PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061622

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061622

Light-Sport Aircraft - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

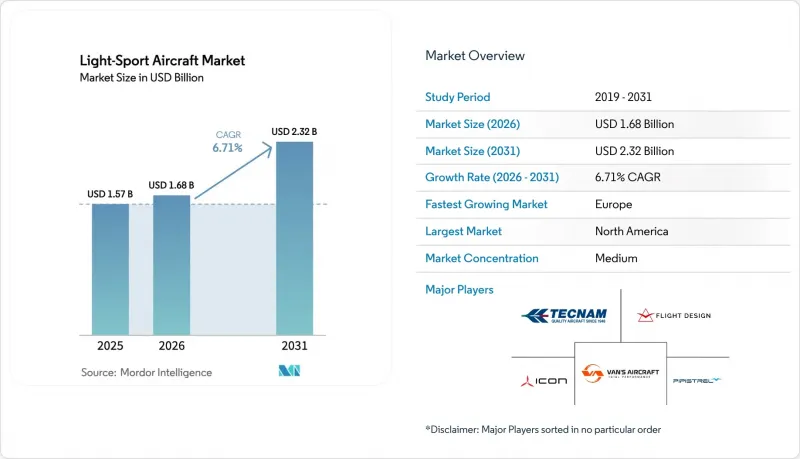

According to Mordor Intelligence, the light-sport aircraft market size is expected to grow from USD 1.57 billion in 2025 to USD 1.68 billion in 2026 and is forecasted to reach USD 2.32 billion by 2031 at a 6.71% CAGR over 2026-2031.

This report is Segmented by Type (Airplane and Seaplane), Propulsion Type (Conventional ICE, Hybrid-Electric, and Electric), Application (Flight Training and Pilot Schools, Personal/Recreational Ownership, Aerial Work and Utility Operations, and Rental/Flying Clubs), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Light-Sport Aircraft Market Trends and Insights

MOSAIC Final Rule Expands LSA Capabilities And Sport Pilot Privileges

The FAA's July 2025 MOSAIC final rule replaces prescriptive weight limits with a 59-knot calibrated airspeed VS1 threshold for sport pilots and a 61-knot VS0 for aircraft certificated after July 2026, enabling broader aircraft eligibility and operational flexibility. The rule authorizes four-seat configurations, retractable landing gear, controllable-pitch propellers, and night operations subject to appropriate endorsements and medical status under the new framework. The shift immediately widens the pool of sport-pilot-eligible aircraft, with association analysis indicating that a large portion of legacy single-engine piston models now fall within sport-pilot privileges under performance criteria rather than legacy weight caps. Manufacturer statements and product updates show rapid alignment, including amphibious and advanced avionics variants that benefit from the performance-based approach. The staged effective dates, with pilot training and repairman updates in late 2025 and airworthiness certification changes in 2026, create a manageable transition period for schools and OEMs to adjust fleets and production scheduling.

Flight Training Demand And Fleet Renewal Favor Cost-Effective LSA Trainers

High-utilization training schools continue to expand fleets with modern, low-operating-cost platforms, sustaining near-term order books and line utilization for LSA-aligned OEMs. Fleet procurement in 2025 and early 2026 concentrated on glass-cockpit trainers and multi-engine types to support progression from entry certificates to commercial ratings, signaling the value of standardized avionics and maintenance across large operations. OEM announcements point to increased training capacity at schools in North America and Europe, with deliveries of single- and twin-trainers that fit within or parallel to the expanding LSA envelope. Aligning MOSAIC privileges with training profiles, including night operations with endorsements, enhances aircraft utility and scheduling flexibility at busy schools. Electrified trainers add a complementary pathway to sustainability goals at select locations where short sorties and charging infrastructure align with curriculum needs.

Insurance Availability And Premium Pressure For GA/LSA Operators

Aviation insurers have flagged modest firming for 2026, with the best pricing available to operators that maintain clean loss records, structured recurrent training, and documented safety features across fleets. Premium differentiation often reflects pilot total time, time in type, recency of training, and aircraft equipment levels more than the specific medical certification path, which lowers uncertainty for operators adapting to MOSAIC and BasicMed intersections. Rate dispersion remains notable for new operations without claims history or for higher hull values, which can translate to elevated base rates until operators establish stable safety performance over time. Documented mitigations like hangared storage, defined currency standards, and modern avionics often qualify for credits that partially offset broader market pressure. The overall implication for the light-sport aircraft market is that professionally managed fleets can contain insurance inflation. At the same time, casual or newly established operations face a higher bar to achieve best-available pricing.

Other drivers and restraints analyzed in the detailed report include:

- BasicMed Expansion And Sport-Pilot Pathways Broaden The Eligible Pilot Pool

- Composite Airframes And Modern Avionics Reduce Operating Cost And Improve Safety

- Supply-Chain Bottlenecks For Engines, Avionics, And Composites

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Airplanes accounted for 94.32% market share in 2025, the highest share across types in the light-sport aircraft market, while seaplanes are projected to grow at a 7.78% CAGR to 2031 from a smaller installed base. The profile reflects extensive land-based training fleets and high dispatch reliability on paved and grass strips, with embedded infrastructure at schools and clubs across North America and Europe. OEM shipment data show meaningful volumes for conventional configurations, supported by broad familiarity among instructors and maintenance teams. Amphibious platforms add distinct use cases in waterfront regions and recreational corridors, and they benefit from MOSAIC's performance framing, which favors stall-speed parameters for operational approval rather than legacy weight caps. A flagship amphibious model raised its gross weight in 2024 and emphasizes spin-resistant characteristics, placing it as a premium niche choice for operators who value water access and safety systems.

Growth prospects for seaplanes reflect underpenetrated coastal, lake-country, and island routes where waterborne access can substitute for longer overland segments or limited surface infrastructure. With MOSAIC's flexibility around performance-based standards, future four-seat configurations and expanded equipment options improve mission versatility where takeoff and landing areas are constrained by geography. For landplanes, the light-sport aircraft market size narrative centers on training-cycle stability, high airframe utilization, and standardized avionics that streamline instruction and maintenance planning at scale. The interplay between these subsegments supports a portfolio approach for schools and owner-operators who split time between paved strips and water sites depending on season, mission, and region. Shipment concentration in 2025 among a handful of brands underscores the importance of after-sales support and the availability of ready parts in sustaining uptime for both land and water operations.

Geography Analysis

North America held a 40.03% share of the light-sport aircraft market in 2025 and is expected to benefit from MOSAIC's staged implementation across training and airworthiness. The regulatory modernization expands eligible aircraft and missions, supporting fleet augmentation at schools and rental networks. Schools with national networks have begun taking deliveries aligned to their plans, reinforcing a steady pipeline of glass-cockpit trainers. As BasicMed and MOSAIC converge, pilots may progress more fluidly from sport to private privileges, improving utility and time-on-type continuity for operators. Across the US and Canada, regulatory validation and OEM support underpin the fleet renewal cycle in the light-sport aircraft market.

Europe is projected to grow at a 7.88% CAGR through 2031, supported by a robust OEM ecosystem and momentum in propulsion certification. European training organizations continue to add single and twin models with modern avionics to scale capacity, guided by standardized procedures for airline-oriented training tracks. With a certified 125 kW electric motor approved by EASA and production capacity enabled by semi-automated lines in France and the UK, European OEMs and integrators have a clear path to expand electrified options for training and short-hop missions. Cross-border certification structures help OEMs deploy platforms more broadly, while market readiness varies by airport infrastructure, charging capacity, and training doctrine. Facility expansions and forward order coverage at leading manufacturers indicate a sustained book of business that extends into the forecast window.

Asia-Pacific, South America, and the Middle East and Africa collectively account for the balance, with certifications and partnerships opening new channels for electrified trainers and modern LSAs. The first national safety certificate for a fully electric light trainer in South Korea highlights entry points for low-noise aircraft in urban or noise-sensitive airspaces. Manufacturers and training providers in South Asia have advanced direct-factory representation and launched new academies to accelerate fleet support and spare-parts responsiveness. Regional growth trajectories are likely to track national regulatory alignment, airport readiness, and training demand, with incremental adoption of electric trainers where infrastructure and curricula support charging throughout the day. Over the forecast period, the light-sport aircraft market benefits from cascading adoption as certification reciprocity and OEM support networks deepen in newer geographies.

- Costruzioni Aeronautiche TECNAM S.p.A.

- PIPISTREL D.O.O.

- Flight Design general aviation GmbH

- Van's Aircraft, Inc.

- ICON Aircraft, Inc.

- CubCrafters, Inc.

- American Legend Aircraft Co.

- TL-ULTRALIGHT s.r.o.

- Aeropro SK s.r.o.

- Jabiru Aircraft Pty Ltd

- Zenith Aircraft Company

- Brumby Aircraft Australia Pty. Ltd.

- Stemme Production GmbH

- Super Petrel USA

- Czech Aircraft Group s.r.o.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 MOSAIC final rule expands LSA capabilities and sport pilot privileges

- 4.2.2 Flight training demand and fleet renewal favor cost-effective LSA trainers

- 4.2.3 Composite airframes and modern avionics reduce operating cost and improve safety

- 4.2.4 BasicMed expansion and sport-pilot pathways broaden the eligible pilot pool

- 4.2.5 Unleaded avgas transition pathways (fleet authorizations) de-risk engine operations

- 4.2.6 Limited aerial-work authorizations under MOSAIC create new revenue streams

- 4.3 Market Restraints

- 4.3.1 Supply-chain bottlenecks for engines, avionics, and composites

- 4.3.2 Insurance availability and premium pressure for GA/LSA operators

- 4.3.3 Electric LSA endurance/charging limits constrain training throughput

- 4.3.4 Airspace and VFR/day restrictions cap utility in dense corridors

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Airplane

- 5.1.2 Seaplane

- 5.2 By Propulsion Type

- 5.2.1 Conventional ICE

- 5.2.2 Hybrid-Electric

- 5.2.3 Electric

- 5.3 By Application

- 5.3.1 Flight Training and Pilot Schools

- 5.3.2 Personal/Recreational Ownership

- 5.3.3 Aerial Work and Utility Operations

- 5.3.4 Rental/Flying Clubs

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 France

- 5.4.2.3 Germany

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Costruzioni Aeronautiche TECNAM S.p.A.

- 6.4.2 PIPISTREL D.O.O.

- 6.4.3 Flight Design general aviation GmbH

- 6.4.4 Van's Aircraft, Inc.

- 6.4.5 ICON Aircraft, Inc.

- 6.4.6 CubCrafters, Inc.

- 6.4.7 American Legend Aircraft Co.

- 6.4.8 TL-ULTRALIGHT s.r.o.

- 6.4.9 Aeropro SK s.r.o.

- 6.4.10 Jabiru Aircraft Pty Ltd

- 6.4.11 Zenith Aircraft Company

- 6.4.12 Brumby Aircraft Australia Pty. Ltd.

- 6.4.13 Stemme Production GmbH

- 6.4.14 Super Petrel USA

- 6.4.15 Czech Aircraft Group s.r.o.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment