PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061650

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061650

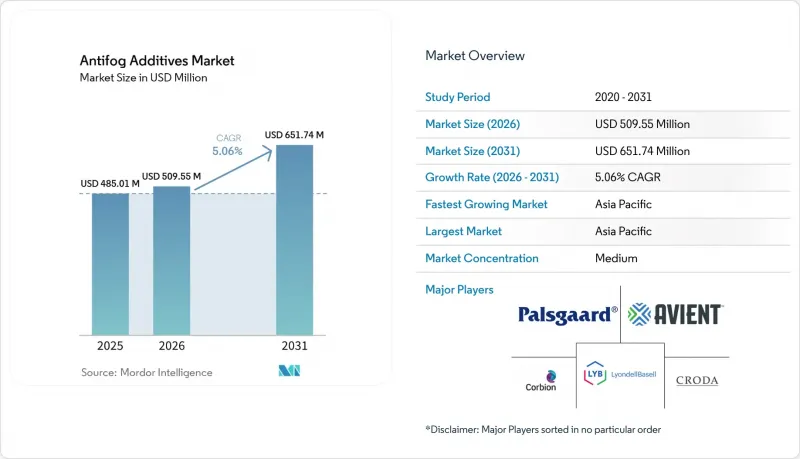

Antifog Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, antifog additives market size in 2026 is estimated at USD 509.55 million, growing from 2025 value of USD 485.01 million with 2031 projections showing USD 651.74 million, growing at 5.06% CAGR over 2026-2031.

This report is Segmented by Type (Glycerol Esters, Polyglycerol Esters, Sorbitan Esters of Fatty Acids, Other Types), Application (Agricultural Films, Packaging Films, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Antifog Additives Market Trends and Insights

Shift to high-clarity greenhouse films in vertical farming

Vertical farming relies on optical precision, making condensation control a direct productivity lever. Chinese trials show that selecting advanced antifog films lifts solar radiation penetration by 5.33%, enhancing yields and farmer margins. Berry Global's Tufflite Infrared film illustrates how anti-drip chemistry lengthens growing seasons and justifies premium pricing[1]. As luminescent quantum-dot films gain traction, any fog interference diminishes wavelength tuning, creating a self-reinforcing cycle of clarity requirements, higher prices, and performance-driven demand in the antifog additives market for next-generation additives.

Surge in mono-material flexible food packaging demand

The EU Packaging & Packaging Waste Regulation propels a pivot toward recyclable mono-material structures, removing traditional barrier layers that previously contained additive migration. Huhtamaki guidance under the India Plastics Pact places mono-material solutions at 73% of national plastic use, widening the addressable base for compliant antifog solutions in the antifog additives market. DNP Group's polyethylene-only pouches maintain oxygen and water-vapor resistance, yet require antifog chemistries that neither hinder sorting nor raise migration risk. Younger consumers' scrutiny of environmental claims forces brands to pick suppliers with demonstrable sustainability credentials.

Tightening REACH limits on ester migration in food-contact films

Regulation (EU) 2025/351 introduces new purity standards and NIAS risk-assessment thresholds. Any migration above 0.00015 mg/kg food now demands extensive toxicological data, pushing up testing costs and elongating development timelines. EFSA modeling shows polyglycerol packages could migrate up to 50 mg/kg food under worst-case conditions, limiting design windows. Suppliers unwilling to fund reformulation face potential market exit by the September 2026 compliance deadline, reshaping competition in the antifog additives market.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory cold-chain labeling regulations in North America

- Biobased ester innovation pipelines at key suppliers

- Short service-life complaints in hot-humid equatorial zones

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Glycerol esters held 37.58% of antifog additives market share in 2025 owing to decades-long acceptance by regulators and processors. The FDA 21 CFR 172.854 and WHO ADI of 0-25 mg/kg body weight underpin confidence in food packaging use. However, polyglycerol esters are outpacing at 5.65% CAGR thanks to superior thermal stability and lower volatility, properties validated in lab extrusion studies.

Sorbitan esters service niche polymer systems where specific migration properties are needed. An emerging cluster of biobased specialty blends targets controlled-release delivery that sustains antifog performance under temperature swings. Avient's Cesa platform integrates these chemistries, demonstrating how smart carrier matrices can extend film clarity in multi-cycle use.

Geography Analysis

Asia-Pacific leads the antifog additives market with 36.31% share in 2025, underpinned by state-driven agricultural modernization. Chinese subsidy programs increase cropland scale, encouraging investments in high-clarity greenhouse films that feature controlled antifog agents. India's protected cultivation is jumping to 250 million tons output by 2025, sustaining long-term additive demand. Japan's Positive List system, active since June 2025, requires local and imported films to pass stringent migration tests before market entry, thereby lifting technical barriers and unit pricing.

North America relies on cold-chain compliance to maintain food safety. FSMA 204 requires legible labeling during the entire distribution channel, making antifog visibility a compliance cost rather than an optional upgrade. The Global Cold Chain Alliance lists clear pack windows as a KPI for logistics quality audits.

Europe is in regulatory flux. REACH alignment under Regulation (EU) 2025/351 calls for extensive NIAS assessments and purity upgrades. While that creates near-term cost burdens, it also rewards early movers capable of documenting migration behavior at sub-ppm levels-often the global multinationals already invested in analytic capacity. South America and Middle East & Africa provide greenfield growth opportunities. Government greenhouse programs in Peru and Morocco pilot anti-drip films, but fragmented regulations and price sensitivity keep adoption gradual.

- Avient Corporation

- Corbion

- Croda International PLC

- Dupont

- Emery Oleochemicals

- Evonik Industries AG

- Guangzhou Cardlo biotechnology Co.,LTD

- High Grade Industries

- Kraton Corporation

- LyondellBasell Industries Holdings B.V.

- Palsgaard

- PCC Group

- Polyfill Technologies LLP

- Rapidmasterbatches

- Silibase Silicone

- Surya Masterbatches

- Taprath Elastomers LLP

- Tosaf

- ULTRA-PLAS CORPORATION

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid shift to high-clarity greenhouse films in vertical farming

- 4.2.2 Surge in mono-material flexible food packaging demand

- 4.2.3 Mandatory cold-chain labeling regulations in North America

- 4.2.4 Biobased ester innovation pipelines at key suppliers

- 4.2.5 Asia-Pacific agricultural subsidy programs for anti-fog films

- 4.3 Market Restraints

- 4.3.1 Tightening REACH limits on ester migration in food contact films

- 4.3.2 Short service-life complaints in hot-humid equatorial zones

- 4.3.3 Volatile mono- and poly-glycerol feedstock pricing

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Glycerol Esters

- 5.1.2 Polyglycerol Esters

- 5.1.3 Sorbitan Esters of Fatty Acids

- 5.1.4 Other Types

- 5.2 By Application

- 5.2.1 Agricultural Films

- 5.2.2 Packaging Films

- 5.2.3 Other Applications

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Avient Corporation

- 6.4.2 Corbion

- 6.4.3 Croda International PLC

- 6.4.4 Dupont

- 6.4.5 Emery Oleochemicals

- 6.4.6 Evonik Industries AG

- 6.4.7 Guangzhou Cardlo biotechnology Co.,LTD

- 6.4.8 High Grade Industries

- 6.4.9 Kraton Corporation

- 6.4.10 LyondellBasell Industries Holdings B.V.

- 6.4.11 Palsgaard

- 6.4.12 PCC Group

- 6.4.13 Polyfill Technologies LLP

- 6.4.14 Rapidmasterbatches

- 6.4.15 Silibase Silicone

- 6.4.16 Surya Masterbatches

- 6.4.17 Taprath Elastomers LLP

- 6.4.18 Tosaf

- 6.4.19 ULTRA-PLAS CORPORATION

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment