PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044262

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044262

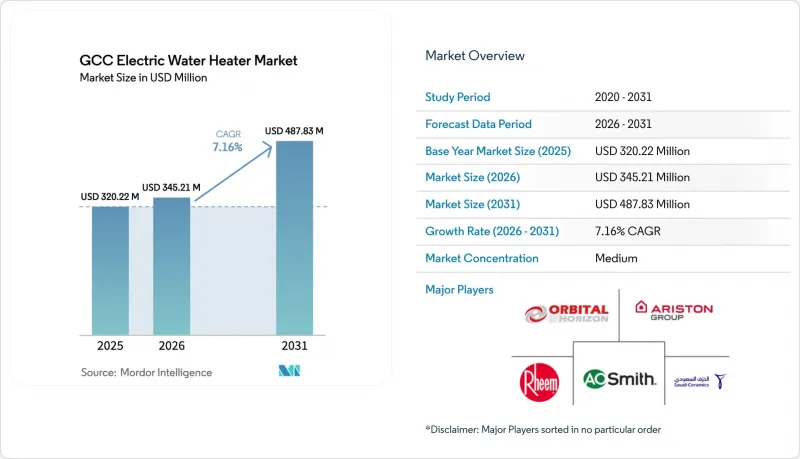

GCC Electric Water Heater - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The GCC electric water heater market size is expected to increase from USD 320.22 million in 2025 to USD 345.21 million in 2026 and reach USD 487.83 million by 2031, growing at a CAGR of 7.16% over 2026-2031.

The GCC electric water heater market benefits from sustained residential construction supported by Saudi Arabia's Sakani program and Dubai's population growth agenda, and it gains further momentum from mandatory efficiency labeling and minimum performance standards that shape product portfolios across storage, tankless, and heat pump categories. As mixed-use, hospitality, and healthcare projects expand, buyers emphasize faster recovery, lower operating costs, and compliance readiness, which lift demand for tankless and heat pump systems, especially in high-rise and retrofit settings. The GCC electric water heater market is also shaped by water-quality constraints in desalination-heavy geographies, which intensify corrosion risks and steer buyers toward anode-free or titanium-anode solutions with longer service intervals. Competitive intensity remains moderate, with global brands scaling local compliance and manufacturing and regional players competing on speed, service, and cost alignment with GCC standards.

GCC Electric Water Heater Market Trends and Insights

Housing Program-Fueled Residential Construction

Saudi Arabia's Sakani program has provided support to more than one million families since the launch of Vision 2030, lifting national homeownership above 60% by 2022 and targeting 70% by 2030. These policy outcomes sustain demand for mid-range electric storage water heaters in 30-80-liter brackets as financing translates into steady handovers and fit-outs in major cities. In the UAE, contracts awarded between 2020 and August 2025 totaled USD 328.7 billion, with residential real estate accounting for 28% of the construction pipeline, supporting recurring demand in apartments and villas. Mixed-use developments that represent a significant share of future projects are shifting specifications toward compact tankless and heat pump units that align with Estidama, Al Sa'fat, and Barjeel frameworks in local markets. A UAE high-rise case study using Ariston heat pump water heaters lowered connected electrical load from 508.8 kW to 178.4 kW, reducing connection fees by AED 660,800 (USD 179,932) and annual running costs by AED 193,000 (USD 52,553).

Mandatory Energy-Efficiency Labeling and Standards

Mandatory energy-efficiency labeling and standards across GCC countries are driving demand for advanced electric water heaters. Regulatory frameworks encourage manufacturers to develop energy-efficient models, while consumers increasingly prefer labeled products to reduce electricity costs. These policies support sustainability goals and accelerate the replacement of older, inefficient systems with compliant, high-performance alternatives. SASO 2884:2017/AMD4:2021 mandates energy labels for electric storage and instantaneous water heaters, including declared load profiles and consistent testing parameters for compliance and market entry. GSO 2770:2024, approved at the GCC level, establishes Minimum Energy Performance Standards for electric storage, instantaneous, heat pump, and solar heaters up to 70 kW and 2,000 liters, harmonizing thresholds across member states while allowing national variations where applicable. The unified GCC Conformity Mark framework requires the GSO Conformity Tracking Symbol and digital traceability through the Hazm platform, ensuring that higher-risk electrical products complete type examination and factory audits before placement on the market. These requirements accelerate the phaseout of sub-MEPS inventory and reward brands that invest in accredited testing and in-region compliance workflows. Third-party testing scope expansions, such as Oman's DGSM accreditation with UL Solutions Demko A/S in late 2025, reinforce enforcement and shorten approval cycles as suppliers update portfolios. In practice, these rules shift purchasing toward higher-efficiency storage models, tankless systems with improved controls, and heat pumps in retrofit and new-build contexts.

Competition from Gas and Solar Thermal Alternatives in Select Projects

Pipeline networks and legacy project designs can favor gas-fired hot water in compounds and facilities where local tariffs, existing infrastructure, or engineered standards already tilt the balance against fully electric systems. Rooftop solar thermal systems mandated for Dubai villas reinforce this restraint in low-rise detached housing, where collectors fit well on available roof space. Developers targeting net-zero or near-zero operating profiles sometimes specify hybrid architectures that rely on thermal collection as a primary source with an electric boost for reliability. Under certain design and tariff assumptions, the lifecycle economics of solar thermal can be competitive in villas with favorable orientation and minimal shading. Electric systems retain an edge in high-rise and multi-family buildings due to roof area constraints per dwelling and in retrofits where structural conditions limit collector installation.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Hotel and Healthcare Pipeline Boosting Commercial Demand

- Replacement Demand from the Aging Installed Base of Storage Heaters

- Higher Upfront Cost for HPWH and Tankless vs. Basic Storage Units

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Storage tank systems accounted for 68.76% of revenue in 2025 within the GCC electric water heater market, while tankless models are forecast to post an 8.18% CAGR through 2031 from a smaller base. Storage remains prevalent due to lower first cost, installer familiarity, and compatibility with existing infrastructure across new-build and retrofit contexts. Tankless models grow faster where space is tight, recovery speed is important, and standby losses need reduction in luxury apartments and hospitality suites. Modular tankless architectures enable cascaded installations to meet peak loads with better utilization, which supports uptake in commercial kitchens and spas that need swift temperature stabilization. Leading portfolios adapt to Gulf water chemistry with anti-scale features and corrosion control that preserve efficiency and extend service intervals in hard-water conditions.

Heat pump water heaters create a premium subcategory within storage, where COP 3+ performance and smart controls help reduce operating costs in villas and high-end retrofits. Brands are also aligning product testing with SASO Energy Efficiency Labeling and the GCC G-Mark system to streamline approvals under unified compliance workflows. In-region manufacturing investments and regional service networks shorten lead times and enable faster product updates that reflect evolving standards. This execution focus supports broader choice across storage, tankless, and heat pump systems in the GCC electric water heater industry, encouraging channel partners to match product features to project requirements.

Medium-sized units around 50-100 liters held a 47.73% share in 2025, reflecting the capacity range favored in villas and two-to-three-bedroom apartments across major GCC cities. Small-capacity units under 50 liters are projected to grow at a 7.26% CAGR as densification adds studios and one-bedroom apartments near transit and employment centers. Large-capacity formats above 100 liters serve multi-bathroom villas, hospitality, and healthcare use cases that demand redundancy or extended draw profiles. Tankless products disrupt traditional capacity definitions by shifting sizing from stored volume to flow rate, which allows designers to right-size systems based on peak fixtures and diversity factors.

Water chemistry is a factor in effective capacity over time, as scale can reduce flow and heat transfer in high-TDS zones unless mitigated by product design. Anode-free and titanium-anode designs aim to preserve performance throughout service life, which sustains rated output in homes and small commercial sites. As unit mixes evolve with housing formats, contractors emphasize serviceability and total lifecycle cost to recommend capacity categories that balance draw patterns and energy savings within the GCC electric water heater industry.

The GCC Electric Water Heater Market Report is Segmented by Product Type (Storage Tank Water Heaters, and Tankless Water Heaters), Capacity (Small, Medium, and Large), End-Users (Commercial, and Residential), Distribution Channels (Online, and Offline), and Geography (Saudi Arabia, United Arab Emirates, Kuwait, Oman, Qatar, and Bahrain). Market Forecasts are Provided in Terms of Value (USD Billion).

List of Companies Covered in this Report:

- Ariston Group

- A. O. Smith MEA

- Rheem Middle East & Africa

- Bosch Home Comfort (Thermotechnology)

- Stiebel Eltron

- Haier

- Midea

- Groupe Atlantic

- Thermex

- Jaquar Group

- Saudi Ceramics Company

- Orbital Horizon

- National Heaters Industries

- Noritz

- TESY

- Dana Water Heaters & Coolers Factory

- Everhot (Al Huraiz Group)

- Ferroli

- Milano

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Housing program-fueled residential construction (KSA, UAE)

- 4.2.2 Mandatory energy-efficiency labeling and standards (SASO/MoIAT/GSO)

- 4.2.3 Rapid hotel and healthcare pipeline boosting commercial demand

- 4.2.4 Replacement demand from aging installed base of storage heaters

- 4.2.5 Heat-pump and smart controls reducing operating costs (retrofits)

- 4.2.6 Electrification of DHW in light industry and mixed-use projects

- 4.3 Market Restraints

- 4.3.1 Competition from gas/solar thermal alternatives in select projects

- 4.3.2 Higher upfront cost for HPWH/tankless vs. basic storage units

- 4.3.3 Water-quality (scale/corrosion) increasing maintenance costs

- 4.3.4 Skilled installer availability uneven across GCC micro-markets

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts

- 5.1 By Product Type

- 5.1.1 Storage Tank Water Heaters

- 5.1.2 Tankless Water Heaters

- 5.2 By Capacity

- 5.2.1 Small

- 5.2.2 Medium

- 5.2.3 Large

- 5.3 By End Users

- 5.3.1 Commercial

- 5.3.2 Residential

- 5.4 By Distribution Channels

- 5.4.1 Online

- 5.4.2 Offline

- 5.5 By Geography

- 5.5.1 Saudi Arabia

- 5.5.2 United Arab Emirates

- 5.5.3 Kuwait

- 5.5.4 Oman

- 5.5.5 Qatar

- 5.5.6 Bahrain

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Ariston Group

- 6.4.2 A. O. Smith MEA

- 6.4.3 Rheem Middle East & Africa

- 6.4.4 Bosch Home Comfort (Thermotechnology)

- 6.4.5 Stiebel Eltron

- 6.4.6 Haier

- 6.4.7 Midea

- 6.4.8 Groupe Atlantic

- 6.4.9 Thermex

- 6.4.10 Jaquar Group

- 6.4.11 Saudi Ceramics Company

- 6.4.12 Orbital Horizon

- 6.4.13 National Heaters Industries

- 6.4.14 Noritz

- 6.4.15 TESY

- 6.4.16 Dana Water Heaters & Coolers Factory

- 6.4.17 Everhot (Al Huraiz Group)

- 6.4.18 Ferroli

- 6.4.19 Milano

7 Market Opportunities & Future Outlook

- 7.1 Retrofit heat-pump DHW packages for villas, hotels, and staff housing (50-75% energy savings potential)

- 7.2 Made-in-GCC storage portfolios (KSA/UAE) enabling faster delivery, SASO/MoIAT compliance, and cost control

- 7.3 B2B e-procurement/contractor portals bundling SASO/ESMA-certified heaters with installation and AMCs