PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061504

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061504

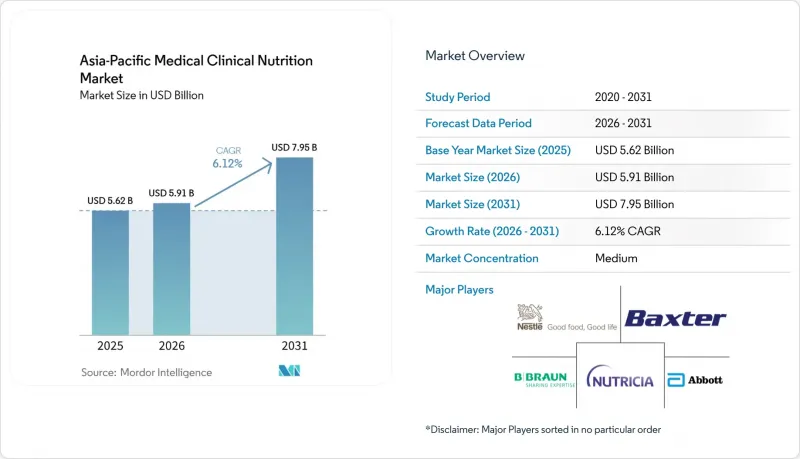

Asia-Pacific Medical Clinical Nutrition - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the asia-Pacific medical clinical nutrition market size was valued at USD 5.62 billion in 2025 and is estimated to grow from USD 5.91 billion in 2026 to reach USD 7.95 billion by 2031, at a CAGR of 6.12% during the forecast period (2026-2031).

This report Segments the Industry Into Route of Administration (Oral and Enteral, Parenteral), Application (Malnutrition, Metabolic Disorders, and More), Age Group (Pediatric, Adult, and Geriatric), Distribution Channel (Hospitals Pharmacies, Retail Pharmacies, and More), and Country (China, Japan, India, and More). Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Medical Clinical Nutrition Market Trends and Insights

Rising Prevalence of Metabolic and Chronic Diseases

Hospital caseloads of diabetes, renal failure, and metabolic syndrome are swelling, with regional diabetes prevalence projected to rise from 295.8 million in 2021 to 411.7 million by 2045. Many patients now present at younger ages, lengthening lifetime dependence on medical nutrition. Singapore's 2024 chronic disease initiative, which combines continuous glucose monitoring with dietitian-led counseling, is already showing improvements in adherence metrics. South Korea has documented a parallel uptick in metabolic syndrome admissions requiring intravenous amino acid solutions. Formulas fortified with branched-chain amino acids, omega-3 fatty acids, and fiber blends are therefore displacing standard polymeric products in critical-care wards. Hospitals that integrate proactive metabolic-nutrition pathways report shorter stays and lower readmission bills, reinforcing payer support for specialized products.

Expanding Geriatric Population

The share of residents aged 60 plus is on track to double to 22.9% by 2050 in Southeast Asia. Sarcopenia, dysphagia, and polypharmacy are boosting the need for hyper-protein, texture-modified formulas. Japan's 2024 long-term care reforms fund home enteral regimens that can be stored at room temperature, thereby increasing demand in rural prefectures. Eleven nations endorsed the Colombo Declaration on Healthy Ageing, pledging routine nutrition screening in primary care. Updated Chinese guidelines now recommend 1.2-1.5 g of protein per kilogram for frail seniors, up from 1.0 g, which raises per-capita formula volumes.

Inconsistent Reimbursement Across APAC

Only 40% of regional governments fund home enteral nutrition. Cash-pay reliance forces caregivers to prepare blenderized feeds that risk microbial contamination. Thailand lifted reimbursement caps in 2024, yet still covers just 60% of standard-formula costs, excluding premium disease-specific variants. India's flagship health insurance plan omits the enteral and parenteral categories, limiting its penetration to urban households with annual incomes above USD 5,000. Manufacturers, therefore, run dual portfolios, releasing value-engineered lines priced below USD 2 per serving for cash markets while reserving premium immunonutrition for reimbursed systems in Japan and Australia.

Other drivers and restraints analyzed in the detailed report include:

- Growing Healthcare Spending and Middle-Income Expansion

- Home-Based Nutrition Uptake Via Smart Pumps and Telehealth

- Low Inventory Appetite in Hospital Pharmacies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oral and Enteral held 89.52% of Asia-Pacific medical clinical nutrition market share in 2025, reflecting affordability and compatibility with functional gastrointestinal tracts. Nevertheless, parenteral formulations are posting a 7.36% CAGR due to rising ICU admissions and the broader use of automated compounding, which reduces contamination to 0.1%. China's 2024 device-approval reforms enabled domestic three-chamber bags to reach hospitals a year faster than before, reducing reliance on imports. Hospitals across Japan and South Korea are transitioning from manual mixing to premixed multi-chamber bags, which are delivered within 48 hours, thereby decreasing pharmacy labor and waste. Enteral innovation continues, with thickened "jelly" formats mitigating aspiration risk in dysphagic elders while oral immunonutrition shortens surgical stays by 2.5 days.

Malnutrition held 14.72 % revenue share in 2025, yet oncology formulas are expanding at 7.69% CAGR as 40%-80% of cancer inpatients present undernourished. China's nationwide audit revealed only 38% of malnourished oncology patients received dedicated intervention, underscoring a sizeable treatment gap. Japan cleared three new perioperative immunonutrition products in 2025, accelerating specialty launches across the region. Formulas targeting inflammatory bowel disease, chronic kidney disease, and liver disorders continue to generate stable demand, while exclusive enteral nutrition achieved a 60% remission rate in pediatric Crohn's cohorts in 2025.

List of Companies Covered in this Report:

- Abbott Laboratories

- Ajinomoto

- B. Braun

- Baxter

- Beckton Dickinson

- Boston Scientific

- Cardinal Health

- Danone

- DSM-Firmenich

- Fresenius

- Hero Nutritionals

- JW Pharmaceutical

- Kate Farms

- Kelun Pharma

- Meiji Holdings

- Nestle Health Science

- Otsuka

- Perrigo

- Reckitt/Mead Johnson

- Vifor Pharma

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Metabolic & Chronic Diseases

- 4.2.2 Expanding Geriatric Population

- 4.2.3 Growing Healthcare Spending & Middle Class

- 4.2.4 Home-Based Nutrition Uptake Via Smart Pumps & Telehealth

- 4.2.5 nHEOR Evidence Shaping Reimbursement

- 4.2.6 Regionalization of Premixed PN Manufacturing

- 4.3 Market Restraints

- 4.3.1 Inconsistent Reimbursement Across APAC

- 4.3.2 Low Inventory Appetite in Hospital Pharmacies

- 4.3.3 Counterfeit Products in Emerging ASEAN Markets

- 4.3.4 Shortage of Precision-Nutrition Dietitians

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Route of Administration

- 5.1.1 Oral & Enteral

- 5.1.2 Parenteral

- 5.2 By Application

- 5.2.1 Malnutrition

- 5.2.2 Metabolic Disorders

- 5.2.3 Gastrointestinal Diseases

- 5.2.4 Neurological Diseases

- 5.2.5 Cancer

- 5.2.6 Other Diseases

- 5.3 By Age Group

- 5.3.1 Pediatric

- 5.3.2 Adult

- 5.3.3 Geriatric

- 5.4 By Distribution Channel

- 5.4.1 Hospitals Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Channel

- 5.4.4 Others

- 5.5 By Country

- 5.5.1 China

- 5.5.2 Japan

- 5.5.3 India

- 5.5.4 Australia

- 5.5.5 South Korea

- 5.5.6 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott

- 6.3.2 Ajinomoto

- 6.3.3 B. Braun SE

- 6.3.4 Baxter

- 6.3.5 Becton Dickinson

- 6.3.6 Boston Scientific

- 6.3.7 Cardinal Health

- 6.3.8 Danone Nutricia

- 6.3.9 DSM-Firmenich

- 6.3.10 Fresenius Kabi

- 6.3.11 Hero Nutritionals

- 6.3.12 JW Pharmaceutical

- 6.3.13 Kate Farms

- 6.3.14 Kelun Pharma

- 6.3.15 Meiji Holdings

- 6.3.16 Nestle Health Science

- 6.3.17 Otsuka Pharmaceutical

- 6.3.18 Perrigo

- 6.3.19 Reckitt/Mead Johnson

- 6.3.20 Vifor Pharma

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment