PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061609

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061609

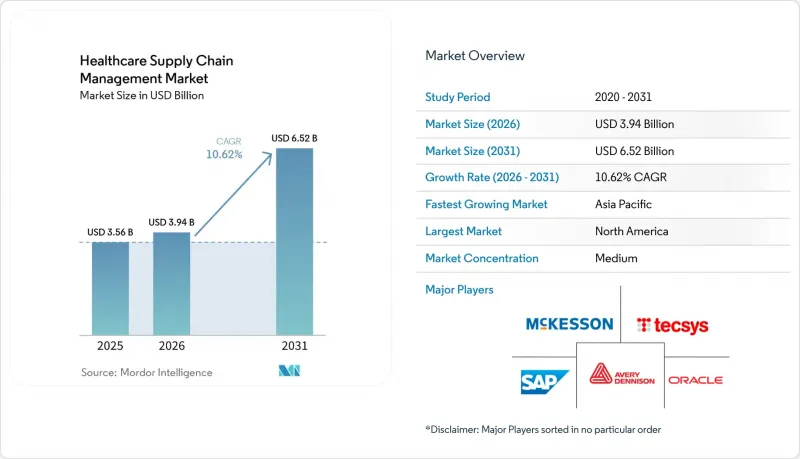

Healthcare Supply Chain Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the healthcare supply chain management market size was valued at USD 3.56 billion in 2025 and estimated to grow from USD 3.94 billion in 2026 to reach USD 6.52 billion by 2031, at a CAGR of 10.62% during the forecast period (2026-2031).

This report is Segmented by Component (Software, Hardware and More), by Deployment Mode (On-Premise and Cloud-Based), End-User (Healthcare Providers, Healthcare Payers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Global Healthcare Supply Chain Management Market Trends and Insights

Cloud-First Upgrades to Cut Inventory Waste

Nearly 70% of U.S. hospitals plan to run core supply operations on cloud platforms by 2026, unlocking real-time visibility that trims excess stock and reduces stockouts. Machine-learning engines embedded in these platforms analyze consumption patterns, seasonality, procedure schedules, and supplier lead times to keep inventory within clinically safe but financially lean thresholds. Health systems that completed migration report inventory-related savings of up to 30% alongside improved clinician satisfaction due to fewer product shortages. Cloud architecture also streamlines integration with electronic health records and simplifies multi-site coordination, critical as provider networks consolidate.

Mandatory UDI & Track-and-Trace Regulations

The FDA's Unique Device Identification system and DSCSA serialization requirements force every device and drug unit to carry a machine-readable code that travels across the entire chain, from factory to bedside. Compliance platforms automatically capture, store, and exchange this data, cutting recall investigation times from weeks to hours and strengthening patient safety. Providers that align early gain operational benefits through automated expiration alerts and end-to-end provenance auditing.

High Up-Front Integration & Training Costs

Implementing a full-stack platform demands USD 2-15 million for a mid-sized system, covering software, hardware, interfaces, and six-to-twelve-month staff education. Complex links to electronic health records and financial modules often double initial budgets, stretching payback horizons to 18-24 months and deterring smaller providers.

Other drivers and restraints analyzed in the detailed report include:

- AI-Driven Demand Sensing & Predictive Restocking

- Rapid Outsourcing to GPOs for Cost Containment

- Cyber-Security & Data-Privacy Liabilities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software platforms accounted for 60.70% of the healthcare supply chain management market in 2025, reflecting urgent demand for unified command centers that coordinate sourcing, contracting, logistics, and compliance. Services, though smaller, post the fastest 11.45% CAGR thanks to provider reliance on implementation, workflow redesign, and change-management support . Hardware-RFID readers, automated dispensing cabinets, and IoT sensors-remains indispensable for real-time data capture, even as budgets tilt toward cloud licenses.

Software's edge stems from embedded analytics that spot variance, predict demand, and surface compliance gaps. Oracle Health's next-generation EHR integrates supply chain modules, enabling clinicians to place auto-replenish orders without leaving patient charts. Such convergence aligns procurement decisions with clinical pathways, shrinking waste and improving case costing

Geography Analysis

North America retained 45.10% of healthcare supply chain management market share in 2025. DSCSA deadlines and a mature GPO ecosystem underpin stable demand, while ongoing consolidation among IDNs fuels enterprise-scale platform rollouts. Canada's provincially funded health systems invest in supply-chain command centers to curb rising procedure costs.

Asia-Pacific records the steepest 12.42% CAGR to 2031. Rapid hospital construction in China and India, vaccine self-sufficiency programs, and governmental push for digital health infrastructure drive adoption. Thailand's vendor-managed inventory pilots and Singapore's IoT-enabled hospital campuses showcase regional innovation. The healthcare supply chain management market size for Asia-Pacific is projected to double by 2030 as cold-chain for advanced therapeutics scales.

Europe shows steady growth underpinned by Medical Device Regulation (MDR), climate-aligned ESG mandates, and Brexit-triggered buffer-stock strategies. Multinational health systems seek platforms that consolidate multilingual labeling, track environmental metrics, and interface with country-specific e-procurement portals.

- GHX

- Tecsys Inc.

- Infor

- Oracle

- SAP

- Mckesson

- Syft

- Cardinal Health

- Owens & Minor

- LogiTag Systems

- Jump Technologies

- Epicor

- JDA (Blue Yonder)

- Manhattan Associates

- IBM

- Medline Industries

- FlexLogistics

- ClarusONE

- Zebra Technologies

- OptiFreight(UPS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-first upgrades to cut inventory waste

- 4.2.2 Mandatory UDI & track-and-trace regulations

- 4.2.3 AI-driven demand sensing & predictive restocking

- 4.2.4 Rapid outsourcing to GPOs for cost containment

- 4.2.5 Vendor-managed inventory for critical drugs

- 4.2.6 Climate-resilient cold-chain design mandates

- 4.3 Market Restraints

- 4.3.1 High up-front integration & training costs

- 4.3.2 Cyber-security & data-privacy liabilities

- 4.3.3 Shortage of supply-chain IT talent in hospitals

- 4.3.4 Opaque supplier ESG data blocking compliance

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Hardware

- 5.1.3 Services

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud-based

- 5.3 By End User

- 5.3.1 Healthcare Providers

- 5.3.2 Healthcare Payers

- 5.3.3 Pharma & Biotech Companies

- 5.3.4 Contract Manufacturing Organizations

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 GHX

- 6.3.2 Tecsys Inc.

- 6.3.3 Infor

- 6.3.4 Oracle (Cerner)

- 6.3.5 SAP SE

- 6.3.6 McKesson Corporation

- 6.3.7 Syft

- 6.3.8 Cardinal Health

- 6.3.9 Owens & Minor

- 6.3.10 LogiTag Systems

- 6.3.11 Jump Technologies

- 6.3.12 Epicor

- 6.3.13 JDA (Blue Yonder)

- 6.3.14 Manhattan Associates

- 6.3.15 IBM

- 6.3.16 Medline Industries

- 6.3.17 FlexLogistics

- 6.3.18 ClarusONE

- 6.3.19 Zebra Technologies

- 6.3.20 OptiFreight(UPS)

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment