PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044197

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044197

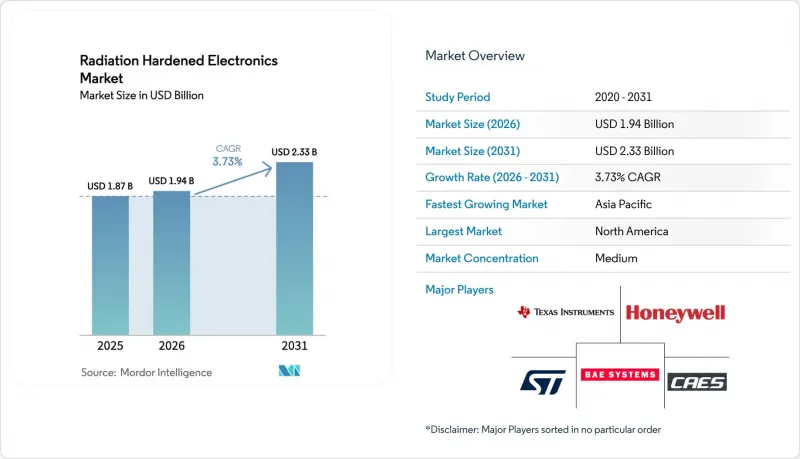

Radiation Hardened Electronics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Radiation Hardened Electronics Market size was valued at USD 1.87 billion in 2025 and is estimated to grow from USD 1.94 billion in 2026 to reach USD 2.33 billion by 2031, at a CAGR of 3.73% during the forecast period (2026-2031).

Demand continues to come from three structural outlets, namely mega-constellations in low Earth orbit, the modernization of NATO airborne and missile platforms, and the wave of new nuclear reactors in Asia and the Middle East. Product lifecycles are long because every part must clear multi-year qualification gates, yet suppliers are still expanding capacity for field-programmable gate arrays, gallium-nitride power devices, and mixed-signal front ends that can tolerate 100 kilorads or more. Program funding from the United States Space Force, the European Space Agency, and Asian nuclear utilities underpins steady unit volumes, while export-control rules and restricted foundry access temper upside growth.

Global Radiation Hardened Electronics Market Trends and Insights

Surge in LEO and Deep-Space Satellite Constellations

Orders for thousands of satellites per operator have changed purchasing patterns in the radiation hardened electronics market. Amazon committed USD 10 billion to Project Kuiper through 2026, while OneWeb finished its first constellation in 2024 and has green-lit a second cluster with laser inter-satellite links that require 10 gigabit-per-second single-event-latchup-immune transceivers. ESA's Galileo Second Generation payloads are specified for 15 years on-orbit, demanding oscillators hardened to 15 years of radiation exposure. Deep-space projects add extreme needs; NASA's Europa Clipper carries electronics verified to 2.9 megarads, removing most commercial parts from contention. The dual pull of higher volume and harsher physics pushes suppliers to lower unit costs while lifting the ceiling on total ionizing dose.

Modernization of Strategic and Tactical Defence Electronics in NATO Region

Defense ministries are replacing 1990s-era avionics with parts rated to today's single-event-upset benchmarks. The United Kingdom earmarked GBP 24 billion to refresh Tornado and Typhoon mission computers, and BAE Systems won GBP 317 million for gallium-nitride electronic-warfare suites on the Tempest fighter. The United States Air Force allocates USD 28 billion for Next Generation Air Dominance, specifying autonomous flight computers qualified to MIL-STD-883 Class S. Lockheed Martin's hypersonic projects carry rad-hard inertial sensors to survive plasma blackout, showing that tactical missiles are aligning with space standards. Together, these budgets anchor multi-year demand for processors qualified above 100 kilorads.

High Design-for-Reliability Cost and Long Qualification Cycles

Non-recurring engineering for a single mixed-signal IC often tops USD 5 million, and qualification may last 24-36 months. MIL-STD-883 testing demands multiple dose rates and temperatures, while heavy-ion beam time at ESA's RADEF or Texas A&M's cyclotrons can cost USD 3,000 per hour with queues that stretch a year. ESA's destructive-analysis flow pushes total outlay above USD 8 million for complex parts. Smaller satellite firms therefore select commercial chips with shielding and software scrubbing, accepting higher in-orbit failure risk in exchange for 60% lower cost and one-year shorter lead time.

Other drivers and restraints analyzed in the detailed report include:

- Nuclear-New-Build Momentum in Asia and Middle East

- High-Altitude UAV and Supersonic Aircraft Electronics Resilience Needs

- Restricted Foundry Capacity for RHBP Nodes <= 90 nm

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Space platforms represented 46.32% of 2025 revenue, underscoring how mega-constellations and science craft consume the largest share of the radiation hardened electronics market. Operators ordered more than 120,000 integrated circuits during 2025, and ESA's lunar programs keep demand resilient. Growth will trail the overall market because low Earth orbit constellations increasingly adopt selective shielding with commercial parts. High-altitude UAV and HAPS systems provide the fastest 4.11% CAGR lane as Airbus and U.S. primes validate stratospheric drones. Their avionics must survive cosmic rays at 70,000 feet, so every flight computer integrates triple-modular redundancy and error-correction logic. Classic aerospace and defense equipment - fighters, missiles, and naval combat systems - claimed about 28% of revenue, led by NATO modernization budgets that fund MIL-STD-883 Class S processors and gallium-nitride transmit-receive modules. The nuclear sector added around 12% thanks to the Kakrapar and Barakah reactors, while medical imaging and particle-physics labs filled the remainder.

The 2025 sales mix illustrates how the radiation hardened electronics market size remains weighted toward orbital platforms, yet faster unit expansion is visible in stratospheric drones and emerging hypersonic weapons. Defense primes increasingly blend space-qualified processors with Gallium-Nitride power stages to achieve weight savings. Nuclear utilities prioritize neutron-hard sensors that align with IAEA safety targets. Imaging system OEMs, guided by new FDA and EU rules, now specify rad-tolerant analog front ends for CT and PET scanners. Scientific facilities such as CERN's High-Luminosity Large Hadron Collider refresh detector electronics every shutdown using custom application-specific ICs built on radiation-hard-by-design libraries. Collectively, these shifts point to a gradual broadening of the customer base beyond traditional satellite integrators while keeping qualification pedigree at the center of procurement.

Analog and mixed-signal devices captured 35.21% of component revenue in 2025, reflecting their ubiquity in telemetry, sensor interfaces, and power conditioning. Voltage references, operational amplifiers, and high-precision data converters from Texas Instruments ship in every satellite bus, often rated to 100 kilorads total ionizing dose and single-event-latchup-immune. Field-programmable gate arrays expand at 4.41% per year, the fastest track among components. Microchip Technology's RT PolarFire, built on 28 nanometer process nodes with radiation-hard-by-design cells, logged 14 orbital prime wins in 2025 and enables on-orbit reconfiguration of phased-array antennas and synthetic-aperture radar processors. Microcontrollers and microprocessors add roughly 18% of revenue, anchored by BAE Systems' RAD5545 and Honeywell's RAD750 lines that meet 1 megarad tolerance for deep-space jobs.

Complementary components fill critical roles. Non-volatile memory, including spin-transfer-torque MRAM, accounts for about 15% of revenue, valued for its immunity to single-event upsets at LET levels above 80 MeV*cm2/mg. Discrete semiconductors and power management ICs comprise the balance, and their relevance rises with electric propulsion. Infineon's CoolGaN devices reach 98% efficiency in power-processing units, translating into lighter thermal systems for satellite buses. Taken together, the component breakdown shows a migration from fixed-function ASICs toward reconfigurable or software-defined elements that cut life-cycle cost and enable late-stage feature updates, a shift that benefits the radiation hardened electronics market.

The Radiation Hardened Electronics Market Report is Segmented by End-User (Space, Aerospace and Defense, and More), Component (Discrete Semiconductors, Sensors, and More), Product Type (Analog and Mixed-Signal, and More), Manufacturing Technique (RHBD, RHBP, and More), Semiconductor Material (Silicon, Sic, and More), Radiation Type (TID, SEE, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America delivered 41.63% of 2025 revenue as the United States Space Force budgeted USD 29 billion for space systems and NASA bought hardware for Artemis lunar-gateway modules. Ongoing F-35 avionics and Next Generation Air Dominance flight computers extend demand. Canada contributes through star trackers and ground stations built by MDA, preserving share in niche sensors. The region's future growth slows to the market average because NewSpace primes in California and Colorado have pivoted to commercial processors with software fault coverage, trimming the bill of material per spacecraft.

Asia Pacific is projected to expand at a 4.99% CAGR, the fastest regional clip in the radiation hardened electronics market. China's eight newly connected Hualong One reactors each mandate neutron-hard control electronics rated to 10^14 neutrons per cm2. India's Gaganyaan crewed capsule specifies 50 kilorad avionics with triple-modular redundancy, while South Korea's Nuri launch vehicle and lunar orbiter plans generate local sourcing mandates. Southeast Asian nuclear aspirations, led by Indonesia's 2 GWe partnership with Rosatom, will surface near 2028 and 2029. Japan's H3 launch vehicle and JAXA science missions continue to import mixed-signal ICs yet will localize microcontrollers through the Renesas-JAXA alliance.

Europe accounted for roughly 32% of 2025 revenue, centered on ESA's EUR 1.8 billion Galileo Second Generation and Airbus OneWeb spacecraft builds. The United Kingdom's Tempest fighter piles on gallium-nitride demand, and EU Medical Device Regulation rules enlarge need for rad-tolerant CT scanner channels. The Middle East delivered about 6%, dominated by UAE's Barakah nuclear program. South America and Africa stayed below 5%, although Brazil's planned small modular reactor and South Africa's Koeberg life-extension project form a pipeline. The dispersion shows how regional defense and energy strategies map directly onto capital flows in radiation hardened electronics.

List of Companies Covered in this Report:

- Honeywell International Inc.

- BAE Systems plc

- CAES (Cobham Advanced Electronic Solutions)

- Texas Instruments Inc.

- STMicroelectronics N.V.

- Microchip Technology Inc.

- Infineon Technologies AG

- Frontgrade Technologies

- Teledyne e2v Semiconductors

- AMD (Xilinx RT Series)

- Renesas Electronics Corp.

- Solid State Devices Inc.

- Micropac Industries Inc.

- Everspin Technologies Inc.

- Vorago Technologies

- Analog Devices HiRel

- International Rectifier HiRel (Infineon)

- Maxwell Technologies

- 3D Plus

- GSI Technology Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in LEO and Deep-Space Satellite Constellations

- 4.2.2 Modernization of Strategic and Tactical Defence Electronics in NATO Region

- 4.2.3 Nuclear-New-Build Momentum in Asia and Middle East

- 4.2.4 High-Altitude UAV and Supersonic Aircraft Electronics Resilience Needs

- 4.2.5 Mandated Radiation-Tolerance Standards in Medical Imaging (US FDA EU MDR)

- 4.2.6 Rapid Adoption of SiC/GaN Rad-Hard Power Devices in Spacecraft PPU

- 4.3 Market Restraints

- 4.3.1 High Design-for-Reliability Cost and Long Qualification Cycles

- 4.3.2 Restricted Foundry Capacity for RHBP Nodes ? 90 nm

- 4.3.3 Performance Trade-Offs Versus COTS Chips (Speed Density)

- 4.3.4 ITAR/Export-Control Supply-Chain Bottlenecks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Degree of Competition

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By End-User

- 5.1.1 Space

- 5.1.2 Aerospace and Defense (Air Land Naval)

- 5.1.3 Nuclear Power Generation and Fuel Cycle

- 5.1.4 Medical Imaging and Radiotherapy

- 5.1.5 High-Altitude UAV/HAPS Platforms

- 5.1.6 Industrial Particle Accelerators and Research Labs

- 5.2 By Component

- 5.2.1 Discrete Semiconductors

- 5.2.2 Sensors (Optical Image Environmental)

- 5.2.3 Integrated Circuits (ASIC SoC)

- 5.2.4 Microcontrollers and Microprocessors

- 5.2.5 Memory (SRAM MRAM FRAM EEPROM)

- 5.2.6 Field-Programmable Gate Arrays (FPGA)

- 5.2.7 Power Management ICs

- 5.3 By Product Type

- 5.3.1 Analog and Mixed-Signal

- 5.3.2 Digital Logic

- 5.3.3 Power and Linear

- 5.3.4 Processors and Controllers

- 5.4 By Manufacturing Technique

- 5.4.1 Rad-Hard-by-Design (RHBD)

- 5.4.2 Rad-Hard-by-Process (RHBP)

- 5.4.3 Rad-Hard-by-Software/Firmware Mitigation

- 5.5 By Semiconductor Material

- 5.5.1 Silicon

- 5.5.2 Silicon Carbide (SiC)

- 5.5.3 Gallium Nitride (GaN)

- 5.5.4 Other Semiconductor Materials

- 5.6 By Radiation Type

- 5.6.1 Total Ionizing Dose (TID)

- 5.6.2 Single-Event Effects (SEE)

- 5.6.3 Displacement Damage Dose (DDD)

- 5.6.4 Neutron and Proton Fluence

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 United Kingdom

- 5.7.3.2 Germany

- 5.7.3.3 France

- 5.7.3.4 Italy

- 5.7.3.5 Spain

- 5.7.3.6 Russia

- 5.7.3.7 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 India

- 5.7.4.3 Japan

- 5.7.4.4 South Korea

- 5.7.4.5 Australia

- 5.7.4.6 Southeast Asia

- 5.7.4.7 Rest of Asia Pacific

- 5.7.5 Middle East

- 5.7.5.1 United Arab Emirates

- 5.7.5.2 Saudi Arabia

- 5.7.5.3 Turkey

- 5.7.5.4 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Nigeria

- 5.7.6.3 Egypt

- 5.7.6.4 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Honeywell International Inc.

- 6.4.2 BAE Systems plc

- 6.4.3 CAES (Cobham Advanced Electronic Solutions)

- 6.4.4 Texas Instruments Inc.

- 6.4.5 STMicroelectronics N.V.

- 6.4.6 Microchip Technology Inc.

- 6.4.7 Infineon Technologies AG

- 6.4.8 Frontgrade Technologies

- 6.4.9 Teledyne e2v Semiconductors

- 6.4.10 AMD (Xilinx RT Series)

- 6.4.11 Renesas Electronics Corp.

- 6.4.12 Solid State Devices Inc.

- 6.4.13 Micropac Industries Inc.

- 6.4.14 Everspin Technologies Inc.

- 6.4.15 Vorago Technologies

- 6.4.16 Analog Devices HiRel

- 6.4.17 International Rectifier HiRel (Infineon)

- 6.4.18 Maxwell Technologies

- 6.4.19 3D Plus

- 6.4.20 GSI Technology Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Emerging Opportunities in Modular Small-Sat Avionics

- 7.3 On-Orbit Servicing and Manufacturing Electronics

- 7.4 Radiation-Tolerant AI Accelerators for Edge-Space Computing

- 7.5 Additive Manufacturing of Rad-Hard Packages