PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061564

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061564

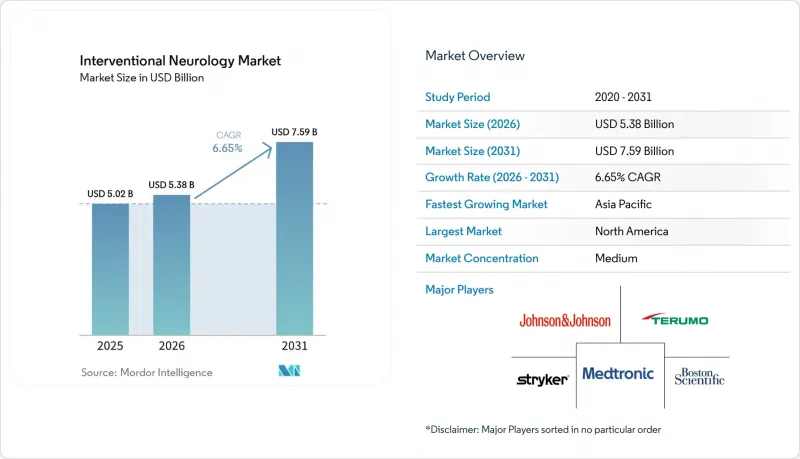

Interventional Neurology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the interventional neurology market size is expected to increase from USD 5.02 billion in 2025 to USD 5.38 billion in 2026 and reach USD 7.59 billion by 2031, growing at a CAGR of 6.65% over 2026-2031.

This report is Segmented by Product Type (Treatment Devices, Diagnostic & Imaging Technologies), Therapeutic Application (Ischemic Stroke, Hemorrhagic Stroke, and More), Procedure Type (Thrombectomy, and More), End-User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Interventional Neurology Market Trends and Insights

Stroke Incidence Outpaces Interventional Capacity

As stroke incidence rises, the gap between this surge and the capacity for intervention widens, driving a consistent demand for both diagnostic software and thrombectomy kits. In 2021, global data reported 7.63 million new ischemic strokes and projected a potential 50% increase by 2050 if current risk trends persist. Projections indicate that by 2030, China will have over 300 million citizens aged 65 and older, and India's stroke mortality has more than doubled from 1990 to 2019. In response, governments are certifying stroke centers and subsidizing endovascular training. Notably, Japan expanded its thrombectomy-capable facilities from 800 in 2020 to a projected 1,100 by 2024. With the demand for specialists lagging behind the growing caseload, hospitals are increasingly turning to AI-triage modules.

Mechanical Thrombectomy Gains Traction

Once 24-hour outcome data validated its efficacy, mechanical thrombectomy transitioned from a niche procedure to a standard care practice. A 2024 trial highlighted a significant difference: 49.2% of patients achieved functional independence at 90 days when thrombectomy was performed within a full-day window, compared to just 33.3% with optimal medical care. Reflecting this trend, Germany's data indicated a jump in thrombectomy usage from 8.2% of ischemic stroke admissions in 2015 to 22.7% by 2021, with analysts projecting penetration to exceed 30% by 2026. However, access remains inconsistent; many small U.S. community hospitals and facilities in emerging markets lack essential resources like biplane angiography and 24/7 specialists, leading to a two-tiered system. In response, manufacturers introduced compact aspiration catheters and single-plane C-arm suites, reducing upfront costs by 25%.

High Device Costs & Reimbursement Challenges

Hospitals face significant financial barriers due to the high costs of biplane angiography suites, which range between USD 2-3 million. Additionally, disposables for a single thrombectomy procedure can exceed USD 12,000. Revisions to Medicare's fee structures have further strained hospital margins in the United States. In India, the National Health Mission reimburses only USD 1,200 per procedure, prompting many public hospitals to discontinue the service. In Latin America, thrombectomy is generally excluded from standard benefit packages, with coverage largely restricted to private insurers in countries like Brazil and Argentina. While manufacturers have introduced catheter lines priced 30% lower than flagship systems, the cost disparity remains a significant challenge for low-income regions. Without the development of sustainable payment models, penetration into secondary cities will remain limited, constraining overall procedural growth.

Other drivers and restraints analyzed in the detailed report include:

- Hospital Mergers Drive Up Capital Expenditure

- AI Imaging Enhances Triage Efficiency

- Shortage of Qualified Neuro-Interventionalists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, treatment devices led in revenue generation, but diagnostic technologies are rapidly gaining ground as hospitals adopt comprehensive stroke pathways. Mechanical thrombectomy kits, anchored by Penumbra's Lightning Flash and Vesalio's NeVa systems, promise higher first-pass rates, solidifying their position in the interventional neurology market. Flow diverters, like Stryker's Surpass Evolve, expedite aneurysm healing, and liquid embolics, such as Onyx, achieve a notable 78% complete obliteration in arteriovenous malformation cases. Hospitals are increasingly allocating budgets for AI-integrated technologies, including CT and biplane labs. Diagnostic vendors are enhancing their value through bundled software licenses, leading to a projected 7.56% CAGR growth for imaging systems by 2031, while maintaining gross margins around 45%.

In 2025, ischemic stroke accounted for 42.12% of spending, underscoring its dominance in clot retrieval. While ischemic care remains a significant share of the interventional neurology market, hemorrhagic indications are gaining traction. Advancements like improved coil technology and low-profile microcatheters are enhancing success rates and reducing retreatments. The 2024 CURES trial highlighted minimally invasive repairs' benefits, leading payers to endorse them. New evidence linking early intervention to reduced cognitive decline is prompting guideline updates, potentially increasing case captures.

With hemorrhagic procedures projected to grow at 7.60% through 2031, their contribution to the interventional neurology market is set to rise, especially in Japan and South Korea, where over 70% of adults over 50 are screened for aneurysms. Vendors focusing on detachable coils and flow disruptors stand to benefit from this trend, providing a cushion against potential price erosions in thrombectomy.

Geography Analysis

In 2025, North America accounted for 41.25% of the revenue, driven by significant thrombectomy adoption and a well-established network of comprehensive stroke centers. Between 2016 and 2021, U.S. case volumes grew by 60%. However, Medicare payment reductions created margin pressures, leading multistate systems to consolidate purchasing power and prioritize vendors offering lifecycle services and AI-driven solutions. In 2024, Canada launched 12 new stroke centers in Ontario and British Columbia. Meanwhile, Mexico introduced pilot thrombectomy programs, although reimbursement remains limited.

Asia-Pacific is expected to be the fastest-growing region, with a projected growth rate of 8.50% through 2031. China plans to establish 5,000 certified stroke centers by 2030 and has mandated AI triage implementation in tier-2 hospitals by 2025. In India, private healthcare providers are investing in endovascular suites in metropolitan areas. Japan, despite challenges related to a shortage of skilled operators, has increased the number of thrombectomy-ready hospitals to 1,100 as of 2024.

Europe continues to benefit from coordinated national strategies. Germany, with its 340 stroke units and rapidly increasing thrombectomy rate, highlights the success of structured rollouts. By 2024, France is expected to expand population access to 75%, while the United Kingdom operates 24 thrombectomy hubs. However, rural areas in Scotland and Wales still lack 24/7 coverage.

Latin America and the Middle East show uneven progress. In Brazil, the national healthcare system covers thrombolysis but not thrombectomy, limiting the number of procedures performed. Argentina's private insurers are piloting coverage, signaling potential future growth. In the Gulf states, expertise is being imported through tele-intervention to address workforce shortages. Africa remains in the early stages of development, constrained by limited reimbursement frameworks and a shortage of specialists.

- Abbott Laboratories

- Acandis

- Balt USA

- Cerus Endovascular

- InspireMD

- Johnson & Johnson (Cerenovus)

- Kaneka Medix

- Medtronic

- MicroPort

- MicroVention Inc.

- Penumbra

- Phenomenex Neuro

- Phenox

- Rapid Medical

- Silk Road Medical

- Stryker

- Terumo

- VESALIO

- Wallaby Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing Population & Stroke Incidence Surge

- 4.2.2 Rapid Adoption of Mechanical Thrombectomy

- 4.2.3 Hospital Consolidation Driving Capital Equipment Upgrades

- 4.2.4 AI-Guided Imaging Enabling Faster Triage & Intervention

- 4.2.5 Technological Advancements

- 4.2.6 Neuro-ICU Tele-Intervention Programs

- 4.3 Market Restraints

- 4.3.1 High Device Cost & Reimbursement Hurdles

- 4.3.2 Shortage of Trained Neuro-Interventionalists

- 4.3.3 Saturation of Primary Stroke Centers in Tier-1 Cities

- 4.3.4 Supply-Chain Exposure to Rare-Earth Metal Volatility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Treatment Devices

- 5.1.1.1 Mechanical Thrombectomy Devices

- 5.1.1.2 Neurovascular Stent Systems

- 5.1.1.3 Embolic Coils & Intrasaccular Implants

- 5.1.1.4 Flow-Diverter Devices

- 5.1.1.5 Liquid Embolic Agents

- 5.1.1.6 Balloon Guide & Aspiration Catheters

- 5.1.1.7 Neurovascular Micro-catheters & Guidewires

- 5.1.2 Diagnostic & Imaging Technologies

- 5.1.2.1 Biplane Cerebral Angiography Systems

- 5.1.2.2 3-D Rotational Angiography

- 5.1.2.3 Intra-operative CT / Cone-Beam CT

- 5.1.2.4 MRI / fMRI for Neuro-intervention Planning

- 5.1.2.5 Trans-cranial & Carotid Doppler Ultrasound

- 5.1.2.6 Neuro-navigation & Robotics Platforms

- 5.1.2.7 AI-based Stroke Imaging & Triage Software

- 5.1.1 Treatment Devices

- 5.2 By Therapeutic Application

- 5.2.1 Ischemic Stroke

- 5.2.2 Hemorrhagic Stroke

- 5.2.3 Sub-arachnoid Hemorrhage

- 5.2.4 Cerebral Aneurysm

- 5.2.5 Arteriovenous Malformation

- 5.3 By Procedure Type

- 5.3.1 Thrombectomy

- 5.3.2 Coiling / Embolization

- 5.3.3 Stenting & Flow Diversion

- 5.3.4 Clipping

- 5.3.5 Angioplasty

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Specialty Stroke Centers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Abbott

- 6.3.2 Acandis GmbH

- 6.3.3 Balt USA

- 6.3.4 Cerus Endovascular

- 6.3.5 InspireMD

- 6.3.6 Johnson & Johnson (Cerenovus)

- 6.3.7 Kaneka Medix

- 6.3.8 Medtronic plc

- 6.3.9 MicroPort Scientific

- 6.3.10 MicroVention Inc.

- 6.3.11 Penumbra Inc.

- 6.3.12 Phenomenex Neuro

- 6.3.13 Phenox GmbH

- 6.3.14 Rapid Medical

- 6.3.15 Silk Road Medical

- 6.3.16 Stryker Corporation

- 6.3.17 Terumo Corporation

- 6.3.18 Vesalio

- 6.3.19 Wallaby Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment