PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044188

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044188

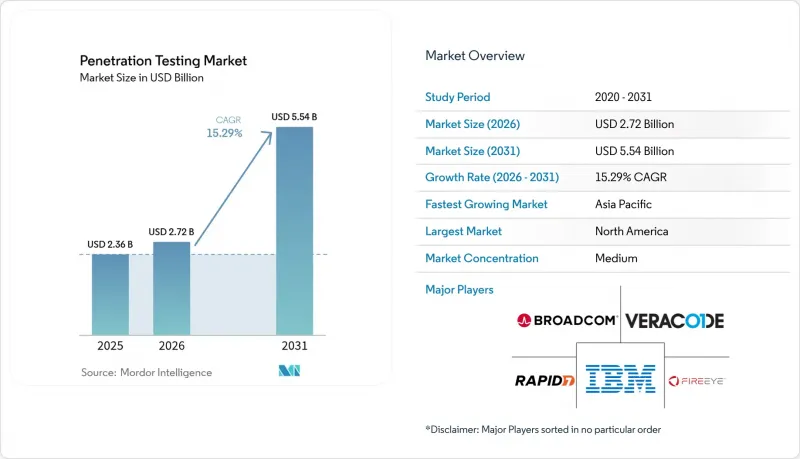

Penetration Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The penetration testing market size is projected to expand from USD 2.36 billion in 2025 and USD 2.72 billion in 2026 to USD 5.54 billion by 2031, registering a CAGR of 15.29% between 2026 to 2031.

Rapid adoption of cloud workloads, a sharp rise in generative-AI driven exploits, and compressed regulatory deadlines are moving penetration testing from ad-hoc audits to an always-on control. Enterprises now treat proactive validation as essential insurance against publicly disclosed vulnerabilities that adversaries weaponize within hours. Mandatory annual tests under HIPAA and PCI DSS version 4.0, along with the European Union's Digital Operational Resilience Act and NIS2, have shortened internal decision cycles and lifted multi-year contract values. Vendors are responding with autonomous red-team agents that cut test duration from weeks to days, while integration with CI/CD pipelines enables developers to trigger tests at every commit. Competitive dynamics, therefore, favor platforms that combine continuous coverage, regulatory mapping, and granular reporting.

Global Penetration Testing Market Trends and Insights

Rising Cybersecurity Risks Across Sectors

Public exploit kits now appear within hours of vulnerability disclosure, shrinking defenders' reaction windows and forcing more frequent penetration tests. Dragos counted 26 threat groups actively probing operational technology in 2026, showing that industrial environments no longer enjoy obscurity or safety. After a coordinated attack on Poland's energy grid, CISA urged quarterly testing for critical infrastructure operators, signaling regulatory impatience with annual testing cycles. A Pentera survey of 500 security leaders found 67% suffered at least one breach in the prior year and raised testing budgets to a median of USD 187,000, confirming that executives now treat proactive validation as insurance rather than an audit luxury. Together, these data points illustrate how escalating threat velocity directly expands demand for continuous penetration testing.

Increasing Demand for Security Assessments and Compliance Audits

Layered industry frameworks are stacking mandatory penetration-testing clauses, compelling organizations to synchronize multiple audits into one program. PCI DSS version 4.0, effective March 2025, requires annual testing for all merchants, plus segmentation and wireless assessments that were previously optional. FDA pre-market guidance obliges medical-device makers to include test results in every submission and maintain post-market evidence, widening the scope beyond hospitals to their suppliers. FedRAMP 3.0 requires quarterly scanning and annual testing for federal cloud providers, with a draft 4.0 proposal to double the cadence for high-impact systems. New York's amended 23 NYCRR 500 rule requires boards to review penetration-testing findings within 30 days, elevating tests from technical exercises to governance artifacts. These overlapping audits drive enterprises toward managed service providers that can map a single engagement to multiple rulebooks.

Shortage and High Cost of Skilled Testers

Global demand for certified penetration testers far exceeds supply, driving up engagement fees and lengthening project queues. ISC2 found that 95% of organizations report cybersecurity staffing gaps, ranking offensive testing among the three hardest roles to fill. The United Kingdom still needed 11,200 additional cybersecurity workers in 2024, with offensive roles taking the longest to hire. Pass rates for advanced OSCP credentials remain below 50%, underscoring steep learning curves and slow growth in the talent pipeline. Enterprises, therefore, turn to automation for routine tasks, yet scoping, social engineering, and post-exploitation analysis still require human expertise. The persistent talent deficit caps service capacity and tempers market growth despite strong demand.

Other drivers and restraints analyzed in the detailed report include:

- Government Mandates and Industry-Specific Regulations

- DevSecOps Pipelines Require Continuous Pen-Testing Integration

- Lack of Awareness Among SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Network assessments held a 38.23% market share in penetration testing in 2025, underscoring the continued priority of perimeter and lateral-movement defenses. Yet cloud penetration testing, propelled by multi-cloud adoption, is projected to advance at a 16.63% CAGR through 2031, making it the fastest-growing modality. The shift reflects container orchestration, serverless functions, and API-centric architectures that fall outside traditional network scopes. Bishop Fox expanded its CloudFox toolkit to Google Cloud Platform in 2026, signaling maturity in cloud-native testing methods. Mobile and web application tests are converging because adversaries frequently reuse API and credential-stuffing tactics across channels. Social-engineering exercises now simulate deepfake voice and video attacks, a trend made possible by generative AI. Wireless testing widens to cover Wi-Fi 6E and 5G private networks in factories and logistics hubs. IoT and operational technology assessments grow as industrial asset owners replicate production environments in sandboxes to avoid downtime.

The penetration testing market size for hybrid engagements that bundle network, cloud, and application scopes is growing, as buyers prefer a single contract that spans multiple frameworks. Vendors that offer unified dashboards and automated retesting win deals as compliance cycles tighten. Continuous validation expectations are rising quickly; Bishop Fox's Cosmos AI claims a 40% reduction in assessment time, while HackerOne's agentic service delivers findings within hours rather than days. These efficiency gains let security teams schedule more frequent tests without escalating budgets. As threat actors weaponize disclosed flaws in hours, enterprises gravitate toward modalities that confirm exploitability, not just vulnerability presence. Consequently, demand migrates from point-in-time network sweeps to always-on cloud and application probes that integrate directly into CI/CD pipelines.

On-premises deployments commanded 59.21% of the penetration testing market share in 2025, as many regulated sectors still favor on-premises control. However, cloud-delivered platforms are set to grow at a 15.61% CAGR to 2031, fueled by elastic scaling and rapid feature updates that align with DevSecOps cycles. Aikido Infinite lets developers trigger penetration tests on every commit without provisioning servers, illustrating the operational ease of SaaS delivery. PCI DSS 4.0 clarified that cloud-based tests satisfy cardholder data rules, removing a lingering barrier. Hybrid environments now dominate enterprise architectures, so visibility into both cloud workloads and on-premise assets becomes essential.

The penetration testing market for on-prem tools remains resilient in air-gapped government and defense networks, where sovereignty rules block external connectivity. Even there, vendors ship virtual appliances that synchronize anonymized findings once links are available. For the broader market, subscription pricing moves expenditure from capital to operating budgets, simplifying approvals. Managed service providers increasingly bundle cloud testing dashboards with verbal readouts that satisfy board-level reporting. Buyers also cite quicker patch validation when test results are fed directly into ticketing systems via REST APIs. As continuous deployment normalizes, organizations view cloud delivery not as an option but as the default unless a statute forbids it.

The Penetration Testing Market Report is Segmented by Testing Type (Cloud Penetration Testing, and More), Deployment Model (On-Premise, and More), Organization Size (Large Enterprises, and Small and Medium Enterprises), Service Delivery Mode (In-House Testing Teams, and Third-Party Managed Services), End-User Industry (IT and Telecom, Manufacturing, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 38.27% penetration testing market share in 2025, anchored by mature regulatory frameworks such as HIPAA, PCI DSS 4.0, and FedRAMP that formalize annual or semiannual testing cadences. U.S. financial institutions bundle threat-led testing into operational resilience programs, while Canadian health-privacy statutes drive hospitals to adopt continuous validation. Mexico's fast-growing fintech ecosystem also embeds penetration testing into cross-border payment licenses, widening regional demand. Venture funding is concentrated in Silicon Valley and Boston, allowing local platform vendors to iterate on AI agents that shorten test cycles for domestic clients. As a result, North America remains the reference market for new tooling and service models.

Asia-Pacific is forecast to expand its penetration testing market size at a 16.26% CAGR through 2031, the fastest regional trajectory. India's 30% to 50% cyber-talent gap encourages enterprises to adopt automated platforms, while data-localization rules in China compel in-country testing of all systems that handle personal information. Japan's revised Act on the Protection of Personal Information and South Korea's critical infrastructure mandates further hardwire annual testing into corporate governance. Rapid digital-payment adoption in Indonesia and the Philippines underscores the need for validation for small merchants connecting to regional gateways. Together, these factors create a demand surge that helps global vendors justify in-region cloud PoPs and local language reporting.

Europe benefits from a compliance floor established by the Digital Operational Resilience Act, NIS2, and the forthcoming Cyber Resilience Act, which collectively elevate penetration testing from best practice to a legal duty. Germany's BSI released sector playbooks for critical infrastructure in 2025, and France expanded its SecNumCloud framework to include mandatory testing for service providers. The United Kingdom's National Cyber Security Centre recommends annual tests for any firm handling sensitive data, to keep post-Brexit standards aligned with continental norms. South America, the Middle East, and Africa are emerging as strong markets as Brazil's data-protection law and Gulf national cyber programs embed offensive testing into licensing regimes. Overall geographic expansion is therefore paced by how quickly statutes migrate from guidance to enforcement across each jurisdiction.

- IBM Corporation

- Rapid7 Inc.

- Synopsys Inc.

- Checkmarx Ltd.

- Acunetix Ltd.

- Broadcom Inc.

- FireEye Inc.

- Veracode Inc.

- Qualys Inc.

- Tenable Holdings Inc.

- Palo Alto Networks Inc.

- Offensive Security LLC

- Core Security Technologies Inc.

- Pentera Security Ltd.

- HackerOne Inc.

- Trustwave Holdings Inc.

- IOActive Inc.

- NCC Group plc

- Cofense Inc.

- Bishop Fox Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Cybersecurity Risks Across Sectors

- 4.2.2 Increasing Demand for Security Assessments and Compliance Audits

- 4.2.3 Government Mandates and Industry-Specific Regulations

- 4.2.4 DevSecOps Pipelines Require Continuous Pen-Testing Integration

- 4.2.5 AI-Driven Autonomous Red Teaming Enables Continuous Validation

- 4.2.6 Software Bill of Materials Mandates Expand Supply-Chain Pentest Scope

- 4.3 Market Restraints

- 4.3.1 Lack of Awareness Among SMEs

- 4.3.2 Shortage and High Cost of Skilled Testers

- 4.3.3 Ethical Constraints on Live Exploitation of Critical OT Environments

- 4.3.4 Unclear Legal Liability in Multi-Jurisdiction Cloud Environments

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Testing Type

- 5.1.1 Network Penetration Testing

- 5.1.2 Web Application Penetration Testing

- 5.1.3 Mobile Application Penetration Testing

- 5.1.4 Social Engineering Penetration Testing

- 5.1.5 Wireless Network Penetration Testing

- 5.1.6 Cloud Penetration Testing

- 5.1.7 Other Testing Types

- 5.2 By Deployment Model

- 5.2.1 On-Premise

- 5.2.2 Cloud-Based

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Service Delivery Mode

- 5.4.1 In-House Testing Teams

- 5.4.2 Third-Party Managed Services

- 5.5 By End-User Industry

- 5.5.1 Government and Defense

- 5.5.2 Banking, Financial Services and Insurance

- 5.5.3 IT and Telecom

- 5.5.4 Healthcare and Life Sciences

- 5.5.5 Retail and E-Commerce

- 5.5.6 Manufacturing

- 5.5.7 Energy and Utilities

- 5.5.8 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves and Funding

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Rapid7 Inc.

- 6.4.3 Synopsys Inc.

- 6.4.4 Checkmarx Ltd.

- 6.4.5 Acunetix Ltd.

- 6.4.6 Broadcom Inc.

- 6.4.7 FireEye Inc.

- 6.4.8 Veracode Inc.

- 6.4.9 Qualys Inc.

- 6.4.10 Tenable Holdings Inc.

- 6.4.11 Palo Alto Networks Inc.

- 6.4.12 Offensive Security LLC

- 6.4.13 Core Security Technologies Inc.

- 6.4.14 Pentera Security Ltd.

- 6.4.15 HackerOne Inc.

- 6.4.16 Trustwave Holdings Inc.

- 6.4.17 IOActive Inc.

- 6.4.18 NCC Group plc

- 6.4.19 Cofense Inc.

- 6.4.20 Bishop Fox Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment