PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044263

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044263

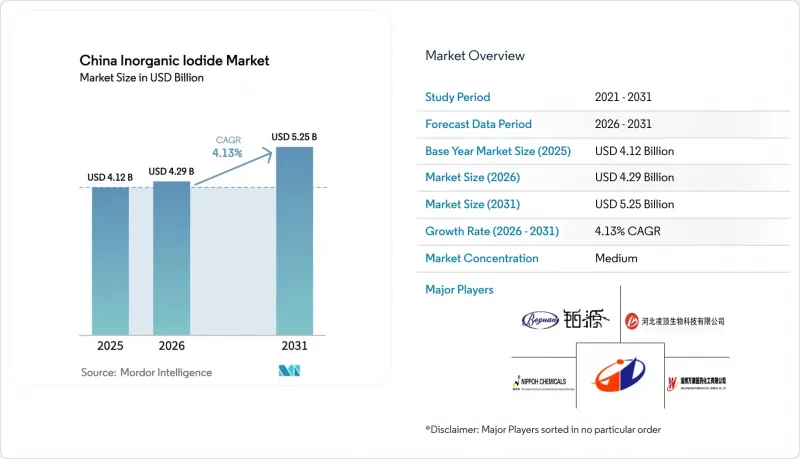

China Inorganic Iodide - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The China Inorganic Iodide Market size is projected to expand from USD 4.12 billion in 2025 and USD 4.29 billion in 2026 to USD 5.25 billion by 2031, registering a CAGR of 4.13% between 2026 and 2031.

Expansion is paced by pharmaceutical demand for potassium iodide, the migration of display-panel incentives that support optical-grade iodides, and government restocking of nuclear-preparedness tablets. Upstream control of 20% of global API output and about 80% of key starting materials keeps domestic converters well placed to absorb feedstock volatility while maintaining capacity utilization at chemical parks along the Bohai Rim and the Yangtze River Delta. Structural headwinds stem from Chile-centric iodine sourcing, LCD-to-OLED substitution, and tighter environmental standards that pressure smaller plants to relocate or shut down. Inventory cycles rather than feedstock swings currently drive domestic spot prices, underscoring the importance of working-capital discipline and long-term supply contracts.

China Inorganic Iodide Market Trends and Insights

Surging API Output Fueling Iodide Demand in China's Pharma Clusters

Converters anchored in Shandong and Jiangsu chemical parks benefit from integrated utilities and regulatory moats created by China's 18% share of European Pharmacopoeia certificates, ensuring that potassium iodide and hydroiodic acid track API growth rather than GDP. The removal of tax rebates on certain fermentation feedstocks in 2024 raised costs, yet margin resilience persists because contrast media and thyroid drugs absorb price swings. High-purity iodides therefore enjoy demand insulation when commodity grades soften.

Expansion of Industrial Feed Mills Boosting Iodide-Fortified Feed Premixes

Animal nutrition accounts for roughly 7% of global iodine use and gains ground as salt-reduction campaigns lower dietary iodine intake. Consolidating feed mills in Shandong and Henan are shifting from crude additives to pharmaceutical-grade potassium iodide, backed by Ministry of Agriculture residue limits that favor ISO 9001-certified suppliers. Because premix contracts turn over slowly, volume growth materializes over multiple seasons, yet intensified livestock farming locks in a durable vibration for the China Inorganic Iodide market.

Health-Related Side-Effects Triggering Tighter Use-Level Caps

WHO's updated contraindications highlight thyroid risks among the elderly, prompting Chinese regulators to examine consumer-goods iodine content and possibly list certain iodides as priority-control substances. Jiangsu's draft pollutant plan outlines audits and potential phase-outs, raising compliance costs for smaller converters. Firms holding comprehensive toxicology files and ISO 9001 certification are positioned to retain access, while non-compliant plants risk exit, shaving a fraction from the China Inorganic Iodide market CAGR.

Other drivers and restraints analyzed in the detailed report include:

- Re-stocking of KI Tablets for Nuclear-Emergency Preparedness

- Rising Adoption of KI Heat Stabilizers in China's Nylon and Engineering Plastics

- Volatile Imported Iodine Prices Squeezing Producer Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Potassium iodide held 38.76% China Inorganic Iodide market share in 2025, capturing demand from thyroid treatments, feed fortification, and civil-defense tablets. Hydroiodic acid is projected to rise at a 5.18% CAGR through 2031 on the back of acetic-acid carbonylation catalysts and graphene reduction, pushing its slice of the China inorganic iodide market size upward. Sodium iodide, potassium iodate, lithium iodide, and silver iodide together fill niche segments such as scintillator crystals and cloud-seeding agents. The decisive factor is purity: ultra-high-grade lots command 3-5 times commodity pricing, shielding earnings when bulk prices weaken.

Second-generation catalytic reduction and electrodialysis purification lower environmental overhead and match Jiangsu pollutant-governance demands, allowing compliant converters to raise output without breaching discharge limits. Because these technologies cut sulfur waste and heavy-metal residues, they also improve ESG profiles sought by multinational pharma buyers, reinforcing the stickiness of imports from the China Inorganic Iodide market.

The China Inorganic Iodide Market is Segmented by Product (Potassium Iodide, Sodium Iodide, Potassium Iodate, Hydroiodic Acid, and Other Products) and by Application (Animal Feed and Nutraceuticals, Pharmaceuticals and Medical, Optical Polarizing Films, Industrial Chemicals, and Other Applications). The Report Offers Market Size and Forecasts for the China Inorganic Iodide Market in Value (USD) for all the Above Segments.

List of Companies Covered in this Report:

- AJAY SQM

- Deep Water Chemicals

- Godo Shigen Co., Ltd

- Hebei Lingding Biotechnology Co., Ltd

- Hebei Yime New Material Technology Co., Ltd

- Independent Iodine China Ltd

- Jiangsu Kaihuida New Material Technology Co., Ltd

- Jiangxi Shengdian S&T Co., Ltd

- Merck KGaA

- Nanjing Taiye Chemical Industry Co., Ltd.

- Nippoh Chemicals Co., Ltd

- Qingdao Gimhae Iodide Chemical Co., Ltd

- Shandong Boyuan Pharmaceutical & Chemical Co., Ltd

- Sqm S.A.

- Tai'an Havay Group Co., Ltd.

- Toho Earthtech, Inc.

- Zibo Anquan Chemical Co., Ltd.

- Zibo Wankang Pharmaceutical & Chemical Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging API output fuelling iodide demand in China's pharma clusters

- 4.2.2 Expansion of industrial feed mills boosting iodide-fortified feed premixes

- 4.2.3 Re-stocking of KI tablets for nuclear-emergency preparedness

- 4.2.4 Rising adoption of KI heat stabilisers in China's nylon and engineering plastics

- 4.2.5 Government incentives for LCD fabs sustaining polarising-film iodide consumption

- 4.3 Market Restraints

- 4.3.1 Health-related side-effects triggering tighter use-level caps

- 4.3.2 Volatile imported iodine prices squeezing producer margins

- 4.3.3 LCD-to-OLED migration eroding iodide demand from display sector

- 4.4 Value Chain Analysis

- 4.5 Regulatory Analysis

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products and Services

- 4.6.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Potassium Iodide

- 5.1.2 Sodium Iodide

- 5.1.3 Hydroiodic Acid

- 5.1.4 Potassium Iodate

- 5.1.5 Other Products

- 5.2 By Application

- 5.2.1 Animal Feed and Nutraceuticals

- 5.2.2 Pharmaceuticals and Medical

- 5.2.3 Optical Polarizing Films

- 5.2.4 Industrial Chemicals

- 5.2.5 Other Applications

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 AJAY SQM

- 6.4.2 Deep Water Chemicals

- 6.4.3 Godo Shigen Co., Ltd

- 6.4.4 Hebei Lingding Biotechnology Co., Ltd

- 6.4.5 Hebei Yime New Material Technology Co., Ltd

- 6.4.6 Independent Iodine China Ltd

- 6.4.7 Jiangsu Kaihuida New Material Technology Co., Ltd

- 6.4.8 Jiangxi Shengdian S&T Co., Ltd

- 6.4.9 Merck KGaA

- 6.4.10 Nanjing Taiye Chemical Industry Co., Ltd.

- 6.4.11 Nippoh Chemicals Co., Ltd

- 6.4.12 Qingdao Gimhae Iodide Chemical Co., Ltd

- 6.4.13 Shandong Boyuan Pharmaceutical & Chemical Co., Ltd

- 6.4.14 Sqm S.A.

- 6.4.15 Tai'an Havay Group Co., Ltd.

- 6.4.16 Toho Earthtech, Inc.

- 6.4.17 Zibo Anquan Chemical Co., Ltd.

- 6.4.18 Zibo Wankang Pharmaceutical & Chemical Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment