PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044194

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044194

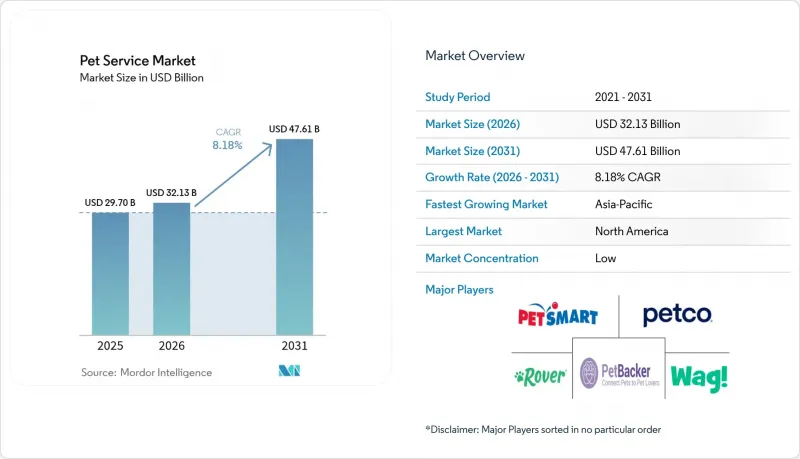

Pet Service - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Pet Service Market size is expected to grow from USD 29.70 billion in 2025 to USD 32.13 billion in 2026 and is forecast to reach USD 47.61 billion by 2031 at 8.18% CAGR over 2026-2031.

The trajectory is propelled by owners who increasingly treat companion animals as family, sustained venture-capital inflows, and software-driven efficiencies that compress scheduling and logistics costs. Recurring-revenue models, notably subscriptions that bundle wellness, grooming, and walking services, foster predictable cash flow and deepen customer loyalty. Digital booking platforms amplify capacity utilization, while mobile vans and in-home offerings satisfy time-pressed urban professionals. Mobile service adoption accelerated approximately 30% in 2025, driven by AI-powered scheduling platforms and consumer preference for in-home convenience. Consolidation is accelerating as private-equity sponsors deploy scale economics to offset wage inflation and compliance overhead.

Global Pet Service Market Trends and Insights

Trend of Pet Humanization and Premiumization

Seventy-one percent of owners now describe pets as family members, elevating expectations for salon-quality grooming and hotel-style boarding services. Luxury facilities feature live-stream video for owners, organic shampoos, and climate-controlled suites that echo human hospitality standards. Behavioral training, senior-pet wellness plans, and allergy-friendly spa packages have become routine offerings rather than niche add-ons. Retail-as-a-service shelves inside salons recommend breed-specific nutrition or dermatology products, converting trust into ancillary revenue. Providers with specialist credentials gain pricing power, sidestepping commodity pricing pressures that encumber basic-care operators.

Growth of Mobile and In-Home Service Models

Demand for door-to-door grooming, walking, and vet-teletriage climbed about 30% in 2025, enabled by route-optimization apps and cashless checkout. Purpose-built vans deliver professional equipment curbside, eliminating rent while capturing a convenience premium. The model eases pet stress by avoiding unfamiliar settings and appeals to apartment dwellers with limited transport options. Technology platforms like MoeGo, SuperSaaS, and Time To Pet facilitate seamless booking and route optimization, making mobile operations scalable for multi-vehicle fleets. This shift particularly benefits working professionals who value time savings and pets who experience reduced stress from familiar environment care.

Escalating Wage and Real-Estate Costs

Groomer salaries exceed USD 2,000-5,000 monthly, while certification programs add USD 6,630-8,800 in entry barriers, curbing talent pipelines . Prime storefront rents climb faster than service prices, squeezing single-location owners. Some operators pivot to suburban warehouses, and others downsize into mobile fleets that trade rent for vehicle financing. Subscriptions hedge against margin compression by locking in recurring revenue that smooths payroll spikes. Mobile service models emerge as partial solutions by eliminating fixed real estate costs, though vehicle acquisition and maintenance create alternative capital requirements. Service providers increasingly adopt subscription pricing models to improve cash flow predictability and offset rising operational expenses through recurring revenue streams.

Other drivers and restraints analyzed in the detailed report include:

- Rise in Pet Health-Insurance Utilization

- AI-Enabled Service Personalization and Scheduling

- Shortage of Skilled Groomers and Care Professionals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dogs delivered 54.30% of the pet service market share in 2025, reflecting higher visit frequency for walking, daycare, and grooming. Owner's willingness to purchase GPS-tracked adventures and social-play packages sustains volume. The pet service market size for dogs is poised to advance in lockstep with premium health offerings such as hydrotherapy pools and orthopedic daycare sessions. The cat segment is projected to grow at a CAGR of 7.18% through 2031, driven by urban pet owners seeking nutritional services, grooming for stress management, and automated litter box systems. Rising disposable income elevates feline services from occasional to scheduled visits, pushing the pet service market share for cats upward in multi-pet households.

Technology adoption diverges. Canine platforms emphasize route tracking, social media sharing, and wearable activity monitors that encourage add-on walks. Feline solutions favor health analytics from litter-box sensors and mood-scoring algorithms that signal stress triggers. Operators therefore zone facilities to separate aromas, acoustics, and lighting conducive to each species, earning premiums for species-specific expertise.

The Pet Service Market Report is Segmented by Pet Type (Dog, Cat, and Other Animals), by Service Type (Grooming, Pet Transportation, Pet Boarding, Pet Sitting, Pet Walking, and Other Specialized Services), and by Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 38.30% of the revenue in 2025, reflecting mature pet ownership and disposable incomes that can afford premium monthly plans. Subscription penetration exceeds 25% of customers, providing a stable cash flow for expansion through targeted acquisitions. Venture capital funding is directed toward AI software that automates check-ins and dynamic pricing. Regulatory oversight from agencies like the USDA emphasizes quality differentiation, with audited compliance serving as a key marketing factor.

Asia-Pacific posts the fastest 7.74% CAGR as rising wages and smaller household sizes spur companion-animal adoption. Megacities adopt mobile-van formats that circumvent high rents and traffic congestion. Governments in China and Hong Kong revise import protocols, acknowledging economic upside while requiring stricter welfare standards. Owners in Tokyo, Seoul, and Singapore are embracing tech-centric experiences, from robotic treat dispensers to on-demand cat grooming subscriptions.

Europe sustains steady growth in line with household income, anchored by robust welfare regulations that certify facilities and limit overcrowding. Operators differentiate themselves through ethical sourcing and eco-friendly products to resonate with consumers' sustainability priorities. Cross-border transport compliance remains complex, favoring multinational consolidators with in-house legal teams. Middle East and Africa are nascent yet promising, expatriate populations and urbanization seed demand for international-standard boarding and veterinary hybrid hubs that integrate grooming, training, and retail.

- PetSmart Inc. (BC Partners LLP)

- Petco Health and Wellness Company, Inc. (CVC Capital Partners and CPPIB)

- Rover Group, Inc.(Blackstone Inc.)

- Wag! Group Co.

- Dogtopia Enterprises LLC. (Red Barn Dog Holdings LLC.)

- PetBacker Pte. Ltd.

- Fetch! Pet Care, Inc.

- Best Friends Pet Care, Inc.

- Barking Mad Ltd. (Franchise Brands plc)

- We Love Pets Ltd.

- AirPets Relocation Services Pvt. Ltd.

- Swifto Inc.

- CareGuide Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Trend of Pet Humanization and Premiumization

- 4.2.2 Growth of Mobile and In-Home Service Models

- 4.2.3 Rise in Pet Health-Insurance Utilization

- 4.2.4 AI-Enabled Service Personalization and Scheduling

- 4.2.5 Subscription-Based Pet-Wellness Bundles

- 4.2.6 Venture-Capital Funding Spurring Capacity Expansion

- 4.3 Market Restraints

- 4.3.1 Escalating Wage and Real-Estate Costs

- 4.3.2 Regulatory Hurdles for Cross-Border Pet Transport

- 4.3.3 Shortage of Skilled Groomers and Care Professionals

- 4.3.4 Allergy and Zoonotic-Disease Concerns Among Consumers

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry Intensity

5 Market Size and Growth Forecasts (Value)

- 5.1 Segmentation by Pet Type

- 5.1.1 Dog

- 5.1.2 Cat

- 5.1.3 Other Animals

- 5.2 Segmentation by Service Type

- 5.2.1 Grooming

- 5.2.2 Pet Transportation

- 5.2.3 Pet Boarding

- 5.2.4 Pet Sitting

- 5.2.5 Pet Walking

- 5.2.6 Other Specialized Services

- 5.3 Segmentation by Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Russia

- 5.3.3.5 Spain

- 5.3.3.6 Italy

- 5.3.3.7 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 India

- 5.3.4.2 China

- 5.3.4.3 Japan

- 5.3.4.4 Australia

- 5.3.4.5 South Korea

- 5.3.4.6 Rest of Asia-Pacific

- 5.3.5 Middle East

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 Saudi Arabia

- 5.3.5.3 Rest of Middle East

- 5.3.6 Africa

- 5.3.6.1 South Africa

- 5.3.6.2 Nigeria

- 5.3.6.3 Rest of Africa

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 PetSmart Inc. (BC Partners LLP)

- 6.4.2 Petco Health and Wellness Company, Inc. (CVC Capital Partners and CPPIB)

- 6.4.3 Rover Group, Inc.(Blackstone Inc.)

- 6.4.4 Wag! Group Co.

- 6.4.5 Dogtopia Enterprises LLC. (Red Barn Dog Holdings LLC.)

- 6.4.6 PetBacker Pte. Ltd.

- 6.4.7 Fetch! Pet Care, Inc.

- 6.4.8 Best Friends Pet Care, Inc.

- 6.4.9 Barking Mad Ltd. (Franchise Brands plc)

- 6.4.10 We Love Pets Ltd.

- 6.4.11 AirPets Relocation Services Pvt. Ltd.

- 6.4.12 Swifto Inc.

- 6.4.13 CareGuide Inc.

7 Market Opportunities and Future Outlook