PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044223

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044223

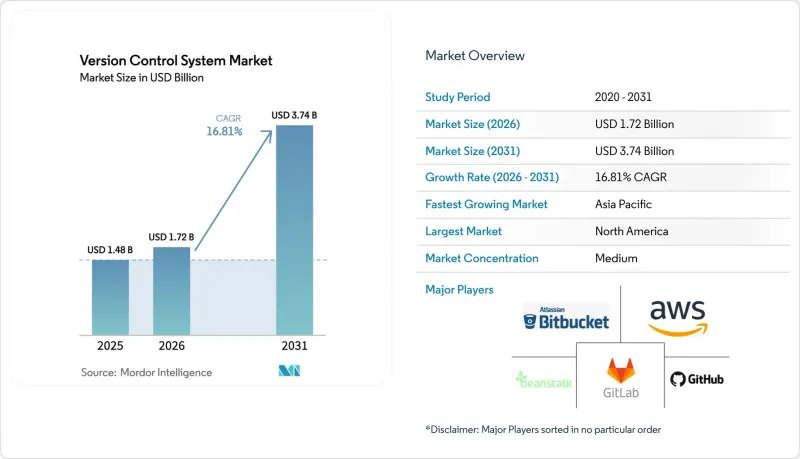

Version Control System - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The version control system market size is projected to be USD 1.48 billion in 2025, USD 1.72 billion in 2026, and reach USD 3.74 billion by 2031, growing at a CAGR of 16.81% from 2026 to 2031.

Enterprises are consolidating fragmented toolchains around Git-based platforms that now bundle continuous integration, security scanning and artifact provenance, reflecting a shift to single-vendor DevSecOps suites. Joint software bill of materials guidance released by twenty-one cybersecurity agencies in September 2025 intensified buyer focus on compliance-ready repositories, while the rapid rollout of agentic AI services such as GitHub Copilot and GitLab Duo is turning the repository into a hub for human-AI collaboration. Demand is reinforced by cloud deployment's elasticity, which supports surging commit volumes as teams adopt continuous delivery, and by the need for data-residency options that satisfy emerging sovereignty rules in Europe, Australia and the United States. Competitive intensity is growing as Microsoft, GitLab, and Atlassian race to integrate AI, signed-commit enforcement, and single-tenant architectures that appeal to regulated sectors.

Global Version Control System Market Trends and Insights

Mainstream DevOps Pipeline Adoption

Continuous integration workloads are soaring, illustrated by 11.5 billion GitHub Actions minutes consumed during 2024-2025, a 35% year-over-year increase that underscores tighter coupling between commits and automated testing. Automotive firms such as Jaguar Land Rover trimmed feedback cycles by 99% and executed as many as 70 daily deploys after moving to GitLab's unified DevSecOps environment. Survey data from Perforce shows 30% of automotive teams now bundle static analysis, version control, and continuous testing to raise code quality. Rising transaction volumes demand scalable branching strategies, conflict-resolution automation, and feature-flag management, favoring enterprise-grade Git platforms. Organizations, therefore, view integrated version control as a prerequisite for reliable, rapid software delivery.

Shift Toward Cloud-Native Workflows

Cloud-hosted repositories remove infrastructure burden and expose elastic compute that supports AI services unavailable in self-managed environments. GitLab's SaaS revenue grew 39% year-over-year in its fiscal Q2 2026, constituting 30% of company turnover. Microsoft is migrating hundreds of thousands of Azure Repos seats to GitHub so customers can tap Copilot's autonomous code generation. GitHub Enterprise Cloud introduced EU data residency in 2024 and expanded to Australia and the United States in 2025, removing sovereignty hurdles for financial services clients. Atlassian will add EU data residency for Bitbucket Cloud in 2026 to court risk-averse enterprises. Although cloud adoption raises vendor lock-in concerns, hybrid models that mix on-premise repositories for sensitive assets with cloud instances for collaboration are easing migration inertia.

Complex Multi-Vendor Toolchains

Nearly three-quarters of organizations run seven or more security tools, yet fewer than half scan both code and binaries, illustrating integration gaps that slow delivery. Atlassian's attempt to charge separately for Bitbucket self-hosted runners in December 2025 triggered backlash, revealing how layered pricing amplifies friction. Enterprises migrating from Azure DevOps to GitHub must rewire pipelines, boards, and testing suites, extending transformation timelines. API tokens spread across repositories, CI/CD, and registries increase compliance risk, prompting demand for unified identity management. The complexity of harmonizing disparate tools remains a brake on market expansion.

Other drivers and restraints analyzed in the detailed report include:

- AI-Assisted Code Review and Traceability

- Digital Product Compliance (SBOM, Secure Supply Chain)

- Repository Scalability Limitations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployment commanded 62.77% of the version control system market share in 2025 as enterprises prioritized elasticity and zero-maintenance operations. The segment is forecast to grow at a 17.32% CAGR through 2031, supported by the integration of AI copilots that rely on hyperscale compute. GitHub Enterprise Cloud's data-residency rollout in the EU, Australia and the United States has neutralized many sovereignty objections and catalyzed migrations from Azure Repos and self-managed Git servers. The version control system market size for cloud users will therefore expand fastest where regulators now accept SaaS platforms that hold FedRAMP, ISO 27001 and SOC 2 credentials.

On-premise installations persist among defense, semiconductor and aerospace organizations that mandate air-gapped environments. GitLab revealed that self-managed licenses still generated 70% of revenue in fiscal Q3 2026, although SaaS growth is outpacing on-premise sales. Perforce Helix Core and Unity Version Control remain staples for studios and automotive firms manipulating large binary assets under ISO 26262 workflows. Hybrid strategies-on-premise for sensitive IP and cloud for external collaboration-are closing the confidence gap and extending the version control system market to conservative buyers.

Distributed platforms such as Git held 92.43% of the version control system market share in 2025, a dominance born of flexible branching, offline commits and a rich plugin ecosystem. GitHub crossed the 100 million-developer threshold, while GitLab now counts more than half of the Fortune 100 among active customers, confirming the ubiquity of distributed workflows. The version control system market size attached to distributed tools will continue to rise as AI code generation multiplies commit events.

Centralized systems are expected to post a faster 17.64% CAGR through 2031 from a smaller base because binary-centric industries are revisiting exclusive locking models. Perforce's acquisition of Snowtrack, rebranded P4 One, makes the workflow friendlier for artists and designers, while Unity Version Control pitches smart locks that travel across branches. Automotive, gaming, and media teams value linear history, deterministic builds, and petabyte repositories. Their specialized needs create pockets of growth that preserve centralized tools' relevance inside the broader version control system market.

The Version Control System Market Report is Segmented by Deployment Mode (On-Premise, and Cloud), Type (Distributed VCS, and Centralized VCS), End-User Industry (IT and Telecom, BFSI, Retail and E-Commerce, Healthcare and Life Sciences, Media and Entertainment, Education, and More), Organization Size (Small and Medium Enterprises, and Large Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America dominated 39.78% of the market share in 2025, owing to GitHub's heavy Fortune 100 penetration and federal procurement rules that require FedRAMP Moderate authorization for DevSecOps suites. GitLab secured the same clearance for its Dedicated for Government service in early 2026, enabling public agencies to solicit competitive bids while preserving data sovereignty. Canada and Mexico trail the United States but are adopting SaaS repositories across fintech and near-shore software outsourcing, extending the regional version control system market.

Asia-Pacific is forecast to post an 18.02% CAGR through 2031, the fastest worldwide. India's services firms, China's internet conglomerates, and Southeast Asia's e-commerce leaders are migrating monolithic code bases to distributed Git workflows. Gaming hubs in Japan and South Korea rely on Perforce and Unity to manage terabyte-scale art assets, while Australia's public sector adopts GitHub Enterprise Cloud with local data storage. Fragmented regulations and lower SME spending temper growth, yet hyperscale cloud rollouts continue to unlock latent demand.

Europe's share is shaped by the Cyber Resilience Act, effective January 2024, and the Digital Operational Resilience Act, enforceable since January 17 2025. Both laws require SBOM generation and vulnerability disclosure, spurring demand for compliance-ready platforms. Germany, the United Kingdom and France lead adoption in automotive, finance and industrial IoT. South America, the Middle East and Africa still contribute a small portion of the version control system market, yet sovereign cloud mandates in Brazil, Saudi Arabia and South Africa signal future upside as local data centers come online and developer populations expand.

- GitHub (Microsoft Corporation)

- GitLab Inc.

- Bitbucket (Atlassian Corporation Plc)

- Perforce Software Inc.

- Amazon Web Services Inc.

- Azure DevOps (Microsoft Corporation)

- Google Cloud Source Repositories (Google LLC)

- Digital.ai Software Inc.

- Unity Technologies (Plastic SCM)

- Apache Subversion

- Beanstalk (Wildbit, LLC)

- Mercurial SCM

- Canonical Ltd. (Launchpad)

- Fossil SCM

- Azure Repos

- IBM Corporation (Rational Team Concert)

- SAP SE (SAP Cloud ALM)

- JetBrains s.r.o. (Space)

- Helix Core (Perforce Software Inc.)

- Dynatrace GmbH (Keptn)

- Anchorpoint Software GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream DevOps Pipeline Adoption

- 4.2.2 Shift Toward Cloud-Native Workflows

- 4.2.3 Cost Optimization Imperatives in Software Delivery

- 4.2.4 AI-Assisted Code Review and Traceability

- 4.2.5 Digital Product Compliance (SBOM, Secure Supply Chain)

- 4.2.6 Real-Time Asset Collaboration in Gaming and Media

- 4.3 Market Restraints

- 4.3.1 Complex Multi-Vendor Toolchains

- 4.3.2 Repository Scalability Limitations

- 4.3.3 Shortage of Advanced VCS Skill Sets

- 4.3.4 Open-Source License and Vulnerability Exposure

- 4.4 Industry Supply Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.2 By Type

- 5.2.1 Distributed VCS

- 5.2.2 Centralized VCS

- 5.3 By End-user Industry

- 5.3.1 IT and Telecom

- 5.3.2 BFSI

- 5.3.3 Retail and E-commerce

- 5.3.4 Healthcare and Life Sciences

- 5.3.5 Media and Entertainment

- 5.3.6 Education

- 5.3.7 Gaming and Digital Content

- 5.3.8 Automotive and Embedded Systems

- 5.3.9 Aerospace and Defense

- 5.3.10 Other End-user Industries

- 5.4 By Organization Size

- 5.4.1 Small and Medium Enterprises

- 5.4.2 Large Enterprises

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Kenya

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 GitHub (Microsoft Corporation)

- 6.4.2 GitLab Inc.

- 6.4.3 Bitbucket (Atlassian Corporation Plc)

- 6.4.4 Perforce Software Inc.

- 6.4.5 Amazon Web Services Inc.

- 6.4.6 Azure DevOps (Microsoft Corporation)

- 6.4.7 Google Cloud Source Repositories (Google LLC)

- 6.4.8 Digital.ai Software Inc.

- 6.4.9 Unity Technologies (Plastic SCM)

- 6.4.10 Apache Subversion

- 6.4.11 Beanstalk (Wildbit, LLC)

- 6.4.12 Mercurial SCM

- 6.4.13 Canonical Ltd. (Launchpad)

- 6.4.14 Fossil SCM

- 6.4.15 Azure Repos

- 6.4.16 IBM Corporation (Rational Team Concert)

- 6.4.17 SAP SE (SAP Cloud ALM)

- 6.4.18 JetBrains s.r.o. (Space)

- 6.4.19 Helix Core (Perforce Software Inc.)

- 6.4.20 Dynatrace GmbH (Keptn)

- 6.4.21 Anchorpoint Software GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment