PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044179

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044179

Multilayer Ceramic Capacitor (MLCC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

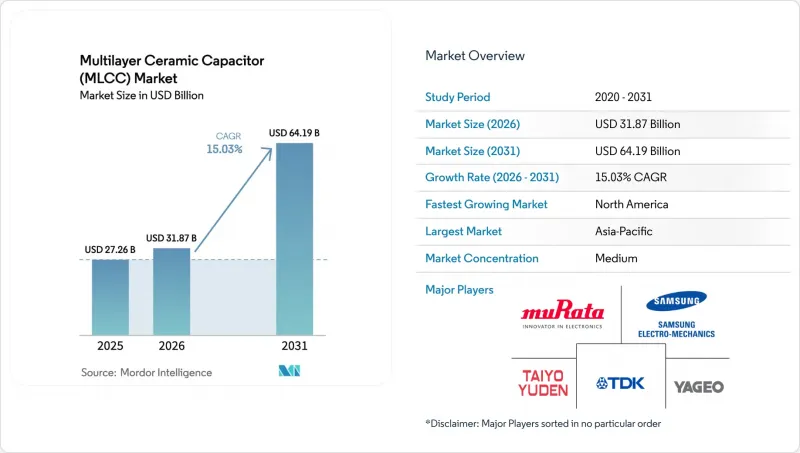

The multilayer ceramic capacitor (MLCC) market size is projected to expand from USD 27.26 billion in 2025 and USD 31.87 billion in 2026 to USD 64.19 billion by 2031, registering a 15.03% CAGR between 2026 and 2031. The growth trajectory reflects surging demand for passive components as vehicle electrification, artificial-intelligence infrastructure, and edge computing converge, placing sustained pressure on legacy supply chains. Class 1 temperature-stable dielectrics continue to gain traction in safety-critical designs, while 0402 packages are becoming the preferred form factor for high-performance servers that prize ultra-low equivalent series inductance over absolute footprint savings. Geo-diversified friend-shoring is unlocking incremental capacity in India and Southeast Asia, yet long qualification cycles for AEC-Q200 parts keep near-term supply tight. Competitive dynamics favor vertically integrated leaders that control barium-titanate powders and nickel electrode metallurgy, especially as volatility in nickel and palladium prices raises cost risk across the multilayer ceramic capacitor market.

Global Multilayer Ceramic Capacitor (MLCC) Market Trends and Insights

800 V EV Architectures Accelerate Demand for High-Voltage MLCCs

Automakers shifting to 800 V battery platforms need MLCCs that withstand >=1,000 V operating margins, prompting suppliers to thicken nickel-palladium electrodes and refine sub-micrometer dielectric deposition. Samsung Electro-Mechanics released a 2,000 V X7R family in 2025 for silicon-carbide inverters, while Murata's GCM32 series pairs 1,000 V ratings with 100 nH equivalent series inductance for noise suppression. IDTechEx expects 800 V vehicles to represent 40% of production by 2028, lifting MLCC content per car by roughly one-quarter. Qualification bottlenecks persist because automotive-grade life testing still spans 1,000 hours at 150 °C, yet suppliers mastering these hurdles enjoy premium pricing in the multilayer ceramic capacitor (MLCC) market.

Gen-AI Server Build-Out Spurs Ultra-Low-ESL, High-CV MLCC Adoption

Inference accelerators drawing 700 W per socket create voltage transients that demand 0402 MLCCs positioned within 2 mm of the die. Murata began shipping a 47 µF 4 V 0402 device in July 2025 that stacks 800 layers only 0.6 µm thick. KYOCERA AVX doubled capacity for its low-ESL server portfolio because each GPU board now carries up to 3,000 capacitors, far above CPU systems. TrendForce reported 35% MLCC unit growth in servers during 2025, well ahead of server shipment growth. Japanese precision houses therefore widen their lead as defect rates climb when active layers exceed 600.

Volatile Nickel and Palladium Prices Inflate BOM Costs

Nickel spiked 42% in early 2024 after Indonesian export curbs, then swung 18% lower by late 2025, while palladium fluctuated between USD 900 and USD 1,400 per troy ounce amid Russian supply uncertainty. A 10% rise in electrode-metal cost lifts finished MLCC bills by 3-5%, squeezing suppliers in consumer tiers where annual price erosion already approaches 8%. TDK said raw-material inflation trimmed its passive-component margin by 120 bps in fiscal 2026, accelerating copper electrode substitution. Murata is renegotiating quarterly price clauses tied to nickel futures, passing some risk to data-center clients. Smaller Asian suppliers without hedging programs cut automotive output in late 2025, deepening shortage conditions.

Other drivers and restraints analyzed in the detailed report include:

- On-Device AI and Advanced Wearables Require Sub-1005 Miniature MLCCs

- Geo-Diversified Friend-Shoring of Passive-Component Supply Chains

- Persistent Capacity Mismatch for Automotive-Grade MLCCs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Class 1 devices accounted for 62.69% multilayer ceramic capacitor (MLCC) market share in 2025, reflecting automakers' need for drift-free performance over 15-year vehicle lifespans. The segment is set to grow at a 15.83% CAGR, faster than the broader multilayer ceramic capacitor market size, as wide-bandgap inverters and medical electronics migrate to zero-temp-coefficient ceramics. Murata's 1,250 V C0G series exemplifies the shift toward thicker electrodes that combat electromigration while maintaining sub-ppm temperature tracking. In contrast, Class 2 barium-titanate parts still dominate smartphones because their higher volumetric efficiency offsets aging losses, yet they lose share in safety-critical designs.

The trade-off between board real estate and stability remains central. Class 1 capacitors occupy up to five times the footprint of Class 2 equivalents, yet predictable capacitance eliminates costly design margins, which matters in ISO 26262-compliant powertrain control units. Regulatory bodies do not explicitly mandate dielectric selection, but AEC-Q200 life testing implicitly steers designs toward Class 1 formulations. Consequently, the MLCC market continues to bifurcate: high-value automotive and industrial nodes lean on Class 1 stability, while consumer electronics retain Class 2 density.

The 0201 footprint captured 56.48% of the multilayer ceramic capacitor (MLCC) market in 2025, driven by smartphones and wearables chasing sub-millimetre components. Yet 0402 units are rising 16.02% annually, supported by AI servers that need 47 µF decoupling capacitors contiguous to 700 W GPUs. Murata's July 2025 release of an 800-layer 0402 part doubled capacitance density over its previous generation. KYOCERA AVX followed with a 10 µF 0402 range for smart-watch modules.

Manufacturing complexity scales sharply below 0402, requiring photolithography-grade clean rooms and laser trim. This concentrates capacity among three Japanese and Korean leaders, extending lead times to 20 weeks in early 2026, while Chinese entrants compete in commoditised 0603 and 0805 lines. As GPU boards swell to 3,000 MLCCs each, supply tightness in 0402 parts is likely to persist, underpinning premium price realisation across the multilayer ceramic capacitor market.

The Multilayer Ceramic Capacitor (MLCC) Market Report is Segmented by Dielectric Type (Class 1, and Class 2), Case Size (0 201, 0 402, 0 603, 1 005, 1 210, and More), Voltage Rating (Low-Range Voltage, Mid-Range Voltage, and More), Mounting Type (Surface-Mount, Metal-Cap, and Radial-Lead), End User (Automotive, Consumer Electronics, Industrial, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 57.69% of multilayer ceramic capacitor revenue in 2025, reflecting Japan's mastery of precision ceramics, South Korea's high-mix production, and China's vast consumer-electronics export engine. Chinese factories supplied up to 75% of global MLCC output, yet geopolitical tension spurred OEMs to dual-source through Japanese, Korean, and Indian sites. Murata, TDK, and Taiyo Yuden all ran full utilisation in early 2026 and expanded capacity in the Philippines and India to satisfy friend-shoring mandates. Samsung Electro-Mechanics, likewise running at capacity, channelled parts to BYD's 800 V vehicles while fortifying its Philippine campus.

North America is growing at 16.07% through 2031, buoyed by CHIPS and Science Act incentives that pull semiconductor and passive-component supply back onshore. Hyperscalers such as Microsoft and Amazon doubled server-grade MLCC orders during 2025, chasing ultra-low-ESL decoupling for AI accelerators. Proposed U.S. fabs remain delayed by labour cost and lengthy AEC-Q200 qualification cycles, so Mexican sites pick up overflow assembly under USMCA trade terms. Canada's piece is small but may rise as critical-mineral policies support domestic nickel and palladium supply.

Europe held a mid-teens share in 2025, tied to Germany's automotive corridor and Nordic renewable-energy projects. The European Union Chips Act encourages localisation, though strict RoHS and REACH standards extend qualification and inflate costs by up to 15% versus Asia. Wurth Elektronik is scaling automotive-grade output, yet still imports sub-micron dielectric powders from Japan. Elsewhere, South America, the Middle East, and Africa represent a low-single-digit slice, with growth centring on Brazil's electric-vehicle rollout and Gulf data-center builds that value low-inductance MLCCs.

List of Companies Covered in this Report:

- Murata Manufacturing Co., Ltd.

- Samsung Electro-Mechanics Co., Ltd.

- Taiyo Yuden Co., Ltd.

- Yageo Corporation

- TDK Corporation

- Kyocera AVX Components Corporation

- Walsin Technology Corporation

- Vishay Intertechnology, Inc.

- Wurth Elektronik GmbH and Co. KG

- Guangdong Fenghua Advanced Technology Holding Co., Ltd.

- Maruwa Co., Ltd.

- Samwha Capacitor Group

- Panasonic Holdings Corporation

- Shenzhen Torch Technology Co., Ltd.

- Holy Stone Enterprise Co., Ltd.

- Shenzhen Eyang Technology Development Co., Ltd.

- Johanson Dielectrics, Inc.

- KEMET Corporation (Yageo Group)

- Shenzhen Sunlord Electronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 800 V EV Architectures Accelerate Demand for High-Voltage MLCCs

- 4.2.2 Gen-AI Server Build-Out Spurs Ultra-Low-ESL, High-CV MLCC Adoption

- 4.2.3 On-Device AI and Advanced Wearables Require Sub-1 005 Miniature MLCCs

- 4.2.4 Geo-Diversified "Friend-Shoring" of Passive Component Supply Chains

- 4.2.5 Sustainability Mandates Favor Lead-Free and Recycled-Ceramic MLCCs

- 4.2.6 Semiconductor-Subsystem Co-Design Embeds MLCCs inside Chiplets

- 4.3 Market Restraints

- 4.3.1 Volatile Nickel and Palladium Prices Inflate BOM Costs

- 4.3.2 Persistent Capacity Mismatch for Automotive-Grade MLCCs

- 4.3.3 China Price-Led Offensive in Commodity MLCCs Erodes Global Margins

- 4.3.4 Physical Limits on Dielectric Layer Thickness (Less than 1 µm) Stall Capacitance Gains

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Supply-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Dielectric Type

- 5.1.1 Class 1

- 5.1.2 Class 2

- 5.2 By Case Size

- 5.2.1 0 201

- 5.2.2 0 402

- 5.2.3 0 603

- 5.2.4 1 005

- 5.2.5 1 210

- 5.2.6 Other Case Sizes

- 5.3 By Voltage Rating

- 5.3.1 Low Voltage (Less than 500 V)

- 5.3.2 Mid Voltage (500 - 1000 V)

- 5.3.3 High Voltage (Above 1000 V)

- 5.4 By Mounting Type

- 5.4.1 Surface-Mount

- 5.4.2 Metal-Cap

- 5.4.3 Radial-Lead

- 5.5 By End-Use Application

- 5.5.1 Aerospace and Defense

- 5.5.2 Automotive

- 5.5.3 Consumer Electronics

- 5.5.4 Industrial

- 5.5.5 Medical Devices

- 5.5.6 Power and Utilities

- 5.5.7 Telecommunications

- 5.5.8 Rest of End-Use Applications

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 South Korea

- 5.6.3.4 India

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 Rest of the World

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Murata Manufacturing Co., Ltd.

- 6.4.2 Samsung Electro-Mechanics Co., Ltd.

- 6.4.3 Taiyo Yuden Co., Ltd.

- 6.4.4 Yageo Corporation

- 6.4.5 TDK Corporation

- 6.4.6 Kyocera AVX Components Corporation

- 6.4.7 Walsin Technology Corporation

- 6.4.8 Vishay Intertechnology, Inc.

- 6.4.9 Wurth Elektronik GmbH and Co. KG

- 6.4.10 Guangdong Fenghua Advanced Technology Holding Co., Ltd.

- 6.4.11 Maruwa Co., Ltd.

- 6.4.12 Samwha Capacitor Group

- 6.4.13 Panasonic Holdings Corporation

- 6.4.14 Shenzhen Torch Technology Co., Ltd.

- 6.4.15 Holy Stone Enterprise Co., Ltd.

- 6.4.16 Shenzhen Eyang Technology Development Co., Ltd.

- 6.4.17 Johanson Dielectrics, Inc.

- 6.4.18 KEMET Corporation (Yageo Group)

- 6.4.19 Shenzhen Sunlord Electronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment