PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044168

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044168

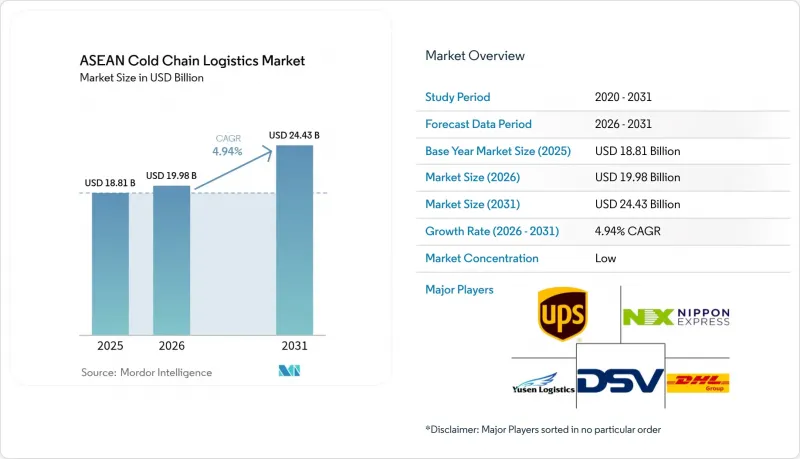

ASEAN Cold Chain Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The ASEAN Cold Chain Logistics Market size is projected to expand from USD 18.81 billion in 2025 and USD 19.98 billion in 2026 to USD 24.43 billion by 2031, registering a CAGR of 4.94% between 2026 to 2031.

The ASEAN cold chain logistics market is gradually strengthening as regional food supply chains become more organized and export-oriented. Countries with strong seafood, meat, and tropical fruit production, such as Thailand, Vietnam, and Indonesia, are increasing investments in refrigerated storage and temperature-controlled transportation to reduce post-harvest losses and support exports. At the same time, the expansion of modern retail, quick-commerce grocery platforms, and pharmaceutical distribution is pushing demand for more reliable cold chain infrastructure across the region. However, the market remains uneven, with developed hubs like Singapore having advanced logistics capabilities while several emerging ASEAN economies still face gaps in cold storage capacity and distribution networks. As a result, logistics companies are focusing on building regional cold storage hubs, improving monitoring technologies, and strengthening cross-border supply chains to capture growing demand.

ASEAN Cold Chain Logistics Market Trends and Insights

Growing Middle-Class Disposable Income Driving Demand for Imported Frozen and Chilled Goods

Rising incomes in large ASEAN economies are driving demand for imported proteins, premium dairy, and ready-to-cook formats requiring reliable frozen and chilled transport. Urban retailers are increasing temperature-sensitive assortments to meet higher demand for freshness and quality. In Muslim-majority markets, halal-certified frozen meals and processed foods necessitate segregated storage and compliance with halal logistics rules, boosting demand for certified providers. Seasonal disruptions, like storm seasons in the Philippines, highlight the need for stockpiles and reliable distribution routes. These trends are fueling growth in the ASEAN cold chain logistics market as buyers prioritize custody control for sensitive cargo.

Modern Retail and Supermarket Chain Expansion Across Tier-2 and Tier-3 Cities

Convenience and grocery chains are scaling beyond capitals into secondary cities, which creates distributed demand for short-haul chilled replenishment and micro-fulfillment. E-Mart24's 2026 plan to open 130 stores in Malaysia, Cambodia, and Laos introduces 24-hour formats that require consistent 2-8°C storage and delivery routines for beverages and ready meals. Indonesia's Alfamart is extending its footprint across secondary islands, which deepens route density for chilled fleets serving towns that previously relied on ambient stock. Retailers are bringing in remote temperature monitoring and exception alerts for cold cases, which tightens coordination between stores and upstream distribution and raises expectations for data visibility from carriers and warehouses. This buildout shifts the ASEAN cold chain logistics market toward modular cross-docks, right-sized cold rooms, and flexible trucking. Providers that can scale smaller nodes and adjust routing quickly are gaining an edge over operators concentrated in large centralized sites.

Regulatory Inconsistencies and Varying Cold Chain Standards Across Member States

Halal and pharmaceutical regulations vary by country, complicating facility design, staff training, and cross-border documentation. Indonesia's Regulation 42/2024 mandates halal-only cold rooms and dedicated handling flows, increasing costs for certified sites. Malaysia's MS 2400 standard requires segregation across logistics zones, raising configuration and audit demands. Singapore's HSA GDP rules enforce validated equipment and chain-of-custody for pharmaceutical logistics, unlike some neighboring markets. These differences increase onboarding costs and risk shipment delays due to misaligned paperwork. Large integrators with centralized compliance programs adapt faster, influencing market share in the ASEAN cold chain logistics market.

Other drivers and restraints analyzed in the detailed report include:

- FDI Inflows in Greenfield Cold Storage and Distribution Center Development

- Government Food Security Programs Mandating Post-Harvest Cold Storage Capacity

- High Upfront Capital Expenditure Deterring SME Cold Chain Operators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerated storage commands 49.3% share in 2025, while value-added services are growing fastest at 5.7% CAGR as brand owners outsource blast-freezing, repackaging, GDP-compliant labeling, and validated packing for life-sciences loads. Within the ASEAN cold chain logistics market size context, pharma-focused nodes with -80°C capacity and digitized custody are expanding as operators build GDP-ready environments for clinical-trial materials and biologics. UPS doubled Singapore capacity in June 2025, adding ultra-low freezers and visibility features that help healthcare shippers meet audit requirements and timing constraints. Road remains the primary mode for intra-country logistics and uses GPS-linked telemetry for exception handling and route optimization in sensitive lanes. Maritime networks continue to scale inter-island connectivity for frozen foods, and regional carriers have signaled reefer expansion to serve domestic and export flows. Airfreight supports time-bound biologics and high-care shipments, where transit integrity and chain-of-custody records define provider choice.

Public warehousing dominates, where importers and distributors prefer scalable, asset-light access rather than private investment that may be exposed to regulatory change. Private cold rooms remain critical for vertically integrated processors that prioritize control of inventory turns, blending, and export readiness. Thailand's new multi-temperature warehouse commissioned near Bangkok in December 2024 highlights a build pattern that supports e-commerce and retail consolidation as store networks expand. In pharmaceuticals, GDP rules steer flows toward audited facilities and handling zones with validated equipment, which supports premium service differentiation. As energy resilience and monitoring become standard, service expectations are rising across the ASEAN cold chain logistics market, and providers are using compliance status to signal capability. The ASEAN cold chain logistics industry is therefore shifting toward higher service baselines supported by documentation and technology adoption.

The ASEAN Cold Chain Logistics Market is Segmented by Service Type (Refrigerated Storage, Transportation, and Value-Added Services), by Temperature (Chilled, Frozen, Ambient, and Deep-Frozen), by Application (Fruits and Vegetables, Meat and Poultry, Fish and Seafood and More), and by Geography (Singapore, Thailand, Vietnam, Indonesia, Malaysia, Philippines, and Rest of ASEAN). Forecasts are in Value (USD).

List of Companies Covered in this Report:

- Deutsche Post DHL

- Nippon Express

- United Parcel Service (UPS)

- Yusen Logistics (Part of NYK Line)

- DSV

- Yamato Transport

- JWD Logistics

- Royal Cargo

- KOSPA Logistics

- PT Wahana Cold Storage

- Thai Max Co. Ltd

- HAVI Logistics

- Lineage Logistics

- Kuehne + Nagel

- Nichirei Logistics

- Kerry Logistics

- AJ Total Vietnam

- YCH Group

- Linfox

- MGM Bosco Logistics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Middle-Class Disposable Income Driving Demand for Imported Frozen and Chilled Goods

- 4.2.2 Modern Retail and Supermarket Chain Expansion Across Tier-2 And Tier-3 Cities

- 4.2.3 FDI Inflows in Greenfield Cold Storage and Distribution Center Development

- 4.2.4 Government Food Security Programs Mandating Post-Harvest Cold Storage Capacity

- 4.2.5 Aquaculture Industry Boom in Vietnam, Thailand, and Indonesia Boosting Seafood Cold Logistics

- 4.2.6 Regional Free Trade Agreements (RCEP, CPTPP) are Facilitating Chilled Agri-Food Trade Flows

- 4.3 Market Restraints

- 4.3.1 Regulatory Inconsistencies and Varying Cold Chain Standards Across Member States

- 4.3.2 High Upfront Capital Expenditure Deterring SME Cold Chain Operators

- 4.3.3 Competition From Informal and Unregulated Cold Storage Providers is Undercutting Prices

- 4.3.4 Climate Vulnerability and Extreme Weather Disrupting Cold Chain Continuity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Emission Standards and Regulations

- 4.9 Insights into Refrigerants and Packaging Materials

- 4.10 Insights into Halal Standards and Certifications (ID and MY)

- 4.11 Insights into Ambient / Temperature-controlled Storage

- 4.12 Geopolitical Impact

5 Market Size and Growth Forecasts (Value)

- 5.1 By Service Type

- 5.1.1 Refrigerated Storage

- 5.1.1.1 Public Warehousing

- 5.1.1.2 Private Warehousing

- 5.1.2 Refrigerated Transportation

- 5.1.2.1 Road

- 5.1.2.2 Rail

- 5.1.2.3 Sea

- 5.1.2.4 Air

- 5.1.3 Value-Added Services

- 5.1.1 Refrigerated Storage

- 5.2 By Temperature Type

- 5.2.1 Chilled (0-5°C)

- 5.2.2 Frozen (-18-0°C)

- 5.2.3 Ambient

- 5.2.4 Deep-Frozen/Ultra-Low (less than-20°C)

- 5.3 By Application

- 5.3.1 Fruits and Vegetables

- 5.3.2 Meat and Poultry

- 5.3.3 Fish and Seafood

- 5.3.4 Dairy and Frozen Desserts

- 5.3.5 Bakery and Confectionery

- 5.3.6 Ready-to-Eat Meals

- 5.3.7 Pharmaceuticals and Biologics

- 5.3.8 Vaccines and Clinical Trial Materials

- 5.3.9 Chemicals and Specialty Materials

- 5.3.10 Other Perishables

- 5.4 By Geography

- 5.4.1 Singapore

- 5.4.2 Thailand

- 5.4.3 Vietnam

- 5.4.4 Indonesia

- 5.4.5 Malaysia

- 5.4.6 Philippines

- 5.4.7 Rest of ASEAN

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Deutsche Post DHL

- 6.4.2 Nippon Express

- 6.4.3 United Parcel Service (UPS)

- 6.4.4 Yusen Logistics (Part of NYK Line)

- 6.4.5 DSV

- 6.4.6 Yamato Transport

- 6.4.7 JWD Logistics

- 6.4.8 Royal Cargo

- 6.4.9 KOSPA Logistics

- 6.4.10 PT Wahana Cold Storage

- 6.4.11 Thai Max Co. Ltd

- 6.4.12 HAVI Logistics

- 6.4.13 Lineage Logistics

- 6.4.14 Kuehne + Nagel

- 6.4.15 Nichirei Logistics

- 6.4.16 Kerry Logistics

- 6.4.17 AJ Total Vietnam

- 6.4.18 YCH Group

- 6.4.19 Linfox

- 6.4.20 MGM Bosco Logistics

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment