Manure-to-fertilizer Projects

- Biopolymer-Coated Granules Integrating Humic Acids with Algae Extracts Boost Nutrient Uptake Efficiency

- Short Shelf-life for High-moisture Liquids in Warmer States

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Meal-based products captured 48.50% of total sales in 2025, the largest slice of the North America organic fertilizer market share, because steam-sterilized ingredients yield predictable nutrient profiles that pass regulatory audits. Processing removes pathogens and extends shelf life, giving distributors confidence in inventory planning. Manufacturers blend soybean meal, bone meal, and feather meal to customize nitrogen release curves that align with precision agriculture prescriptions. Manure-based fertilizers are growing fastest at a 11.76% CAGR as municipal digestate rules and on-farm composting projects deliver steady feedstock streams. Technology investments such as forced-air static piles and biochar inoculation minimize odor and speed maturation, closing the quality gap with meals. Emerging sub-categories like biochar-enhanced pellets and micro-algae powders find niche demand among high-value horticulture operators looking for carbon-rich amendments. Innovations across the form segment make it a central battleground for suppliers aiming to raise share in the North America organic fertilizer market.

The North America organic fertilizer market value for meal-based products is expected to grow steadily through 2031, highlighting the segment's increasing importance in row-crop rotations, where reliability and consistency are prioritized over nutrient density. Producers highlight audit-ready formulations that lower documentation burdens under organic certification. In parallel, manure-based lines ride cost advantages where local livestock waste offers negative feedstock costs and carbon-credit upside. Oilcakes, led by neem and castor seed products, maintain niche status for specialty fruit and nut crops because slow nitrogen release matches long growing cycles. Processors continue to expand capacity as CalRecycle grants unlock USD 130 million for feedstock-to-fertilizer infrastructure in California, adding to total supply available to the North America organic fertilizer market.

The North America Organic Fertilizer Market Report is Segmented by Form (Manure, Meal-Based Fertilizers, and Oilcakes), Crop Type (Cash Crops, Horticultural Crops, and Row Crops), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

List of Companies Covered in this Report:

- Sustane Natural Fertilizer Inc.

- The Espoma Company

- Scotts Miracle-Gro Company

- BioFert Manufacturing Inc.

- California Organic Fertilizers Inc.

- Cascade Agronomics LLC

- Cedar Grove Composting Inc.

- E.B. Stone and Sons Inc.

- Morgan Composting Inc.

- True Organic Products Inc.

- Nutrien Ag Solutions (Nutrien Ltd.)

- Midwestern BioAg

- Nature Safe (Darling Ingredients Inc.)

- EnviroKure Inc.

- Pacific Biochar Benefit Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

- 1.3 Research Methodology

2 REPORT OFFERS

3 EXECUTIVE SUMMARY AND KEY FINDINGS

4 KEY INDUSTRY TRENDS

- 4.1 Area Under Organic Cultivation

- 4.2 Per Capita Spending On Organic Products

- 4.3 Regulatory Framework

- 4.3.1 Canada

- 4.3.2 Mexico

- 4.3.3 United States

- 4.4 Value Chain and Distribution Channel Analysis

- 4.5 Market Drivers

- 4.5.1 Expanding certified organic acreage

- 4.5.2 Precision-ag liquid application systems boost adoption of low-viscosity organics

- 4.5.3 USDA carbon-credit pilots rewarding manure-to-fertilizer projects

- 4.5.4 Rapid scale-up of controlled-environment agriculture (CEA) in the U.S. and Canada

- 4.5.5 Municipal food-waste digestate mandates create local supply pools

- 4.5.6 Biopolymer-coated granules integrating humic acids with algae extracts boost nutrient uptake efficiency

- 4.6 Market Restraints

- 4.6.1 Inconsistent nutrient analysis across batches

- 4.6.2 Short shelf-life for high-moisture liquids in warmer states

- 4.6.3 Slow-release profile mismatched to short-season row crops

- 4.6.4 Persistent heavy-metal limits in some recycled waste streams

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Form

- 5.1.1 Manure

- 5.1.2 Meal Based Fertilizers

- 5.1.3 Oilcakes

- 5.1.4 Other Organic Fertilizer

- 5.2 Crop Type

- 5.2.1 Cash Crops

- 5.2.2 Horticultural Crops

- 5.2.3 Row Crops

- 5.3 Country

- 5.3.1 Canada

- 5.3.2 Mexico

- 5.3.3 United States

- 5.3.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Sustane Natural Fertilizer Inc.

- 6.4.2 The Espoma Company

- 6.4.3 Scotts Miracle-Gro Company

- 6.4.4 BioFert Manufacturing Inc.

- 6.4.5 California Organic Fertilizers Inc.

- 6.4.6 Cascade Agronomics LLC

- 6.4.7 Cedar Grove Composting Inc.

- 6.4.8 E.B. Stone and Sons Inc.

- 6.4.9 Morgan Composting Inc.

- 6.4.10 True Organic Products Inc.

- 6.4.11 Nutrien Ag Solutions (Nutrien Ltd.)

- 6.4.12 Midwestern BioAg

- 6.4.13 Nature Safe (Darling Ingredients Inc.)

- 6.4.14 EnviroKure Inc.

- 6.4.15 Pacific Biochar Benefit Corporation

7 KEY STRATEGIC QUESTIONS FOR AGRICULTURAL BIOLOGICALS CEOS