PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044283

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044283

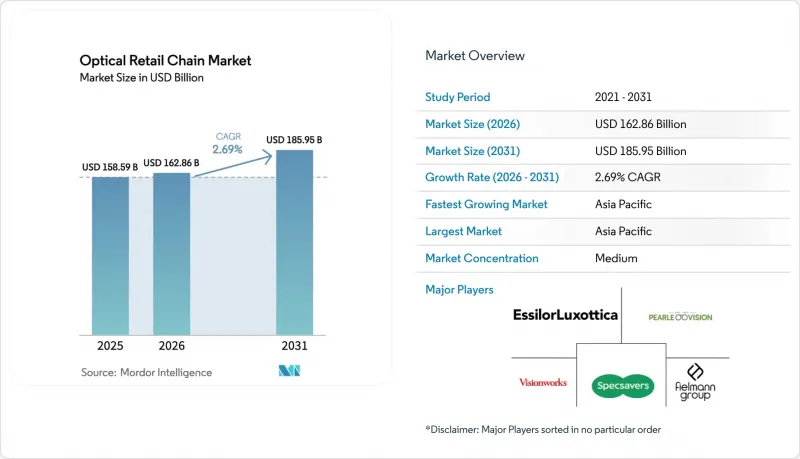

Optical Retail Chain - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Optical Retail Chain market size was USD 158.59 billion in 2025, is projected at USD 162.86 billion in 2026, and is forecast to reach USD 185.95 billion by 2031 at a 2.69% CAGR.

Demand and delivery models are shifting as myopia becomes a global public health issue, while tariffs and online disruptors compress margins for incumbents. Chains are investing in AI-enabled diagnostics, smart eyewear attachments, and omnichannel logistics to protect traffic and capture higher-value prescriptions. Premiumization holds even as unit volumes soften, as the United States' spending reached USD 69.5 billion in 2025 despite volume declines, reflecting trade-up behavior toward progressive lenses and specialty solutions. Leading platforms that link retail, lens technology, and services are scaling faster than mid-tier independents that face greater tariff exposure and weaker negotiating leverage with suppliers. Hardware and software integration is now a core differentiator, as shown by double-digit growth and strong cash generation at vertically integrated leaders that monetize AI glasses, myopia management, and subscription services tied to in-store expertise.

Global Optical Retail Chain Market Trends and Insights

Rising Incidence of Myopia Among Gen-Z Consumers

Global myopia prevalence has accelerated, with 2025 levels reaching 34% of the population and long-range projections indicating near half of the world population could be myopic by 2050, with East Asia as the epicenter of growth. China's urban teens already post very high prevalence, which sustains recurring demand for more frequent prescription updates and higher-complexity lenses. This demand shift has elevated myopia management to a core growth vector for chains that can support clinical fitting and follow-up across large store networks. Recent research shows a substantial rise in myopia prevalence among children and adolescents, with data from China indicating over half of urban school-aged youth are affected, and projections suggesting that myopia will continue rising sharply through mid-century. Myopia rates have increased markedly over the past decades across global youth, with systematic reviews estimating that roughly one-third of children and teens are now nearsighted, and prevalence is expected to approach 40% by 2050. These trends reflect lifestyle and environmental factors driving the early onset and progression of myopia among younger generations, including Gen-Z. The growing burden of myopia is driving demand for corrective solutions, such as prescription eyewear and optical care services. The combination of rising prevalence and an expanding portfolio of regulated solutions now supports a durable uplift in the Optical Retail Chain market, where clinical programs can be delivered consistently at scale.

Growing Elderly Demographic Driving Presbyopia Demand

Presbyopia remains a near-universal condition by middle age and is driving steady demand for progressive, multifocal, and photochromic lenses within the Optical Retail Chain market. Product mix upgrades are visible in retailer disclosures, including premium progressives that lifted revenue per customer and supported resilience against macro softness. EssilorLuxottica's lens portfolio momentum in 2025 featured advanced progressives and next-generation photochromics across EMEA, reinforcing the shift toward higher value prescriptions within chain retail. Adjacent opportunities are emerging at the intersection of audiology and vision, supported by the company's Nuance Audio hearing aid glasses, which received United States and EU clearances in 2025 and reached broad retail distribution by year-end. Retailers that couple progressive lenses with integrated care journeys and cross-category add-ons are positioned to capture more lifetime value per patient encounter and create recurring upgrade cycles. Disclosures from leading United States eyewear retailers also show sustained customer adoption of premium lens tiers, validating the presbyopia-led mix shift in 2025.

Margin Compression From Online-Only Competitors

Direct-to-consumer operators sustain low entry prices and lean supply chains, pressuring legacy chains on headline price points and shipping costs. Warby Parker's reporting showed gross margin variability in 2025 driven by tariffs, category mix, and logistics, underscoring how input costs and channel shifts feed into pricing decisions. Subscription models, including omnichannel formats in which members receive exchanges and bundled services, expanded in 2025 and lifted average order values for operators that aligned store services with digital replenishment. Competitive dynamics remain intense, as United States peers highlighted industry rivalry and structural cost pressures in their risk disclosures while targeting mix upgrades into premium lens categories to stabilize margins. The net effect is a bifurcating Optical Retail Chain market, where scale, vertical integration, and service bundling help offset pressures squeezing mid-tier, price-only propositions.

Other drivers and restraints analyzed in the detailed report include:

- Strategic Omnichannel Investments by Optical Retail Chains

- Expanding Consumer Spending Power Across APAC

- Supply Chain Disruptions in Acetate and Metal Inputs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Spectacles accounted for 55.72% of the Optical Retail Chain market in 2025, and contact lenses are projected to grow at an 8.01% CAGR through 2031, driven by the adoption of daily disposables and subscription models. Retailers continue to report lens mix upgrades to premium progressives and advanced coatings that support resilient ticket values, even as traffic normalizes. Warby Parker disclosed a rising mix of contact lenses as part of its broader assortment, which supported top-line momentum while adding cost complexity that management closely monitored. EssilorLuxottica's direct channels have become important for sunglasses and smart eyewear journeys, with store staff enabling prescription attachment and photochromic conversions at scale. Myopia management lenses posted strong growth in 2025 across the company's Stellest portfolio, reflecting greater clinician training and parent awareness in markets with high pediatric prevalence.

The Optical Retail Chain market is also seeing targeted private-label innovation that enhances margins and control over lead times. Mister Spex reported higher margins from its SpexPro private-label lenses and continued to grow its share of prescription glasses in Germany in 2025, aided by omnichannel service programs that encourage in-store fitting and follow-up. Sunglasses remain an important gateway into the category, with premium banners like Sunglass Hut leveraging both online and store-based curation and seasonal drops to maintain flow. The Vision Council's 2025 report confirms consumer trade-up dynamics in the United States, where spending rose even as volumes softened, reinforcing the shift toward higher-quality frames and lenses. Operators that combine differentiated assortment with clinical programs for myopia and presbyopia are capturing a larger share of the category's durable value pools. As more retailers refine inventory depth around hero SKUs and tie customization to store labs, conversion into premium lenses is likely to remain a central lever for growth in the Optical Retail Chain market.

The Optical Retail Chain Market is Segmented by Product (Spectacles, Sunglasses, and Contact Lenses), Gender (Men, Women, and Unisex), Distribution Channel (Offline, Online), and Geography (Asia-Pacific, North America, Europe, South America, and the Middle East & Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led with 42.31% of the Optical Retail Chain market share in 2025 and is projected to expand at a 6.86% CAGR through 2031, powered by underpenetrated city tiers in India and China, fast-rising disposable incomes, and aggressive omnichannel rollouts. Myopia management is a structural tailwind in Greater China, where EssilorLuxottica's Stellest portfolio grew strongly and where new iterations of the lens family and related smart eyewear are expanding addressable pediatric segments. Japan's aging population supports premium lens and audiology convergence, reflected in large national chains that have broadened their formats and invested in technology-led shopping experiences. JINS opened a flagship in Tokyo's Ginza with a digital-first journey and continues to scale across Asia with standardized processes that compress exam-to-delivery times. Regional champions are also expanding across Southeast Asia and the Middle East through owned stores and partnerships, creating a multi-country platform layer that can support faster product diffusion and unified service standards. The Optical Retail Chain market in APAC will likely remain the primary growth engine as clinical capacity, mobile commerce, and in-store technology penetrate beyond tier 1 cities.

North America remained the second-largest region by value, with the United States optical sector reaching USD 69.5 billion in 2025 despite volume declines, pointing to consumers trading up to premium prescriptions and lens technologies. Average exam costs rose year over year, reflecting greater diagnostic complexity and screening for age-related conditions, including presbyopia and glaucoma. EssilorLuxottica reported growth in North America, with smart eyewear programs and premium banners delivering peak sales days and strong comps in late 2025. Warby Parker expanded to 313 stores by Q3 2025 and announced a partnership with Google to develop AI-powered glasses, backed by substantial product development funding, signaling deeper convergence of optical retail and wearables. National Vision ended a legacy partnership, rebalanced its footprint, and outlined a transformation plan to 2030 that targets mix shifts into premium lenses and managed care segments while aiming for margin expansion.

Europe demonstrated resilience through localized sourcing, premium positioning, and disciplined omnichannel models in the Optical Retail Chain market. EssilorLuxottica's EMEA operations delivered strong results in 2025, with double-digit growth in both professional solutions and direct-to-consumer activity, aided by continued integration of former GrandVision banners and higher penetration of EssilorLuxottica's frames and lenses. Mister Spex consolidated its German core market in 2025, closed non-core international stores, and improved store-level margins while expanding service-linked products that support repeat traffic. The EU advanced proposals in late 2025 to simplify medical device rules and promote innovation, which should, over time, reduce compliance friction for chains with strong regulatory systems. Aging demographics in several European countries continue to support presbyopia segments, favoring retailers that can deliver advanced progressives and hearing-vision hybrids tied to clinical screening. The region's pathway shows steady mid-single-digit growth rather than outsized surges, anchored by service-led differentiation and subscription models that drive loyalty in mature markets.

- EssilorLuxottica

- GrandVision

- Specsavers

- Vision Express

- LensCrafters

- Sunglass Hut

- Visionworks

- MyEyeDr.

- Warby Parker

- Costco Optical

- Walmart Vision Center

- For Eyes

- Apollo Optik

- Fielmann

- Mister Spex

- JINS

- Lenskart

- Owndays

- Optical Superstore

- Ace & Tate

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing myopia prevalence among Gen-Z

- 4.2.2 Aging population boosting presbyopia sales

- 4.2.3 Omnichannel retail investments by chains

- 4.2.4 Rising disposable income in APAC

- 4.2.5 Under-penetrated tier-3 cities in India & China

- 4.2.6 AI-powered vision-screening kiosks in stores

- 4.3 Market Restraints

- 4.3.1 Margin pressure from online-only players

- 4.3.2 Supply-chain volatility in acetate & metals

- 4.3.3 Regulatory caps on reimbursement in EU

- 4.3.4 Counterfeit lenses in emerging markets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product

- 5.1.1 Spectacles

- 5.1.2 Sunglasses

- 5.1.3 Contact Lenses

- 5.2 By Gender

- 5.2.1 Men

- 5.2.2 Women

- 5.2.3 Unisex

- 5.3 By Distribution Channel

- 5.3.1 Offline

- 5.3.2 Online

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Peru

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.3.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 India

- 5.4.4.2 China

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 South-East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, Philippines)

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East & Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East & Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 EssilorLuxottica

- 6.4.2 GrandVision

- 6.4.3 Specsavers

- 6.4.4 Vision Express

- 6.4.5 LensCrafters

- 6.4.6 Sunglass Hut

- 6.4.7 Visionworks

- 6.4.8 MyEyeDr.

- 6.4.9 Warby Parker

- 6.4.10 Costco Optical

- 6.4.11 Walmart Vision Center

- 6.4.12 For Eyes

- 6.4.13 Apollo Optik

- 6.4.14 Fielmann

- 6.4.15 Mister Spex

- 6.4.16 JINS

- 6.4.17 Lenskart

- 6.4.18 Owndays

- 6.4.19 Optical Superstore

- 6.4.20 Ace & Tate

7 Market Opportunities & Future Outlook

- 7.1 Seamless tele-optometry integration across stores

- 7.2 Subscription-based eyewear replacement programs