PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044232

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044232

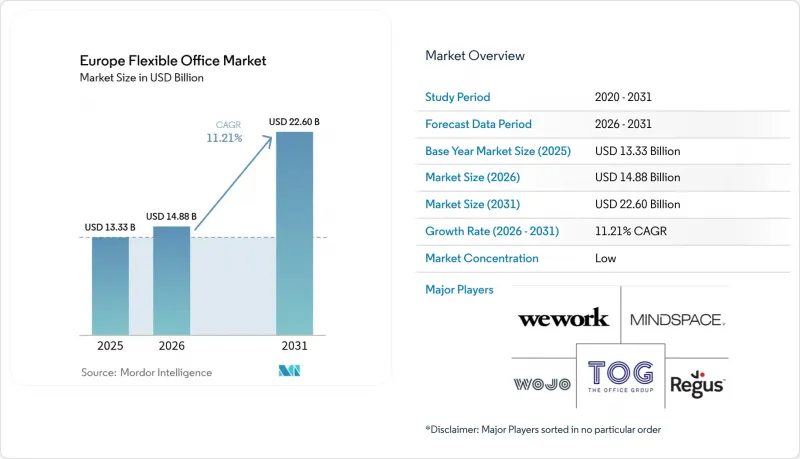

Europe Flexible Office - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe flexible office market size is projected to be USD 13.33 billion in 2025, USD 14.88 billion in 2026, and reach USD 22.60 billion by 2031, growing at a CAGR of 11.21% from 2026 to 2031.

Base-year revaluation, which now captures previously untracked serviced-office inventory as well as embedded flex desks inside corporate headquarters, produced the sharp 2025-2026 step-change, aligning European reporting with North American IFRS 16 lease-accounting standards. Hybrid work policies that require three to four days in the office each week, together with rising demand for Grade-A, ESG-certified buildings, have created a resilient baseline for occupiers that view flex space as an essential portfolio component rather than surge capacity. AI-enabled occupancy analytics and private 5G connectivity are lifting revenue per workstation and lowering entry barriers for independent operators. Meanwhile, sustainability-linked loans are channeling capital into retrofit projects, expanding high-quality supply and keeping vacancy for premium assets structurally tight.

Europe Flexible Office Market Trends and Insights

Flight-to-Quality Toward Grade-A, ESG-Compliant Flex Offices

Occupiers are trading up to buildings that deliver verifiable environmental performance, widening the rent premium for certified space to 15-20% over secondary stock in 2025. EU Corporate Sustainability Reporting Directive rules compel disclosure of Scope 3 emissions from leased real estate, making uncertified space a reputational liability. Operators such as IWG and The Office Group publish granular carbon-intensity metrics and have portfolio-wide net-zero commitments. In turn, landlords favor revenue-share partnerships with flex brands that help de-risk stranded assets. This quality flight anchors price resilience for prime flex hubs even while incentives proliferate in lower-grade buildings.

Mandatory 3-to-4-Day Office Policies Sustain Hybrid Flex-Space Demand

Europe's largest employers have converted temporary hybrid schedules into permanent policy. Vodafone requires eight office days per month, the European Central Bank has extended its hybrid framework through 2027, and Microsoft keeps a three-day rule for regional staff. Because daily attendance remains unpredictable, enterprises hedge by locking multi-year memberships that guarantee overflow capacity, ensuring stable occupancy for operators. Policy reversals such as Stellantis's 2024 full-time return order underscore volatility, reinforcing flex space as insurance against mandate changes. Even with tech head-count reductions, desk-per-employee ratios are rising, supporting revenue growth. This structural shift explains why the Europe flexible office market continues expanding despite cyclical layoffs.

High Fit-Out & M&E Costs Erode Operator Margins

Construction-cost inflation ran 8-12% annually in 2024-2025, lifting premium fit-out spend to USD 870-1,305 per m2. Advanced HVAC controls, LED lighting, and smart-building sensors demanded by EU Taxonomy compliance add another 15-20% to budgets. Because new sites often take 18-24 months to reach break-even, capital-constrained operators risk prolonged cash burn. Smaller brands lacking bulk-purchase agreements or in-house engineering are most exposed, pushing them toward lower-value freelancer niches and away from enterprise contracts.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Decarbonization & EU Taxonomy Accelerate Retrofit Flex Hubs

- Green-Linked Loans Unlock Refinancing of Distressed Assets Into Flex Space

- Vacant Secondary Offices Undercut Flex Rents With Incentives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Co-working spaces captured 51.22% of Europe flexible office market revenue in 2025, underscoring their appeal to freelancers and creative agencies that prize collaboration. Serviced offices and executive suites, however, are forecast to grow at a 12.1% CAGR to 2031, outpacing overall Europe flexible office market size expansion as banks and consulting firms prioritize data security. The serviced segment's rise mirrors NIS2 compliance pressure; enclosed layouts with dedicated HVAC, lockable access, and private server racks command 30-40% pricing premiums[3]. Operators respond with hybrid products that combine private suites and shared lounges, balancing confidentiality with community.

Continued flight-to-quality strengthens serviced-suite demand. IWG, for example, pre-leased 250,000 m2 of new ESG-certified space across Germany, France, and Spain under a 2025 alliance with Allianz Real Estate. Meanwhile, modular fit-out systems cut build times to eight weeks, reducing capital cycles and de-risking expansion. Co-working's share remains large but is edging lower as enterprise occupiers reshape the Europe flexible office market share mix in favor of privacy-first formats.

The Europe Flexible Office Market Report is Segmented by Type (Co-Working Spaces, Serviced Offices / Executive Suites, and More) by Sector (Information Technology (IT and ITES), and More), by End Use (Enterprises, Freelancers and Start Ups & Others), and by Country (UK, Germany, France, Spain, Italy and Rest of Europe). The Report Provides Market Size and Forecasts in Value (USD) for all the Above Segments.

List of Companies Covered in this Report:

- Regus Group Companies

- WeWork

- The Office Group

- Mindspace

- Wojo

- Knotel

- Talent Garden

- Huckletree

- Selina

- Bisley Flexible Offices

- Impact Hub

- Techspace

- Labs (LabTech)

- CBRE Hana (now - The Office Partners)

- Deskopolitan

- Spacesworks

- Utopicus (Banco Santander)

- Station F

- Ordnungs ApS

- Matrikel 1

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Flight-to-quality toward Grade-A, ESG-compliant flex offices

- 4.2.2 Mandatory 3-to-4-day office policies sustain hybrid flex-space demand

- 4.2.3 Corporate decarbonisation & EU Taxonomy accelerate retrofit flex hubs

- 4.2.4 Green-linked loans unlock refinancing of distressed assets into flex space

- 4.2.5 AI-driven occupancy analytics lift revenue per workstation

- 4.2.6 Private 5G neutral-host roll-out lowers IT barriers for satellite flex offices

- 4.3 Market Restraints

- 4.3.1 High fit-out & M&E costs erode operator margins

- 4.3.2 Vacant secondary offices under-cut flex rents with incentives

- 4.3.3 NIS2 and GDPR privacy scrutiny delays large-enterprise uptake of small brands

- 4.3.4 Cross-border VAT gaps inflate TCO for multi-country occupiers

- 4.4 Value / Supply-Chain Analysis

- 4.4.1 Overview

- 4.4.2 Real Estate Developers & Asset Owners - Key Insights

- 4.4.3 Workspace Design & Technology Consultants - Key Insights

- 4.4.4 Modular Furniture & Smart Office Solutions Providers - Key Insights

- 4.5 Government Regulations & Initiatives in the Industry

- 4.6 Technological Innovations in the Flexible Office Real Estate Market

- 4.7 Key Office Real-Estate Metrics (Supply, Rentals, Prices, Occupancy/Vacancy %)

- 4.8 Impact of Remote Working on Space Demand

- 4.9 Porter's Five Forces

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitutes

- 4.9.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value USD)

- 5.1 By Type

- 5.1.1 Co-Working Space

- 5.1.2 Serviced Offices / Executive Suites

- 5.1.3 Others (Hybrid, Virtual Office)

- 5.2 By Sector

- 5.2.1 Information Technology (IT & ITES)

- 5.2.2 BFSI (Banking, Financial Services & Insurance)

- 5.2.3 Business Consulting & Professional Services

- 5.2.4 Other Services (Retail, Life-Sciences, Energy, Legal)

- 5.3 By End Use

- 5.3.1 Freelancers

- 5.3.2 Enterprises

- 5.3.3 Start-Ups & Others

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 France

- 5.4.3 UK

- 5.4.4 Spain

- 5.4.5 Italy

- 5.4.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Regus Group Companies

- 6.3.2 WeWork

- 6.3.3 The Office Group

- 6.3.4 Mindspace

- 6.3.5 Wojo

- 6.3.6 Knotel

- 6.3.7 Talent Garden

- 6.3.8 Huckletree

- 6.3.9 Selina

- 6.3.10 Bisley Flexible Offices

- 6.3.11 Impact Hub

- 6.3.12 Techspace

- 6.3.13 Labs (LabTech)

- 6.3.14 CBRE Hana (now - The Office Partners)

- 6.3.15 Deskopolitan

- 6.3.16 Spacesworks

- 6.3.17 Utopicus (Banco Santander)

- 6.3.18 Station F

- 6.3.19 Ordnungs ApS

- 6.3.20 Matrikel 1

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment