PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044264

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044264

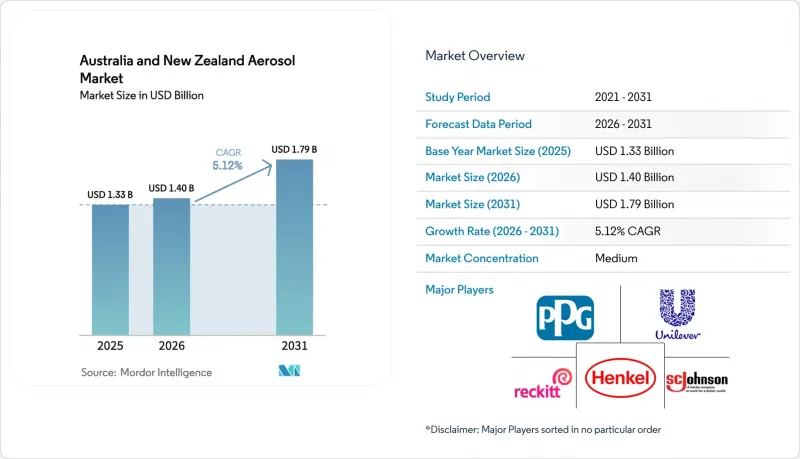

Australia And New Zealand Aerosol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Australia and New Zealand Aerosol Market size is expected to increase from USD 1.33 billion in 2025 to USD 1.40 billion in 2026 and reach USD 1.79 billion by 2031, growing at a CAGR of 5.12% over 2026-2031.

Brand owners are switching from steel to lighter-weight aluminum cans to satisfy retailer recycled-content mandates, while medical inhaler demand is rising under new clinical guidelines that favor anti-inflammatory reliever therapy. Retail private-label lines now specify minimum recyclability and carbon scores, making packaging choices a competitive lever. Propellant policy is equally influential; Australia's HFC phase-down caps tighten again in 2026, accelerating the shift to hydrocarbon blends and opening a technology window for low-GWP alternatives. Meanwhile, construction-related spray-paint consumption benefits from infrastructure outlays in New South Wales, Victoria, and Queensland, albeit with margins pressured by volatile aluminum and tinplate prices linked to global tariff regimes.

Australia And New Zealand Aerosol Market Trends and Insights

Rising Eco-Friendly, Low-GWP Propellant Adoption

Australia's HFC quota falls from 5.25 million tons CO2-e in 2024-2025 to 4.25 million tons CO2-e for 2026-2027, restricting HFC-134a and HFC-152a supply and nudging formulators toward butane, isobutane, and propane blends. CSIRO monitoring shows HFC-152a growth slowing to 1.2% annually, an early sign of market substitution. Dove Advanced Care deodorant now highlights hydrocarbon propellants and a recyclable metal can, aligning with Woolworths' 52% average recycled-content target. Parallel regulatory moves in refrigeration hint at progressively tighter controls that will further squeeze HFC availability. Pharmaceutical inhaler platforms remain an outlier, yet early pilots of dry-powder devices suggest future momentum toward propellant-free options.

Gen-Z-Focused Male Grooming Aerosol Launches

Unilever's February 2026 Rexona RIVALS line deploys QR-code gamification tied to local sports, leveraging Woolworths' 25.7 million weekly shoppers for rapid trial. The 220 ml cans command a premium AUD 10.50 shelf price but sell through quickly during match weekends. Limited-edition cycles shorten development timelines, enabling frequent design refreshes without long-run tooling costs. Retail scorecards oblige aluminum formats with verifiable recycled content, so suppliers integrate mass-balance approaches to hit the 60% threshold due by 2025. Younger consumers respond to interactive packaging and sustainability cues, a mix that drives repeat purchase and lifts category value.

Stricter 2027 VOC-Limit Compliance Costs

The United States Environmental Protection Agency (EPA) extended the aerosol-coatings VOC deadline to January 2027, but Australian and New Zealand exporters must still retool formulas, run shelf-life trials, and absorb certification fees. Smaller fillers lack in-house toxicology labs, so they outsource, lengthening time-to-market. In parallel, domestic Safe Work Australia exposure limits only partly overlap with the EPA's reactivity-based caps, adding paper-chase overhead. The scheduling clash with HFC quota cuts compounds compliance budgeting.

Other drivers and restraints analyzed in the detailed report include:

- Uptick in Metered-Dose Inhalers for Asthma Care

- Construction Boom Driving Quick-Dry Spray Paints

- Volatile Aluminum and Tinplate Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Steel retained 58.28% of Australia and New Zealand aerosol market share in 2025, owing to cost-effective supply into insecticides and technical sprays. Yet aluminum's 5.27% CAGR through 2031 signals a structural pivot in the Australia and New Zealand aerosol market as retailers enforce packaging scorecards that favor lighter, endlessly recyclable metals. Confirming the trend, Dove Advanced Care deodorant now advertises a recyclable-metal can and hydrocarbon propellants to meet low-GWP goals.

Volatile pricing clouds the outlook; the January 2026 Midwest Premium spike fed through to Asia-Pacific offers within days, testing converter margins. Even so, brand owners keep specifying aluminum for premium deodorant, shaving, and hair-styling lines to differentiate on the shelf. Steel cans remain dominant in budget cleaners and paints, making the Australia and New Zealand aerosol market size sensitive to commodity swings across both substrates.

The Australia and New Zealand Aerosol Market Report is Segmented by Material (Steel, Aluminium, and Other Materials), Application (Automotive, Personal Care, Food Products, Herbicide, Household Products, Insecticide, Industrial and Technical, Medical, Paint and Coatings, and Other Applications), and Geography (Australia and New Zealand). The Report Offers Market Size and Forecasts in Value (USD) for all the Above Segments.

List of Companies Covered in this Report:

- Aerosolve

- Akzo Nobel N.V.

- Ball Corporation

- BASF

- Chemz Limited

- Colep Consumer Products

- Crown

- Damar

- Henkel AG & Co. KGaA

- Honeywell International Inc.

- Liquid Engineering NZ

- MMP Industrial

- PPG Industries Inc.

- Reckitt Benckiser Group plc

- S.C. Johnson & Son Inc.

- The Sherwin-Williams Company

- Unilever plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising eco-friendly, low-GWP propellant adoption

- 4.2.2 Gen-Z-focused male grooming aerosol launches

- 4.2.3 Uptick in metered-dose inhalers for asthma care

- 4.2.4 Construction boom driving quick-dry spray paints

- 4.2.5 Super-market private-label aerosol cleaners surge

- 4.3 Market Restraints

- 4.3.1 Stricter 2027 VOC-limit compliance costs

- 4.3.2 Volatile aluminium and tinplate prices

- 4.3.3 Retailer carbon-scorecard penalties on aerosols

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Material

- 5.1.1 Steel

- 5.1.2 Aluminium

- 5.1.3 Other Materials

- 5.2 By Application

- 5.2.1 Automotive

- 5.2.2 Personal Care

- 5.2.3 Food Products

- 5.2.4 Herbicide

- 5.2.5 Household Products

- 5.2.6 Insecticide

- 5.2.7 Industrial and Technical

- 5.2.8 Medical

- 5.2.9 Paint and Coatings

- 5.2.10 Other Applications

- 5.3 By Geography

- 5.3.1 Australia

- 5.3.2 New Zealand

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Aerosolve

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Ball Corporation

- 6.4.4 BASF

- 6.4.5 Chemz Limited

- 6.4.6 Colep Consumer Products

- 6.4.7 Crown

- 6.4.8 Damar

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Honeywell International Inc.

- 6.4.11 Liquid Engineering NZ

- 6.4.12 MMP Industrial

- 6.4.13 PPG Industries Inc.

- 6.4.14 Reckitt Benckiser Group plc

- 6.4.15 S.C. Johnson & Son Inc.

- 6.4.16 The Sherwin-Williams Company

- 6.4.17 Unilever plc

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment