PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044226

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044226

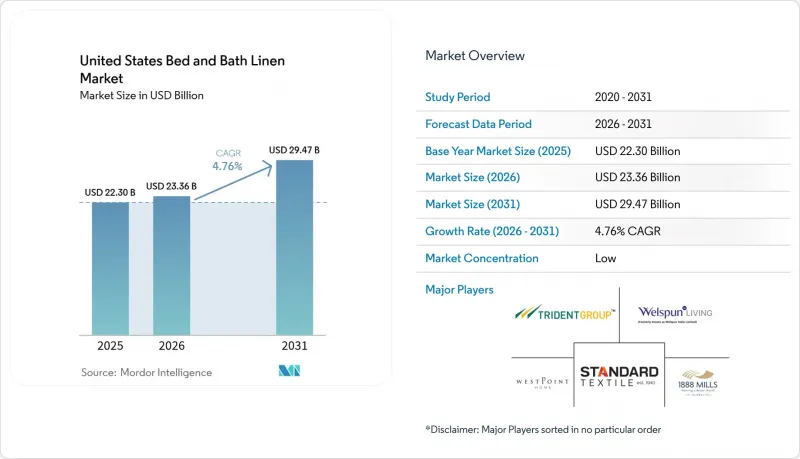

United States Bed And Bath Linen - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States bed and bath linen market size is expected to grow from USD 22.30 billion in 2025 to USD 23.36 billion in 2026, and is forecast to reach USD 29.47 billion by 2031, at a 4.76% CAGR over 2026-2031. Growth builds on stable institutional procurement, a robust hotel construction pipeline that adds nearly 100,000 rooms in 2026, and sustained home-improvement expenditure led by bathroom remodels that refresh towels, mats, and shower curtains. E-commerce penetration continues to rise, now driving a greater share of bed and bath linen purchases, reinforcing direct-to-consumer models and platform partnerships that shorten time-to-market for new collections. Certification momentum shapes demand, with OEKO-TEX issuing 57,412 certificates and labels in 2024 and 2025 combined, and Global Organic Textile Standard registrations expanding further in 2024, signaling firm buyer preferences for verified safe and organic textiles. Hospitality fundamentals show near-term softness in RevPAR, though mega-events such as the FIFA World Cup 2026 and brand conversion cycles still support linen replenishment tied to standard upgrades.

United States Bed And Bath Linen Market Trends and Insights

Residential Turnover and Renovation Cycles

United States home turnover fell to 28 per 1,000 homes in the first nine months of 2025, a 31.2% decline from pre-pandemic 2019 levels, primarily because over 70% of mortgaged homeowners hold mortgage rates below 5% and resist selling into a 6.17% rate environment. First-time buyers represented 31% of existing-home sales in January 2026, up from 28% a year earlier, a shift that supports repeat purchases of coordinated bed and bath sets for new household setups. Renovation spending reached USD 522 billion in 2025 and is expected to grow 2.9% early in 2026 before moderating to 1.6% by year-end, a pattern that favors bath linen upgrades as homeowners refresh fixtures and soft goods in tandem. Bathroom remodels remain among the most popular projects, with urban households reporting a higher incidence than their non-urban peers, pointing to concentrated demand for towels, bathmats, and shower curtains in dense metro areas, where value per square foot justifies higher-quality textiles.

Hospitality Pipeline, Renovations, and Brand Standards

Hotel construction is rebounding, with the 2027 pipeline tracking 1,688 hotels and nearly 192,000 rooms nationwide. Extended-stay hotels comprise 40% of all projects and 34% of all rooms in the construction pipeline at Q3 2025, with middle-tier extended-stay accounting for 1,648 projects/154,499 rooms. Brand conversions reached record levels, with 1,477 projects and 148,035 rooms, up 18% by projects and 22% by rooms year over year, prompting owners to replace linens to meet new flag standards for specifications and treatments. Industry forecasts peg 2026 RevPAR growth at just +0.6%, which signals cautious near-term property spending even as installed capacity rises, while the FIFA World Cup 2026 is expected to contribute +0.4% to the United States RevPAR and drive localized spikes in occupancy and turnover. The United States bed and bath linen market absorbs these cyclical effects through steady institutional replenishment and contract-led adoption of antimicrobial and sustainability features when brands update operating standards.

Intense Price Competition and Private-Label Penetration Compressing Margins

Price competition is heightened in mass and big-box channels as retailers scale proprietary lines and negotiate volume-based pricing that constrains national brand pricing power. Offline distribution remains large and tactile, yet the online share at 28.38% with a projected 5.98% CAGR intensifies transparency as shoppers compare SKUs and reviews in seconds, prompting frequent promotions that weigh on margins. Large retailers are also investing in upstream capabilities and innovation, such as Walmart's Home Textiles Innovation Lab with the Fashion Institute of Technology, which signals an intent to raise the quality of private labels. Direct-to-consumer brands recalibrated physical footprints to preserve unit economics, with Parachute closing most stores in 2025 and pivoting to a selective blend of e-commerce, wholesale, and flagships, while Brooklinen continues to optimize a smaller set of showrooms. This environment pushes suppliers in the United States bed and bath linen market to double down on differentiated features and sustainability badges that rank well in search and on the marketplace.

Other drivers and restraints analyzed in the detailed report include:

- Institutional Demand Growth from Healthcare, Senior Living, and Student Housing Facilities

- Sustainability Certification-Led Premiumization (GOTS, OEKO-TEX)

- Softening Hotel RevPAR/Occupancy in Near Term

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bed linen captured 58.21% of the United States bed and bath linen market share in 2025, supported by the steady replacement of sheets, pillowcases, and duvet covers on 18 to 24-month cycles in many households. Bath linen accounted for 41.79% and is set to grow faster at a 6.65% CAGR through 2031, aided by hotel pipeline additions and extended-stay formats that stock more towels and mats per room. Large-scale producers reinforce category stability, with Welspun reporting that every fifth towel and every seventh sheet sold domestically is manufactured by the company, which supports the rapid rollout of antimicrobial finishes when brand specifications change. Standard Textile emphasizes innovation with more than 150 patents across hospitality products and features such as EZ ID and Center-Lock Labels, which help reduce room makeup times and total housekeeping costs. These elements position bed basics as the volume anchor while lifting the cadence and specification of bath linen orders during peak travel and renovation cycles in the United States bed and bath linen market.

Bath linens' outperformance is linked to construction and conversion dynamics, as extended-stay hotels represent a large share of the pipeline and require heavier towel inventories per occupied room to meet guest expectations for multi-day stays. Antimicrobial bath products are seeing broader use in hospitality and healthcare, supported by technologies such as 1888 Mills' work with FUZE on a durable, water-based treatment that remains effective after more than 100 laundry cycles. The United States healthcare facilities are also on a steady replacement path, with linen replacement costs projected to reach USD 1 billion in 2026, which sustains orders for high-durability terry and performance bedding in medical and senior living settings. In the United States bed and bath linen industry, volume remains anchored by sheets and pillowcases while bathmats and shower curtains add incremental revenue during renovation cycles, particularly in urban cores where bathroom upgrades index higher. These trends underpin the medium-term mix shift toward bath textiles without displacing bed basics as the category's core.

Residential end users accounted for 69.15% of the United States bed and bath linen market, and the residential market is projected to grow at a 6.48% CAGR through 2031. First-time buyers accounted for 31% of existing-home sales in January 2026, creating fresh demand for starter sets in bedrooms and bathrooms, even as total transactions remained muted. As these households prioritize health and aesthetics, certified organic cotton towels and OEKO-TEX labeled sheets earn a pricing premium that buyers accept when transparency and comfort are clear. Residential growth leans on these quality signals, while the commercial base provides predictable contract volumes in the United States bed and bath linen market.

Commercial demand remains steady, with full-bed utilization, and senior housing occupancy reached 89.4% in Q4 2025 and is expected to exceed 90% in 2026 as more baby boomers turn 80 and move into congregate settings. Active adult communities operated near 92% occupancy on average and rose to around 95% at properties open for at least 2 years, and newly built assisted living or memory care properties include larger floor plans that increase per-unit linen needs. Student housing preleasing reached 52.3% for the 2026 to 2027 academic year in January 2026, with purpose-built beds near record occupancy, and around 30,000 new beds scheduled for Fall 2026 delivery. Short-term rentals add frequent turnover, pushing higher wash and replacement cycles, even as supply growth moderates in 2026 in coastal and large-city markets. The FIFA World Cup 2026 is expected to generate a localized midyear lift in occupancy and linen utilization, even if full-year hospitality RevPAR remains generally flat.

The United States Bed and Bath Linen Market Report is Segmented by Product Type (Bed Linen and Bath Linen), End User (Residential, Commercial), Distribution Channel (Offline and Online), Material (Cotton, Linen, Others), and Geography (Northeast, Midwest, South, West). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Welspun USA (Welspun Living)

- WestPoint Home (Martex)

- Trident Group

- 1888 Mills

- Standard Textile

- Brooklinen

- Boll & Branch

- Parachute Home

- Coyuchi

- Frette

- SFERRA

- Peacock Alley

- Matouk

- Kassatex

- The Company Store

- Pottery Barn

- Crane & Canopy

- Downlite Hospitality

- Manchester Mills

- Pacific Coast Feather Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Residential turnover and renovation cycles

- 4.2.2 Hospitality pipeline, renovations, and brand standards

- 4.2.3 Institutional demand growth from healthcare, senior living, and student housing facilities

- 4.2.4 Sustainability certification-led premiumization (GOTS, OEKO-TEX)

- 4.2.5 Short-term rental and mid-term stay inventory growth

- 4.2.6 Antimicrobial and performance textiles adoption in commercial settings

- 4.3 Market Restraints

- 4.3.1 Intense price competition and private-label penetration compressing margins

- 4.3.2 Softening hotel RevPAR/occupancy in near term

- 4.3.3 Supply chain disruptions and import tariff exposure impacting sourcing costs

- 4.3.4 Slower population growth and immigration headwinds

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Bed Linen

- 5.1.1.1 Sheets

- 5.1.1.2 Pillows

- 5.1.1.3 Pillow Covers

- 5.1.1.4 Duvet Cases

- 5.1.1.5 Blankets

- 5.1.1.6 Comforters

- 5.1.1.7 Mattress Protectors

- 5.1.2 Bath Linen

- 5.1.2.1 Towels

- 5.1.2.2 Bathrobes

- 5.1.2.3 Bathmats

- 5.1.2.4 Shower Curtains

- 5.1.1 Bed Linen

- 5.2 By End User

- 5.2.1 Residential

- 5.2.2 Commercial

- 5.3 By Distribution Channel

- 5.3.1 Offline

- 5.3.1.1 Mass Merchandisers (Hypermarkets/Supermarkets)

- 5.3.1.2 Home Centers

- 5.3.1.3 Specialty Stores

- 5.3.1.4 Other Distribution Channels

- 5.3.2 Online

- 5.3.1 Offline

- 5.4 By Material

- 5.4.1 Cotton

- 5.4.2 Linen

- 5.4.3 Others

- 5.5 By Geography

- 5.5.1 Northeast

- 5.5.2 Midwest

- 5.5.3 South

- 5.5.4 West

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Welspun USA (Welspun Living)

- 6.4.2 WestPoint Home (Martex)

- 6.4.3 Trident Group

- 6.4.4 1888 Mills

- 6.4.5 Standard Textile

- 6.4.6 Brooklinen

- 6.4.7 Boll & Branch

- 6.4.8 Parachute Home

- 6.4.9 Coyuchi

- 6.4.10 Frette

- 6.4.11 SFERRA

- 6.4.12 Peacock Alley

- 6.4.13 Matouk

- 6.4.14 Kassatex

- 6.4.15 The Company Store

- 6.4.16 Pottery Barn

- 6.4.17 Crane & Canopy

- 6.4.18 Downlite Hospitality

- 6.4.19 Manchester Mills

- 6.4.20 Pacific Coast Feather Company

7 Market Opportunities & Future Outlook

- 7.1 Premium and differentiated product innovation

- 7.2 Omnichannel expansion and subscription-based replenishment models