PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061528

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061528

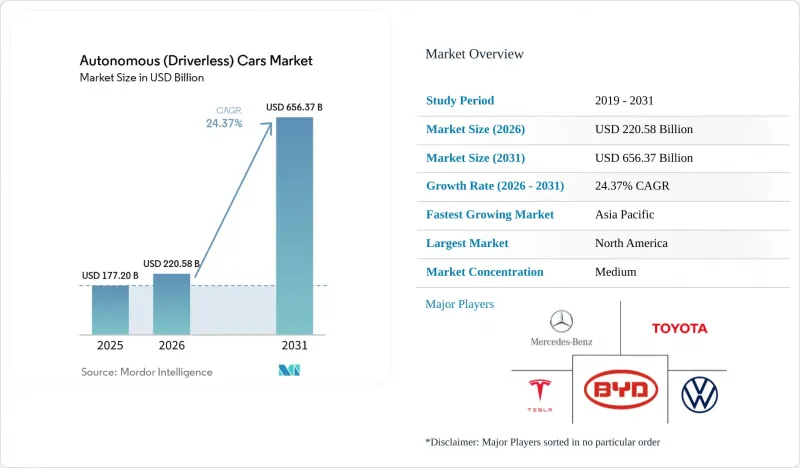

Autonomous (Driverless) Cars - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the autonomous (driverless) cars market size is expected to grow from USD 177.20 billion in 2025 to USD 220.58 billion in 2026, and is forecast to reach USD 656.37 billion by 2031, at a CAGR of 24.37% during the forecast period (2026-2031).

This report is Segmented by Level of Automation (Level 1, Level 2, Level 3, and More), Vehicle Type (Hatchbacks, Sedans, and SUVs and MPVs), Propulsion Type (ICE, BEV, and HEV), Mobility Form (Personal Ownership and Shared Mobility), Component (Hardware, Software, and Services), and Geography. Market Forecasts are Provided in Value (USD) and Volume (Units).

Global Autonomous (Driverless) Cars Market Trends and Insights

Rapid Expansion of Robo-Taxi Pilots across Asian Mega-Cities

In late 2024, Baidu's Apollo Go achieved a significant milestone of cumulative rides across multiple cities in China. Meanwhile, Waymo was recording a substantial number of paid rides weekly in both Phoenix and San Francisco. In April 2025, Tokyo revised its Road Traffic Act, paving the way for Level 4 operations in specific districts. This move prompted automotive giants Toyota and Nissan to hasten their pilot schedules. Waymo's unit economics are on the upswing, with the company's average ride cost dropping to a competitive level. Concurrently, Baidu celebrated achieving positive contribution margins in Wuhan by the end of 2024. Furthermore, municipalities in the region are more amenable to issuing commercial licenses than their Western counterparts, resulting in a notable near-term growth boost.

Government Mandates for ADAS-Centric Safety Regulations in the EU and China

The European Union enforced Regulation 2019/2144 in July 2024, obligating all new passenger vehicles to include autonomous emergency braking, intelligent speed assistance, lane-keeping assist, and driver monitoring systems . China released GB/T 40429-2021 and granted multiple Level 3 permits in Beijing and Shenzhen during 2024, setting hands-free highway operation as an attainable near-term goal . Japan, South Korea, and ASEAN states have adopted UN Regulation 157, creating a contiguous regulatory pull across Asia. The shared compliance calendar increases volume for advanced sensors, reduces per-unit cost, and shortens payback periods for automakers that invest in Level 3 systems.

Patchwork State-Level AV Regulations in the United States Delay Commercial Scale

There is no single federal framework governing autonomous vehicles in the United States; therefore, companies must navigate unique rules in each state. California revoked Cruise permits after a pedestrian-dragging event, and Arizona limited commercial services in certain municipalities. This fragmentation leads to duplicative compliance programs and slows interstate freight automation, resulting in a few percentage points of reduced near-term growth.

Other drivers and restraints analyzed in the detailed report include:

- Falling LiDAR and AI Compute Costs Unlocking Mass-Market Level 3 Launches

- 5G-V2X Corridor Roll-Outs in North American Freight Networks

- Public Mistrust Intensified by High-Profile Robotaxi Incidents

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Level 1 driver assistance captured 43.47% of the autonomous (driverless) cars market share in 2025. The segment benefits from mandatory features, such as autonomous emergency braking and lane-keeping assist, which are now standard in entry trims across Europe and China. Level 3 conditional automation is being scaled in premium models following regulatory approvals in Nevada, California, Germany, and Japan. Mercedes-Benz logged 2 million miles on Drive Pilot during 2024, and BMW plans to deploy Highway Assistant in 2026. The segment transition indicates hardware commoditization and the monetization of subscription software.

Level 5 full automation is projected to grow at a 24.39% CAGR through 2031, as robo-taxi fleets in Wuhan, Phoenix, and Tokyo enlarge service areas. The autonomous (driverless) cars market observes operators amortizing sensor suites across high daily utilization, turning fixed assets into revenue generators for up to 18 hours per day. Level 4 deployments in middle-mile freight and shuttle services demonstrate commercial viability in geo-fenced zones. Subscription models in Level 3 vehicles signal recurring revenue potential, while Level 5 fleets redefine the economics of urban mobility.

SUVs and MPVs held 78.81% of the autonomous (driverless) cars market share in 2025 because their larger rooflines and front fascias can comfortably house LiDAR, radar, and camera arrays without aesthetic trade-offs. Waymo's Jaguar I-PACE and Baidu's Apollo Moon rely on sport-utility form factors for roomy sensor placement. The autonomous (driverless) cars market will retain SUV dominance, where passenger capacity and sensor heat dissipation are key considerations.

Hatchbacks are forecast to expand at a 25.11% CAGR to 2031 as solid-state LiDAR shrinks below 10 centimeters and compute units fit under compact dashboards. Automakers can bring autonomy to high-volume B-segment platforms, and dense Asian cities favor compact dimensions for easier curb access. Sedans remain relevant where long-range aerodynamics and battery efficiency are essential, as seen in the Tesla Model S and Lucid Air deployments.

Geography Analysis

North America generated 38.71% of the autonomous (driverless) cars market share in 2025. Waymo operated more than a lakh weekly rides across four United States cities, and Tesla enrolled multiple vehicles in its supervised Full Self-Driving program. Regulatory fragmentation remains a hurdle after California revoked Cruise's permits; however, federal spending on V2X roadside units supports autonomous freight deployment on interstate corridors. Canada allows Level 4 testing without safety drivers in Ontario and Quebec, but its smaller addressable fleet tempers near-term volume.

Asia Pacific is projected to register a 25.05% CAGR through 2031. Baidu Apollo Go crossed the 6 million ride milestone, and Pony.ai plus AutoX expanded fleets in Beijing, Guangzhou, and Shenzhen. Japan's Road Traffic Act revision allows Level 4 vehicles to operate within geofenced districts, enabling Toyota's pilots in Tokyo's Odaiba and Nissan's trials in Yokohama. India remains nascent until HD mapping density improves and a clear regulatory framework emerges, while South Korea grants Level 4 permits for autonomous buses on dedicated lanes in Sejong City.

Europe benefits from the General Safety Regulation that mandates Level 2 features as standard. Mercedes-Benz launched Drive Pilot in Germany in 2024, followed by Nevada and California. BMW targets a Level 3 rollout by 2026. Fleet decarbonization rules are accelerating the adoption of autonomous electric trucks. Einride has deployed 200 driverless trucks across Germany, the Netherlands, and Sweden, while Volvo introduced the Vera system for port shuttles. South America and the Middle East pilot niche services, yet sparse HD maps and evolving rules delay broader scale.

- Waymo LLC

- Tesla, Inc.

- General Motors Co. (Cruise LLC)

- Baidu Inc. (Apollo)

- Toyota Motor Corporation

- Volkswagen AG

- Mercedes-Benz Group AG

- BMW AG

- Nissan Motor Co. Ltd.

- AB Volvo

- Hyundai Motor Group

- BYD Auto Co., Ltd.

- Pony.ai Inc.

- AutoX Inc.

- Uber Technologies Inc.

- Aptiv PLC

- Mobileye Global Inc.

- NVIDIA Corporation

- Magna International Inc.

- Continental AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Robo-Taxi Pilots across Asian Mega-Cities

- 4.2.2 Government Mandates for ADAS-Centric Safety Regulations in the EU and China

- 4.2.3 Falling LiDAR and AI Compute Costs Unlocking Mass-Market L3 Launches

- 4.2.4 5G-V2X Corridor Roll-outs in North American Freight Networks

- 4.2.5 Power-Efficient Automotive SoCs Enabling In-Vehicle Edge AI

- 4.2.6 Fleet Decarbonization Targets Accelerating Autonomous Middle-Mile Logistics in Europe

- 4.3 Market Restraints

- 4.3.1 Patchwork State-Level AV Regulations in the United States Delay Commercial Scale

- 4.3.2 Public Mistrust Intensified by High-Profile Robotaxi Incidents in China

- 4.3.3 Automotive-Grade AI Chip Shortages and Fab Capacity Constraints

- 4.3.4 High-Definition Map Maintenance Costs in Emerging Markets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Level of Automation

- 5.1.1 Level 1- Driver Assistance

- 5.1.2 Level 2 - Partial Automation

- 5.1.3 Level 3 - Conditional Automation

- 5.1.4 Level 4 - High Automation

- 5.1.5 Level 5 - Full Automation

- 5.2 By Vehicle Type

- 5.2.1 Hatchbacks

- 5.2.2 Sedans

- 5.2.3 Sport Utility Vehicles (SUVs) and Multi-Purpose Vehicles (MPVs)

- 5.3 By Propulsion Type

- 5.3.1 Internal Combustion Engine (ICE)

- 5.3.2 Battery Electric Vehicles (BEV)

- 5.3.3 Hybrid Electric Vehicles (HEV)

- 5.4 By Mobility Form

- 5.4.1 Personal Ownership

- 5.4.2 Shared Mobility (Robo-Taxi, Shuttle)

- 5.5 By Component

- 5.5.1 Hardware

- 5.5.1.1 Sensors (LiDAR, RADAR, Cameras, Ultrasonic, IMU)

- 5.5.1.2 Computing Platforms (SoCs, GPUs)

- 5.5.1.3 Actuators and Control Systems

- 5.5.2 Software

- 5.5.2.1 Perception and Planning Suites

- 5.5.2.2 Mapping and Localization Engines

- 5.5.2.3 Driver Monitoring and HMI

- 5.5.3 Services

- 5.5.3.1 Integration and Validation

- 5.5.3.2 Remote Operation and Tele-operation

- 5.5.1 Hardware

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Waymo LLC

- 6.4.2 Tesla, Inc.

- 6.4.3 General Motors Co. (Cruise LLC)

- 6.4.4 Baidu Inc. (Apollo)

- 6.4.5 Toyota Motor Corporation

- 6.4.6 Volkswagen AG

- 6.4.7 Mercedes-Benz Group AG

- 6.4.8 BMW AG

- 6.4.9 Nissan Motor Co. Ltd.

- 6.4.10 AB Volvo

- 6.4.11 Hyundai Motor Group

- 6.4.12 BYD Auto Co., Ltd.

- 6.4.13 Pony.ai Inc.

- 6.4.14 AutoX Inc.

- 6.4.15 Uber Technologies Inc.

- 6.4.16 Aptiv PLC

- 6.4.17 Mobileye Global Inc.

- 6.4.18 NVIDIA Corporation

- 6.4.19 Magna International Inc.

- 6.4.20 Continental AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment