PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061503

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061503

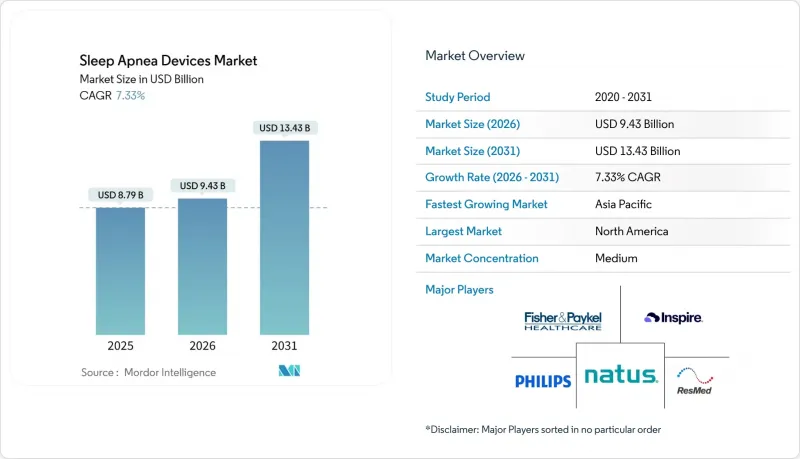

Sleep Apnea Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the sleep apnea devices market size is expected to increase from USD 8.79 billion in 2025 to USD 9.43 billion in 2026 and reach USD 13.43 billion by 2031, growing at a CAGR of 7.33% over 2026-2031.

This report is Segmented by Type (Diagnostic Devices (Polysomnography Systems (PSG), and More)), Therapeutic Devices (Positive Airway Pressure (PAP) Devices, Oxygen Therapy Devices, and More), End-User (Hospitals, Home Care Setting, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Sleep Apnea Devices Market Trends and Insights

Rising Global OSA Prevalence Tied to Obesity

The United States counted about 61 million OSA cases in 2025 and is projected to reach 77 million by 2050, driven by population aging and better screening rather than obesity alone. Middle Eastern and North African nations display steeper curves as urban lifestyles and type 2 diabetes rates climb. Obesity remains the strongest modifiable risk factor for obstructive sleep apnea (OSA), and epidemiologic curves for both conditions rise in tandem. In morbidly obese surgical candidates, OSA prevalence reaches 95% for body-mass-index levels above 60. Yet of the 30 million United States adults estimated to have sleep apnea, only 6 million carry a formal diagnosis. This latent clinical need underpins sustained demand for diagnostic devices, remote monitoring accessories, and long-term therapy solutions. Insurers increasingly acknowledge the downstream economic burden of untreated apnea, such as hypertension-related admissions, making coverage expansion politically and fiscally attractive.

Expanded Insurance Coverage for PAP & Oral Appliances

Reimbursement reforms now embrace a broader toolkit of treatments. In the United States, the Centers for Medicare & Medicaid Services reimburse continuous positive airway pressure (CPAP) initiated by either in-lab polysomnography or qualified home tests. Coverage further extends to oral appliances and hypoglossal-nerve stimulation when patients meet specific clinical criteria. Similar policy shifts in France, Germany, and Japan shorten payback periods for device purchases and elevate replacement cycles. Payers have also instituted adherence audits, tying continued rental payments to the upload of usage data, an arrangement that incentivizes connected hardware and software ecosystems.

Product Recalls and Safety Concerns Undermining Patient Trust

The 2021-2024 Philips Respironics recall covering millions of CPAP, BiPAP, and ventilator units linked foam degradation to respiratory injuries and 560 deaths, according to FDA medical-device reports. The Philips Respironics recall, initiated in June 2021 and escalating through 2024, removed millions of continuous positive-airway-pressure and bi-level positive-airway-pressure devices from service due to polyester-based polyurethane foam degradation that released particulates and volatile organic compounds into the airway, triggering the largest Class I recall in respiratory-device history. The recall's ripple effects extended beyond Philips; ResMed issued a voluntary recall of specific mask models in January 2024 due to magnet-related risks for patients with implanted cardiac devices, and heightened FDA scrutiny has lengthened premarket-review timelines for novel respiratory products. Patient advocacy groups report lingering anxiety about foam integrity and off-gassing, which has elevated demand for transparent material-sourcing disclosures and third-party testing certifications. Manufacturers are responding by migrating to silicone-based sound-attenuation materials and publishing detailed bills of materials, but rebuilding trust remains a multi-year endeavor that constrains premium pricing and complicates new-product launches.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in Cloud-Connected PAP & HST Devices

- Accelerated Uptake of AI-Driven Adherence-Coaching Platforms

- Poor Patient Compliance & Device Abandonment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Diagnostic devices are expanding at an 11.45% CAGR through 2031, nearly double the pace of the broader market, as payers tighten documentation requirements and home sleep-test kits displace costly in-lab polysomnography for uncomplicated obstructive sleep apnea cases. The American Academy of Sleep Medicine updated accreditation standards in January 2025 to recognize Type-3 and Type-4 devices that measure airflow, respiratory effort, oxygen saturation, and, in some cases, actigraphy as acceptable for moderate-to-high pretest-probability patients, thereby compressing diagnostic costs from approximately USD 2,000 per in-lab study to under USD 300 per home test. Polysomnography systems retain a role for complex cases involving central sleep apnea, periodic limb movement disorder, or suspected narcolepsy, but volume is migrating to ambulatory settings. Pulse oximeters and actigraphy wearables serve as screening tools rather than definitive diagnostics. Yet, their ubiquity in consumer wellness devices, Apple Watch Series 10 and Samsung Galaxy Watch, both received FDA clearance in 2024 for sleep-apnea notification, raises the prospect that millions of individuals will bypass clinical pathways entirely.

Therapeutic devices commanded 67.75% of market share in 2025, anchored by the installed base of continuous positive-airway-pressure, bi-level positive-airway-pressure, and automatic positive-airway-pressure systems that benefit from Medicare's 5-year replacement-useful-life standard. Positive-airway-pressure devices, subdivided into continuous, bi-level, and automatic variants, constitute the most significant therapeutic segment. Yet, differentiation has shifted from hardware ergonomics to cloud-connected personalization algorithms, such as ResMed's Smart Comfort, which received FDA clearance in December 2025 and leverages more than 100 million patient nights of data to auto-titrate pressure settings.

Geography Analysis

North America commanded 41.56% of market share in 2025, anchored by entrenched Medicare and private-payer reimbursement pathways, a mature installed base exceeding 10 million active continuous positive-airway-pressure users, and the concentration of platform vendors ResMed, Philips, and Fisher & Paykel that dominate durable-medical-equipment supply chains. The FDA's consent decree against Philips in April 2024, which bars United States sales until the company demonstrates sustained compliance with quality-system regulations, accelerated market-share redistribution; Canada and Mexico exhibit slower growth due to smaller populations and less-developed home-care infrastructure, yet both markets are benefiting from cross-border durable-medical-equipment distribution and the expansion of private sleep clinics that bypass public-system wait times. The regulatory maturity of North America creates both stability and saturation; incremental growth hinges on replacement cycles, adherence improvements, and the penetration of high-margin alternatives such as hypoglossal-nerve stimulation, which expanded its addressable U.S. population to approximately 1.5 million after the FDA broadened indications to moderate obstructive sleep apnea in 2024.

Asia Pacific is forecast to clock an 8.9% CAGR from 2025-2030, the fastest regional trajectory in the global Sleep Apnea Devices market. Prevalence data highlight substantial latent demand: systematic reviews peg adult OSA rates as high as 23.6% in China and suggest India may harbor more than 50 million affected adults. Diagnosis remains limited by physician awareness and the scarcity of sleep labs, but government insurance expansions in China and India are underwriting the adoption of portable HST kits. Multinational brands partner with respiratory-therapy chains and telehealth portals to deploy loaner CPAP programs that convert to household purchases once adherence is proven.

- 3B Medical

- Apex Medical

- Asahi Kasei Corp. (ZOLL Medical)

- BMC Medical Co. Ltd.

- Braebon Medical Corp.

- Cadwell

- Compumedics Ltd.

- Drive DeVilbiss Healthcare

- Fisher & Paykel Healthcare

- Inspire Medical Systems

- Inspire Sleep (Hypoglossal Stim)

- Koninklijke Philips

- Lowenstein Medical GmbH

- Natus Medical

- Nihon Kohden

- Oventus Medical Ltd.

- React Health

- Resmed

- Samsung Electronics Co. Ltd. (Wearable Dx)

- SomnoMed Ltd.

- Teleflex

- Vivos Therapeutics Inc.

- Vyaire Medical

- Whole You Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global OSA Prevalence Tied to Obesity

- 4.2.2 Expanded Insurance Coverage for PAP & Oral Appliances

- 4.2.3 Technological Advances in Cloud-Connected PAP & HST Devices

- 4.2.4 Accelerated Uptake of AI-Driven Adherence-Coaching Platforms

- 4.2.5 Corporate Wellness Programmes Mandating Workforce Sleep Apnea Screening

- 4.2.6 Post-Recall Supplier Diversification Accelerating Emerging-Brand Adoption

- 4.3 Market Restraints

- 4.3.1 Product Recalls & Safety Concerns Eroding Patient Trust

- 4.3.2 Poor Patient Compliance and Device Abandonment

- 4.3.3 Tightened Cybersecurity Rules Raising Connected-Device Costs

- 4.3.4 OTC Wearable Screeners Cannibalising Clinical Device Sales

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Diagnostic Devices

- 5.1.1.1 Polysomnography Systems (In-Lab PSG)

- 5.1.1.2 Home Sleep Test Kits (Type-3/4)

- 5.1.1.3 Pulse Oximeters

- 5.1.1.4 Actigraphy Wearables

- 5.1.1.5 Others

- 5.1.2 Therapeutic Devices

- 5.1.2.1 Positive Airway Pressure (PAP) Devices

- 5.1.2.1.1 Continuous PAP (CPAP)

- 5.1.2.1.2 Bi-level PAP (BiPAP)

- 5.1.2.1.3 Automatic PAP (Auto-PAP)

- 5.1.2.2 Adaptive Servo-Ventilation (ASV)

- 5.1.2.3 Oral Appliances

- 5.1.2.4 Hypoglossal-Nerve Stimulation Implants

- 5.1.2.5 Oxygen Therapy Devices

- 5.1.2.5.1 Stationary Oxygen Concentrators

- 5.1.2.5.2 Portable Oxygen Concentrators

- 5.1.2.6 Airway-Clearance Systems

- 5.1.2.7 Nasal & Full-face Masks

- 5.1.2.8 Accessories & Consumables

- 5.1.2.1 Positive Airway Pressure (PAP) Devices

- 5.1.1 Diagnostic Devices

- 5.2 By End-User

- 5.2.1 Hospitals

- 5.2.2 Home-care Settings

- 5.2.3 Ambulatory Surgical & Specialty Clinics

- 5.2.4 Others

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 India

- 5.3.3.3 Japan

- 5.3.3.4 Australia

- 5.3.3.5 South Korea

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 3B Medical Inc.

- 6.4.2 Apex Medical Corp.

- 6.4.3 Asahi Kasei Corp. (ZOLL Medical)

- 6.4.4 BMC Medical Co. Ltd.

- 6.4.5 Braebon Medical Corp.

- 6.4.6 Cadwell Laboratories Inc.

- 6.4.7 Compumedics Ltd.

- 6.4.8 Drive DeVilbiss Healthcare LLC

- 6.4.9 Fisher & Paykel Healthcare Ltd.

- 6.4.10 Inspire Medical Systems Inc.

- 6.4.11 Inspire Sleep (Hypoglossal Stim)

- 6.4.12 Koninklijke Philips N.V.

- 6.4.13 Lowenstein Medical GmbH

- 6.4.14 Natus Medical Inc.

- 6.4.15 Nihon Kohden Corporation

- 6.4.16 Oventus Medical Ltd.

- 6.4.17 React Health

- 6.4.18 ResMed Inc.

- 6.4.19 Samsung Electronics Co. Ltd. (Wearable Dx)

- 6.4.20 SomnoMed Ltd.

- 6.4.21 Teleflex Inc.

- 6.4.22 Vivos Therapeutics Inc.

- 6.4.23 Vyaire Medical Inc.

- 6.4.24 Whole You Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment