PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044183

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044183

Motherboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

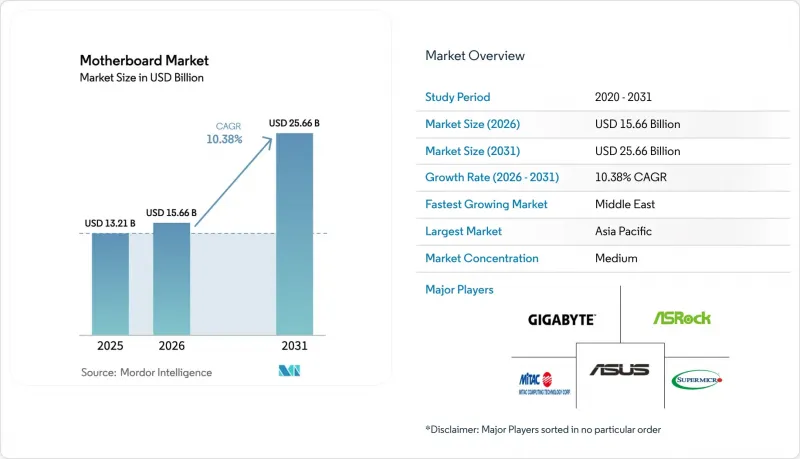

The motherboard market size is projected to expand from USD 13.21 billion in 2025 and USD 15.66 billion in 2026 to USD 25.66 billion by 2031, registering a CAGR of 10.38% between 2026 to 2031.

Growing AI-centric server rollouts are lifting average selling prices for high-layer server boards even as the consumer segment grapples with DDR5 cost swings. Socket transitions to AMD AM5 and Intel LGA-1851 are compressing upgrade windows, while industrial buyers shift toward ruggedized designs that tolerate harsh environments. Asia-Pacific continues to anchor volume through Taiwan's ODM cluster and China's contract-manufacturing base, yet the Middle East is emerging as the fastest-growing region as digital-infrastructure investments accelerate. Component tariffs, multi-layer PCB skill shortages, and second-hand board availability temper near-term demand but do not derail the long-run trajectory of the motherboard market.

Global Motherboard Market Trends and Insights

Server Motherboard Demand From AI Data-Centres

Hyperscale operators expanded AI infrastructure by 61% year-over-year in 2024, and Supermicro's X14 boards supporting up to 12 GPUs per node illustrate how dense topologies are lifting board complexity and margins. Multi-layer stack-ups, redundant VRMs, and out-of-band management add bill-of-materials value that consumer SKUs cannot match. Taiwan ODMs supplied more than 60% of global server-board volume in 2024, leveraging proximity to substrate vendors. Adoption of PCIe 5.0 slots per PCI-SIG CEM 5.0 spec compounds signal-integrity challenges but secures higher ASPs. With major cloud providers budgeting multi-billion-dollar GPU clusters through 2027, server boards remain a pivotal growth engine.

Rapid AM5 and LGA-1851 Platform Refresh Cycles

Intel's Z890 and B860 chipsets, introduced alongside Arrow Lake CPUs in late 2024, dropped DDR4 support and folded Wi-Fi 7 and Thunderbolt 4 into baseline features, forcing faster channel inventory transitions. AMD's AM5 socket, conversely, pledges chipset compatibility through 2027, allowing board brands to span entry-level B650 to halo X870E with minimal socket redesign. ASRock's B850 series debuted in January 2025 at mid-market price points, providing PCIe 5.0 M.2 without overclocking extras. The compressed cadence benefits agile ODMs that can re-tool quickly, but smaller firms face margin squeeze as payback windows narrow. Consumers confront shorter perceived longevity, nudging upgrade behavior toward subscription-like frequency.

End-User Hesitation Due to Generational Price Jumps

A mid-tier LGA-1851 system in early 2025 required USD 200 for the motherboard, USD 150 for 32 GB DDR5-6000, and USD 120 for a PCIe 5.0 SSD, totaling USD 470 before CPU and GPU, versus USD 320 for a comparable 2024 build. Asia-Pacific sees 39% of PC shipments refurbished, highlighting price sensitivity. South American buyers confront additional import duties, with Brazil's IPI adding 10-15% to component costs. The wider delta delays purchase intent, lengthening replacement cycles and trimming short-run shipments. Vendors respond with cut-down chipset SKUs, bundled memory promotions, and financing options, but elasticity remains limited in low-income regions.

Other drivers and restraints analyzed in the detailed report include:

- AI-Accelerated BIOS Utilities Driving DIY Upgrades

- Growth of Industrial IoT Requiring Rugged Boards

- Skill Shortage In Multi-Layer PCB Manufacturing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ATX accounted for 45.28% of 2025 revenue, securing the largest motherboard market share for its robust expansion-slot layout and ample VRM headroom. Mini-ITX, however, is forecast to accelerate at a 10.41% CAGR through 2031 as enthusiasts pursue space-efficient gaming rigs and integrators deploy edge-AI appliances in constrained enclosures. Outside holiday peaks, ATX maintains a steady enterprise refresh cadence, while Mini-ITX spikes align with trade-show launches that unveil high-density PCIe 5.0 storage capabilities.

PCIe 5.0 lanes and 16-phase VRMs have migrated into Mini-ITX, eroding the historical performance gap. ASRock's Taichi OCF Mini-ITX and Gigabyte's X870E Aorus Master showcase 105 A power stages inside 170 mm X 170 mm footprints, signaling that footprint no longer dictates capability. Micro-ATX remains the volume workhorse for budget OEM towers, balancing four expansion slots against simpler six-layer PCB stack-ups. Extended-ATX persists mainly in dual-socket servers and showcase overclocking boards, niches where the motherboard market size supports premium pricing on extra-wide PCBs.

Consumer and DIY builders generated 38.72% of 2025 sales, fueled by eSports cafes and home creators who value RGB lighting, high-refresh outputs, and reinforced PCIe slots. Gaming venues in China and India sustain high ASPs despite moderating unit growth. The industrial and embedded segment, by contrast, is on a 10.44% CAGR path that elevates the motherboard market size across automation and smart-city rollouts needing 5-year component roadmaps and IEC-compliant ruggedness.

Enterprise and data-center buyers demand out-of-band management, ECC memory, and multi-GPU topologies for AI training. Supermicro's server boards with NVIDIA NVLink bifurcation exemplify design features absent from the consumer realm. Longer 36-48 month production runs reduce design churn, improving gross margins relative to 12-18 month consumer cadences. Although gaming boards sell at 30-50% ASP premiums, industrial motherboards increasingly match that uplift by layering certifications, remote-monitoring hardware, and extended warranty packages.

The Motherboard Market Report is Segmented by Form Factor (ATX, Micro-ATX, Mini-ITX, and Extended-ATX), End-User Industry (Consumer/DIY, Gaming and ESports Centres, Industrial/Embedded, and Enterprise and Data-Centre), CPU Platform (Intel LGA-1700/1851, AMD AM4/AM5, and More), Application (Desktop PCs, Workstations, Servers, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 36.71% of the 2025 value, sustained by Taiwan's ODM ecosystem that compresses prototype-to-production lead times and China's 120 million-unit assembly base. Japanese vendors pivot toward factory-automation motherboards with IEC certifications, while South Korea's memory dominance supplies DDR5 modules that streamline board design. Australia and New Zealand contribute modest volumes, mainly in enterprise desktops and educational deployments, yet predictable refresh budgets create a resilient revenue floor.

The Middle East is the fastest-growing territory at a 10.52% CAGR through 2031. Saudi Arabia's USD 100 billion 2025 digital economy and the region's fintech boom are catalyzing low-cost desktop builds for call-center and government workloads. The United Arab Emirates's USD 20 billion electronics sector now locally assembles motherboards for data-center rollouts, reducing import friction. Intermittent power and broadband constraints drive demand for boards with wide-input PSUs and passive cooling, aligning with industrial-grade specifications and boosting regional motherboard market share for rugged SKUs.

North America and Europe represent mature but strategically important regions where tariff policies and eco-design mandates shape sourcing. The United States' 25%-35% Section 301 duties sparked diversification to Vietnam and Mexico, while USD 2 billion in CHIPS Act grants targets domestic substrate production. Europe's Directive 2024/1799 on repairability obliges vendors to supply spares for seven years, nudging designs toward modular daughtercards. Germany and the United Kingdom spearhead AI server deployments, whereas France promotes sovereign compute and Russia accelerates local assembly, all reinforcing sustained, if moderate, motherboard market growth.

- ASUSTeK Computer Inc.

- GIGABYTE Technology Co., Ltd.

- Micro-Star International Co., Ltd. (MSI)

- ASRock Incorporation

- Super Micro Computer, Inc.

- Advantech Co., Ltd.

- MiTAC Computing Technology Corporation

- Biostar Microtech International Corp.

- EVGA Corporation

- Acer Inc.

- Shenzhen Seavo Technology Co., Ltd.

- Sapphire Technology Ltd.

- AAEON Technology Inc.

- Kontron AG

- Advantech Europe B.V.

- DFI Inc.

- IEI Integration Corp.

- Dell Technologies Inc.

- Intel Corporation

- Lenovo Group Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid AM5 and LGA-1851 Platform Refresh Cycles

- 4.2.2 AI-Accelerated BIOS Utilities Driving DIY Upgrades

- 4.2.3 Growth of Industrial IoT Requiring Rugged Boards

- 4.2.4 Server Motherboard Demand From AI Data-Centres

- 4.2.5 Eco-Design Regulations Favoring Repairable Boards

- 4.2.6 Falling DDR5 Prices Lowering Total Build Costs

- 4.3 Market Restraints

- 4.3.1 End-User Hesitation Due to Generational Price Jumps

- 4.3.2 Skill Shortage in Multi-Layer PCB Manufacturing

- 4.3.3 Geopolitical Tariffs on Key PCB Raw Materials

- 4.3.4 Second-Hand LGA 1151 Boards Cannibalizing Sales

- 4.4 Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Form Factor

- 5.1.1 ATX

- 5.1.2 Micro-ATX

- 5.1.3 Mini-ITX

- 5.1.4 Extended-ATX (E-ATX)

- 5.2 By End-user Industry

- 5.2.1 Consumer / DIY

- 5.2.2 Gaming and eSports Centres

- 5.2.3 Industrial / Embedded

- 5.2.4 Enterprise and Data-centre

- 5.3 By CPU Platform

- 5.3.1 Intel (LGA-1700 / 1851)

- 5.3.2 AMD (AM4 / AM5)

- 5.3.3 ARM-based

- 5.3.4 RISC-V and Others

- 5.4 By Application

- 5.4.1 Desktop PCs

- 5.4.2 Workstations

- 5.4.3 Servers

- 5.4.4 Edge-AI and IoT Gateways

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 Turkey

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ASUSTeK Computer Inc.

- 6.4.2 GIGABYTE Technology Co., Ltd.

- 6.4.3 Micro-Star International Co., Ltd. (MSI)

- 6.4.4 ASRock Incorporation

- 6.4.5 Super Micro Computer, Inc.

- 6.4.6 Advantech Co., Ltd.

- 6.4.7 MiTAC Computing Technology Corporation

- 6.4.8 Biostar Microtech International Corp.

- 6.4.9 EVGA Corporation

- 6.4.10 Acer Inc.

- 6.4.11 Shenzhen Seavo Technology Co., Ltd.

- 6.4.12 Sapphire Technology Ltd.

- 6.4.13 AAEON Technology Inc.

- 6.4.14 Kontron AG

- 6.4.15 Advantech Europe B.V.

- 6.4.16 DFI Inc.

- 6.4.17 IEI Integration Corp.

- 6.4.18 Dell Technologies Inc.

- 6.4.19 Intel Corporation

- 6.4.20 Lenovo Group Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment