PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061608

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061608

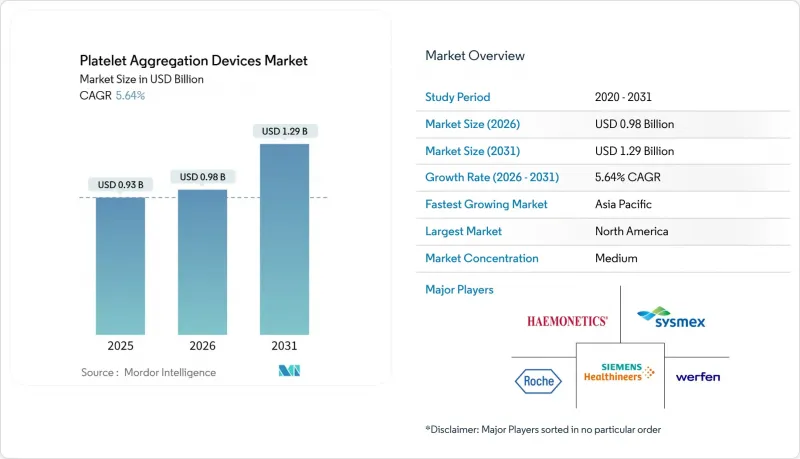

Platelet Aggregation Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the platelet aggregation devices market size is projected to expand from USD 0.93 billion in 2025 and USD 0.98 billion in 2026 to USD 1.29 billion by 2031, registering a CAGR of 5.64% between 2026 to 2031.

This report is Segmented by Product (Systems, Reagents, and More), Technology (Light-Transmission Aggregometry, Impedance Aggregometry, and More), Sample Type (Platelet-Rich Plasma and More), Application (Clinical Diagnostics, Antiplatelet-Therapy Monitoring, and More), End User (Hospitals, Diagnostic Laboratories, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Platelet Aggregation Devices Market Trends and Insights

Rising Incidence of Cardiovascular & Bleeding Disorders

Cardiovascular disease prevalence continues to climb, prompting hospitals to increase routine platelet testing volumes. The American Heart Association projects hypertension rates rising to 61% and diabetes to 26.8% by 2050, trends that drive long-term utilization of platelet analyzers. Clinical teams also observe high rates of platelet dysfunction in hematologic therapies such as CAR-T, adding to the complex testing needs of oncology departments. These converging disease burdens intensify demand across the platelet aggregation devices market. National cardiology registries in the United States and the European Union reported an 8% rise in patients receiving dual antiplatelet therapy between 2024 and 2025. Parallel data from the World Federation of Hemophilia counted 418,000 individuals with diagnosed platelet-function disorders in 2024, a 12% increase from 2022. Interventional cardiologists rely on aggregometers to identify clopidogrel non-responders before percutaneous coronary interventions, while hematologists use the same platforms to phenotype inherited deficiencies, such as Glanzmann thrombasthenia.

Growing Geriatric Population Base

United Nations projections place the global population aged >= 65 years at 1.6 billion by 2050, up from 1.0 billion in 2024. Aging is associated with endothelial dysfunction and heightened platelet reactivity, complicating anticoagulant management during orthopedic or neurologic procedures. European and North American geriatric wards have begun installing benchtop aggregometers to individualize antiplatelet dosing for hip-fracture repair and stroke rehabilitation. Japanese hospitals, serving the world's oldest society, run platelet function panels during routine outpatient visits to pre-empt thrombotic events, reinforcing demand for platelet aggregation devices. Vendors that offer low-volume, fully automated platforms capture this demographic-driven spend because more minor sample requirements align with frail-elderly phlebotomy constraints.

High Capital & Consumable Cost of Advanced Systems

Fully automated platelet-aggregation workstations list between USD 120,000 and USD 180,000, with annual service contracts adding another USD 15,000-25,000. Consumables cost USD 12-18 per patient, compared with under USD 2 for routine coagulation tests reimbursed under bundled codes. Community hospitals operating on single-digit margins hesitate to invest unless vendors offer reagent-rental contracts that shift capital expense into per-test fees. Even in tertiary centers, cap-ex committees require multidisciplinary utilization cards from cardiology, hematology, and perioperative services to approve a purchase. This cost headwind trims the platelet aggregation devices market CAGR by nearly a percentage point in price-sensitive Asia and Latin America.

Other drivers and restraints analyzed in the detailed report include:

- Technological Shift to Automated/Integrated Analyzers

- Hospital Adoption of Point-of-Care Platelet Function Testing

- Shortage of Skilled Hemostasis Technologists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Systems generated 49.90% of 2025 revenue, reflecting the legacy installed base of optical and impedance analyzers in hospital core laboratories. Consumables and accessories, however, are set to outpace the overall platelet aggregation devices market with an 8.90% CAGR through 2031, bolstered by single-use microfluidic discs that slash cleaning downtime and cross-contamination risk. Reagent contracts now bundle agonists with software-unlock codes, converting what was once a one-time hardware sale into an annuity stream. As laboratories migrate toward whole-blood impedance methods, demand shifts to new reagent formulations, fragmenting supplier shares and opening space for niche providers of specialty agonists. Accessories such as calibrators and pipette tips hold slim margins but remain indispensable because hospitals must follow manufacturer-validated workflows to safeguard accreditation.

Margins on consumables encourage vendors to preinstall drive locks in their analyzers, forcing hospitals to source supplies exclusively from the original manufacturer to maintain warranty compliance. That lock-in strategy deepens switching costs and reinforces revenue visibility throughout the forecast period. Regional distributors also bundle preventive-maintenance kits with reagent reorder thresholds, increasing annual spend per instrument. Consequently, the platelet aggregation devices market size attributed to consumables will continue to grow steadily, even in mature regions where capital refresh cycles have plateaued.

Clinical testing accounted for 63.50% of 2025 revenue, as cardiologists and hematologists rely on aggregometry for routine monitoring, preoperative risk assessments, and differential diagnosis of bleeding disorders. The regulatory push for personalized antiplatelet therapy fuels daily test volumes, keeping instrument utilization high in catheterization labs and stroke units. Drug development and toxicology, while smaller, is forecast to expand at an 8.78% CAGR because oncology and cardiovascular trials now require thrombocytopenia surveillance as part of FDA safety checklists. Sponsors demand platforms that output raw kinetic curves for pharmaco-informatics, a capability offered by only a handful of premium devices, thereby commanding higher price points.

Academic consortia investigating platelet involvement in metastasis and neurodegeneration receive European Research Council and NIH grants earmarked for advanced aggregometry.

Geography Analysis

North America accounted for 39.40% of 2025 revenue, driven by hospitals budgeting aggressively for AI-enhanced analyzers and insurers reimbursing high-acuity cardiac procedures. Canada's Ontario and British Columbia health systems piloted reference-lab hubs that process rural samples overnight, leveraging HL7 interfaces to return results before morning rounds.

Europe enforces stringent evidence requirements under IVDR, pushing manufacturers to concentrate market launches in Germany, France, and the United Kingdom, where notified-body capacity is highest. Germany's Federal Joint Committee updated hospital quality indicators in 2025 to include platelet-function testing rates for PCI patients, promoting adoption through pay-for-performance incentives. The United Kingdom's NHS Supply Chain renegotiated framework agreements in 2026, combining consumables and maintenance into outcome-based contracts that reward reductions in downtime.

Asia-Pacific is forecast to grow at an 8.02% CAGR, led by China's national coagulation-disorder registry, which enrolled 1.2 million patients by end-2025 and mandates platelet-function testing for unexplained bleeding cases. Japan and South Korea, both super-aged societies, prioritize microfluidic disc systems that minimize draw volumes, while Australian trauma centers integrate viscoelastic-plus-platelet cartridges into massive transfusion protocols.

- AggreDyne Inc.

- Alpha Laboratories Ltd.

- Bash Medical Ltd.

- Bio/Data

- Chrono-Log

- Drucker Diagnostics LLC

- Entegrion Inc.

- Roche

- Grifols

- Haemonetics

- Helena Biosciences Europe

- Helena Laboratories

- Helmer Scientific

- Instrumentation Laboratory (Stago)

- Siemens Healthineers

- Sienco Inc.

- Sysmex

- Tem Innovations GmbH

- Werfen

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Incidence of Cardiovascular and Bleeding Disorders

- 4.2.2 Growing Geriatric Population Base

- 4.2.3 Technological Shift to Automated/Integrated Analyzers

- 4.2.4 Hospital Adoption of Point-of-Care Platelet Function Testing

- 4.2.5 AI-Driven Decision Support in Antiplatelet Therapy

- 4.2.6 Micro-Fluidic Disc-Based LTA Reducing Sample Volume

- 4.3 Market Restraints

- 4.3.1 High Capital and Consumable Cost of Advanced Systems

- 4.3.2 Shortage of Skilled Hemostasis Technologists

- 4.3.3 Regulatory Delays for Optical-AI Hybrid Devices

- 4.3.4 Inter-Laboratory Result Variability Undermining Reimbursement

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Systems

- 5.1.2 Reagents

- 5.1.3 Consumables and Accessories

- 5.2 By Application

- 5.2.1 Clinical Applications

- 5.2.2 Antiplatelet-therapy Monitoring

- 5.2.3 Disease & Translational Research

- 5.2.4 Drug Development & Toxicology

- 5.2.5 Others

- 5.3 By Technology

- 5.3.1 Light Transmission Aggregometry

- 5.3.2 Impedance/Multiple-Electrode Aggregometry

- 5.3.3 Viscoelastic Platelet Mapping Assays

- 5.3.4 Micro-fluidic Disc-based Aggregometry

- 5.3.5 Flow-Cytometry-based Aggregometry

- 5.4 By Sample Type

- 5.4.1 Whole Blood

- 5.4.2 Platelet-Rich Plasma (PRP)

- 5.4.3 Washed Platelets

- 5.5 By End-User

- 5.5.1 Hospitals

- 5.5.2 Diagnostic Laboratories

- 5.5.3 Blood Banks

- 5.5.4 Research & Academic Institutes

- 5.5.5 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 South Korea

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 AggreDyne Inc.

- 6.3.2 Alpha Laboratories Ltd.

- 6.3.3 Bash Medical Ltd.

- 6.3.4 Bio/Data Corporation

- 6.3.5 Chrono-Log Corporation

- 6.3.6 Drucker Diagnostics LLC

- 6.3.7 Entegrion Inc.

- 6.3.8 F. Hoffmann-La Roche Ltd

- 6.3.9 Grifols S.A.

- 6.3.10 Haemonetics Corporation

- 6.3.11 Helena Biosciences Europe

- 6.3.12 Helena Laboratories Corporation

- 6.3.13 Helmer Scientific Inc.

- 6.3.14 Instrumentation Laboratory (Stago)

- 6.3.15 Siemens Healthineers AG

- 6.3.16 Sienco Inc.

- 6.3.17 Sysmex Corporation

- 6.3.18 Tem Innovations GmbH

- 6.3.19 Werfen

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment