PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044241

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044241

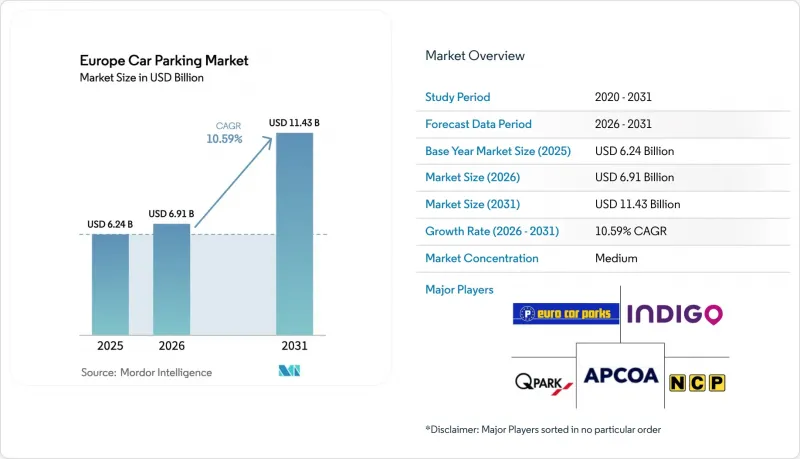

Europe Car Parking - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe Car Parking Market size is projected to expand from USD 6.24 billion in 2025 and USD 6.91 billion in 2026 to USD 11.43 billion by 2031, registering a CAGR of 10.59% between 2026 to 2031.

This rapid expansion reflects the shift from passive space allocation to data-driven, electrification-ready assets that city governments and private operators now treat as a core element of urban-mobility strategy. AFIR-driven retrofit programs, the return of international visitors to pre-pandemic levels, and the roll-out of cashless, sensor-enabled curbside zones have combined to raise pricing power and unlock new revenue streams such as vehicle-to-grid (V2G) aggregation. Competition is intensifying as traditional garage owners defend share through long-term concessions and acquisitions of charging networks, while digital-first platforms convert idle residential and commercial capacity into bookable inventory. Operators that can blend physical capacity with predictive analytics are best placed to capture rising demand linked to e-commerce micro-fulfillment and EV adoption.

Europe Car Parking Market Trends and Insights

Expansion Of EV-Charging Mandates In Parking Facilities

AFIR requires every European parking site with more than 20 spaces to install at least one charger, a rule that entered force in 2024. National add-ons magnify the effect, most notably Germany's GEIG law obliging new non-residential buildings to pre-cable one in every five spaces. Compliance is accelerating joint ventures between garage owners and charge-point specialists such as Allego and Fastned, sharing capital outlays while granting operators upside from energy-services revenue. Utrecht's 500-vehicle V2G pilot proved that parked EVs can supply power during evening peaks, creating a template for monetizing dwell time. Staggered enforcement France extended retrofit deadlines to 2027, Sweden pulled its target forward to 2025 creates a rolling procurement wave that benefits contractors and equipment makers across the decade.

Recovery Of Urban Tourism And Footfall

International arrivals exceeded 2019 levels in 2024, restoring congestion in historic centers and transport hubs. Airports such as Madrid-Barajas introduced 15-minute price recalibration, boosting revenue per space by 12% during Q1 2026. Retailers defend in-store traffic by subsidizing parking, while local ordinances shrinking curb capacity in Barcelona and Amsterdam paradoxically tighten supply even as demand climbs. The rebound is uneven, yet the net effect is upward pressure on hourly rates across tourist corridors.

High Retrofit Costs For EV-Ready Infrastructure

Many multi-story garages built before 2010 lack transformer capacity for multiple fast chargers, forcing pricey grid upgrades that can delay projects up to 18 months. Grant schemes in Italy and Spain reimburse up to 40% of capital outlay but suffer from oversubscription and complex paperwork. Smaller surface-lot owners in secondary cities struggle to finance retrofits without proven utilization forecasts. Software integration mandated by AFIR real-time pricing display and contactless payment acceptance adds further burden to legacy ticketing systems.

Other drivers and restraints analyzed in the detailed report include:

- Municipal Adoption Of Dynamic Pricing And Digital Payments

- Emergence Of Curbside Logistics Hubs For Micro-Fulfillment

- Modal Shift To Active And Shared Mobility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Peer-to-peer platforms digitize fragmented capacity, letting property owners monetize spaces during evenings and weekends. The Europe car parking market size for parking operators stood at 46.23% in 2025, yet platform players are growing 11.26% annually, narrowing the gap. Traditional operators rely on long-term municipal concessions, but users increasingly favor app-based booking that can undercut posted rates by up to 30%. Integration APIs offered by infrastructure vendors now let incumbents white-label their own apps, blurring lines between categories. Compliance questions persist, as some cities classify P2P income as commercial activity subject to tax, while others treat it as ancillary property use, creating a patchwork regulatory map.

Second-order effects include rising adoption of dynamic pricing among asset-heavy operators keen to emulate the elasticity benefits enjoyed by digital rivals. JustPark surpassed 2 million registered spaces in 2025, proving that residential driveways and under-filled office lots can meaningfully expand urban inventory. Infrastructure suppliers capture upside across both camps, selling sensor kits, ANPR cameras, and reservation software that shorten payback periods even as hardware costs fall.

Off-street facilities surface, multi-story, and underground held 63.82% share of the Europe car parking market in 2025. Underground garages command premium tariffs in heritage districts where above-ground development is restricted. However, on-street inventory is forecast to expand at a 11.48% CAGR, faster than any other site class, as sensor grids feed real-time data into municipal pricing engines. London's cashless expansion in 2025 produced a visibility step-change, enabling boroughs to triage curb space among EV charging, bike lanes, and loading bays with minute-level precision.

Operators of private garages respond by upgrading user experience app pre-booking, frictionless entry, and bundled charging to justify higher hourly fees relative to increasingly convenient curb slots. Policies such as Paris' plan to remove 60,000 on-street spaces by 2030 cut raw supply but push per-space revenue higher as scarcity intensifies. The competitive dynamic thus pivots on delivering convenience and ancillary services rather than pure capacity.

The Europe Car Parking Market Report is Segmented by Application Area (Parking Operators and Management Companies, and More), Parking Site (On-Street Parking, Off-Street Parking and More), Technology (Conventional Parking Solutions, and Smart Parking Solutions), End-User Type (Transportation Hubs, Residential Complexes, and Healthcare Facilities), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- APCOA Parking Holdings GmbH

- Indigo Group SA

- Q-Park NV

- Euro Car Parks Limited

- National Car Parks Limited

- JustPark Limited

- ParkingEye Limited

- EasyPark Group AB

- Parkopedia Limited

- NSL Services Group Limited (part of Marston Holdings Limited)

- Interparking SA

- Saba Infraestructuras, S.A.

- Parclick S.L.

- ParkVia Limited

- Flowbird Group SAS (formerly Parkeon)

- Urbiotica S.L.

- Smart Parking Ltd

- ParkBee B.V.

- RingGo Limited

- Tazbell Services Group Limited

- Get My Parking Pvt. Ltd.

- ParkMobile, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of EV-Charging Mandates in Parking Facilities

- 4.2.2 Recovery of Urban Tourism and Footfall

- 4.2.3 Municipal Adoption of Dynamic Pricing and Digital Payments

- 4.2.4 Emergence of Curbside Logistics Hubs for Micro-Fulfilment

- 4.2.5 Integration of Parking Data into City Digital Twins

- 4.2.6 Monetisation of Idle Parking Capacity via Vehicle-to-Grid (V2G) Services

- 4.3 Market Restraints

- 4.3.1 High Retrofit Costs for EV-Ready Infrastructure

- 4.3.2 Modal Shift to Active and Shared Mobility

- 4.3.3 Stricter On-Street Parking Removal in Low-Emission Zones

- 4.3.4 AI-Based Enforcement Errors Triggering Litigation

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Application Area

- 5.1.1 Parking Operators / Management Companies

- 5.1.2 Infrastructure Providers (Hardware and Software)

- 5.1.3 P2P Parking Apps Providers

- 5.2 By Parking Site

- 5.2.1 On-Street Parking

- 5.2.2 Off-Street Parking

- 5.2.2.1 Surface Lots

- 5.2.2.2 Multi-Storey Garages

- 5.2.2.3 Underground Facilities

- 5.3 By Technology

- 5.3.1 Conventional Parking Solutions

- 5.3.2 Smart Parking Solutions

- 5.4 By End-User Type

- 5.4.1 Municipalities and Local Councils

- 5.4.2 Commercial Establishments and Retail

- 5.4.3 Transportation Hubs (Airports, Rail, Ports)

- 5.4.4 Residential Complexes

- 5.4.5 Healthcare Facilities

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Netherlands

- 5.5.7 Belgium

- 5.5.8 Sweden

- 5.5.9 Poland

- 5.5.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 APCOA Parking Holdings GmbH

- 6.4.2 Indigo Group SA

- 6.4.3 Q-Park NV

- 6.4.4 Euro Car Parks Limited

- 6.4.5 National Car Parks Limited

- 6.4.6 JustPark Limited

- 6.4.7 ParkingEye Limited

- 6.4.8 EasyPark Group AB

- 6.4.9 Parkopedia Limited

- 6.4.10 NSL Services Group Limited (part of Marston Holdings Limited)

- 6.4.11 Interparking SA

- 6.4.12 Saba Infraestructuras, S.A.

- 6.4.13 Parclick S.L.

- 6.4.14 ParkVia Limited

- 6.4.15 Flowbird Group SAS (formerly Parkeon)

- 6.4.16 Urbiotica S.L.

- 6.4.17 Smart Parking Ltd

- 6.4.18 ParkBee B.V.

- 6.4.19 RingGo Limited

- 6.4.20 Tazbell Services Group Limited

- 6.4.21 Get My Parking Pvt. Ltd.

- 6.4.22 ParkMobile, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment