PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061652

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061652

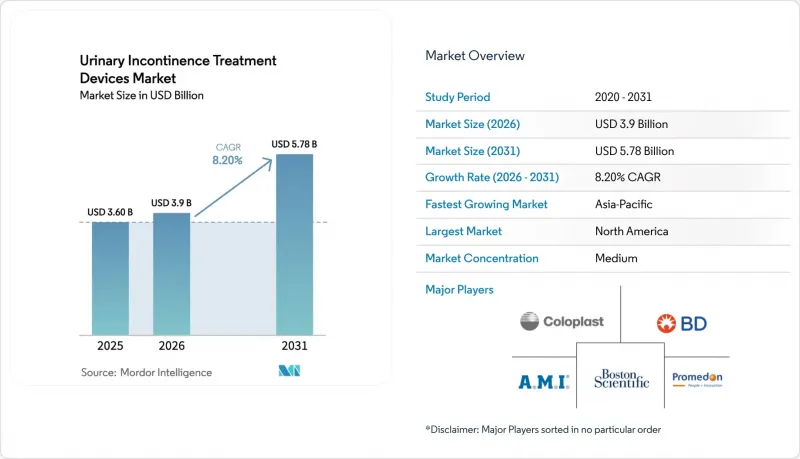

Urinary Incontinence Treatment Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the urinary incontinence treatment devices market size is projected to expand from USD 3.60 billion in 2025 and USD 3.9 billion in 2026 to USD 5.78 billion by 2031, registering a CAGR of 8.20% between 2026 to 2031.

This report is Segmented by Product (Urethral & Vaginal Slings, Artificial Urinary Sphincters, and More), Incontinence Type (Stress, Urge, Mixed, and More), Device Category (Internal Devices and External Devices), End User (Hospitals, Ambulatory Surgical Centers, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Urinary Incontinence Treatment Devices Market Trends and Insights

Ageing Population & Prevalence Surge

One in three women older than 55 now experiences some form of incontinence, and prevalence in residential facilities exceeds 75%. Health systems also report that 11.2% of Medicare beneficiaries carry an incontinence diagnosis, with prevalence jumping to 20.6% in skilled-nursing settings. Because falls, dermatitis and urinary tract infections often follow untreated leakage, clinicians frame devices as preventive investments rather than discretionary aids. This shift shields demand from macro-economic slowdowns, giving the urinary incontinence treatment devices market a recession-resistant profile. For manufacturers, the demographic wave provides a long runway for connected devices that monitor hydration, activity and therapy adherence in real time.

Demand for Minimally-invasive & Outpatient Procedures

Health providers target shorter stays and lower facility fees by moving sacral nerve stimulation and tibial nerve stimulation to office environments. The eCoin device, implanted under local anesthesia, delivers 68% symptom improvement at 48 weeks and eliminates overnight hospitalization. Outpatient neuromodulation cuts direct procedure costs by as much as 40% while preserving outcomes, making payer authorizations faster and broadening patient eligibility. Device vendors therefore engineer quick-fit leads, awake-procedure workflows and training modules for non-surgical specialists. As a result, the urinary incontinence treatment devices market gains access to ambulatory surgery centers and urology offices previously untapped by implantable therapy.

Limited Awareness & Persisting Social Stigma

Seven of every ten people living with symptoms never discuss them with a clinician, delaying diagnosis and skewing prevalence data. Regional surveys show that 32% of older adults in Shanghai regard leakage as shameful compared with 6% of healthcare professionals, revealing stark communication gaps. Stigma also keeps many women from regular exercise, indirectly raising cardiovascular risk. When clinicians omit routine screening, device adoption lags despite technological progress. Addressing cultural barriers therefore remains central to long-run expansion of the urinary incontinence treatment devices market.

Other drivers and restraints analyzed in the detailed report include:

- Favourable Reimbursement in US & EU

- AI-enabled Pelvic-floor Digital Therapeutics Adoption

- Post-operative Complications & Device Recalls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Slings contributed 34.68% to the urinary incontinence treatment devices market share in 2025, a share built on surgical familiarity and mature supply chains. Continuous refinements in mesh material and anchoring techniques sustain relevance, yet future volume growth shifts toward electrical and neuromodulation systems posting a 12.08% CAGR. Battery lives exceeding 10 years, wireless re-charging and MRI conditionality reduce lifetime maintenance, making implants practical for younger patients who expect device longevity. Venture investments in closed-loop stimulation add algorithms that auto-adjust amplitude to bladder pressure, raising therapeutic success while limiting manual re-programming. Slings therefore evolve into one component of a broader toolkit rather than the market's single anchor.

Procedural economics also nudge hospitals toward neuromodulation, because outpatient implantation frees theatre time and yields faster DRG turn-around. Nonetheless, sling revisions still account for a sizeable portion of uro-gynecology caseload, generating predictable consumable demand for specialized surgical instruments. The result is a dual-trajectory product landscape in which low-complexity devices defend existing share while electronics-heavy platforms capture incremental volume. Within this context, the urinary incontinence treatment devices market enjoys diversified revenue streams resilient to reimbursement or technology shocks.

Stress incontinence captured 45.03% of revenue in 2025, underpinned by well-established mid-urethral sling protocols and favorable long-term efficacy data. Yet urge incontinence therapies are projected to log an 11.18% CAGR as sacral and tibial neuromodulation demonstrate 85% first-year success rates against 49% for oral antimuscarinics. Device makers respond by fine-tuning stimulation algorithms that modulate afferent signaling, thereby addressing overactive detrusor activity without systemic side effects. Cross-over designs now allow the same implant to treat mixed incontinence via firmware updates, letting physicians personalize care without added inventory.

For stress cases, innovation targets less-invasive sling insertion and alternative bulking agents to defer surgery. Meanwhile, overflow and functional categories remain niche yet clinically significant, driving demand for sensors that alert caregivers when voiding assistance is needed. Smart diapers equipped with moisture detectors already reduce dermatitis by supporting timely changes in cognitively impaired patients. Diversifying indications therefore enlarges the urinary incontinence treatment devices market while underscoring the need for modular platforms adaptable across symptom clusters.

Geography Analysis

North America held 39.42% of the urinary incontinence treatment devices market share in 2025, buoyed by Medicare Part B covering 80% of approved device costs after deductible thresholds. Leading academic centers in Chicago and Boston adopt smart bladder implants that transmit fullness data to mobile apps, accelerating clinical translation and peer-review dissemination. FDA de novo pathways further facilitate first-in-class approvals, allowing start-ups to navigate stringent quality benchmarks without legacy PMA burdens. Commercial insurers often mirror Medicare policy within one year, shortening payer-adoption lag and maintaining high per-patient revenue within the region.

Asia-Pacific is the fastest-growing geography with a 10.48% CAGR through 2031, driven by rapid population aging in Japan and infrastructure investments in China and India. Japan's policy push for home-based care fuels demand for remote-monitored devices, while private hospitals in tier-one Chinese cities open cash-pay opportunities for neuromodulation implants. Nevertheless, specialist shortages outside urban hubs limit procedural throughput, prompting vendors to build training hubs and tele-mentoring platforms. Cultural taboos around discussing bladder symptoms continue to suppress early diagnosis, yet mobile-first health campaigns supported by governments begin to close awareness gaps.

Germany reimburses prescribed aids with capped co-payments, but southern markets remain price-sensitive, slowing premium implant uptake. Still, policy makers cite the continent's EUR 69 billion (USD 79.84 billion) continence burden to advocate preventive coverage for digital therapeutics and early-stage neuromodulation. Middle East, Africa and South America collectively represent under-penetrated territories where cost-effective external devices and mobile support tools may leapfrog resource constraints, gradually enlarging the global urinary incontinence treatment devices market.

- Coloplast

- Boston Scientific

- Beckton Dickinson

- Medtronic

- Johnson & Johnson

- Hollister

- B. Braun

- ConvaTec Group plc

- PROMEDON

- A.M.I.

- Caldera Medical

- Zephyr Surgical Implants

- Teleflex

- Cardinal Health

- UroMems SA

- Neuspera Medical Inc.

- Uroplasty Inc.

- Kimberly-Clark Worldwide

- Essity

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing Population & Prevalence Surge

- 4.2.2 Demand For Minimally-Invasive & Outpatient Procedures

- 4.2.3 Favourable Reimbursement In US & EU

- 4.2.4 AI-Enabled Pelvic-Floor Digital Therapeutics Adoption

- 4.2.5 Rapid Innovation In Neuromodulation & Wireless Implants

- 4.3 Market Restraints

- 4.3.1 Limited Awareness & Persisting Social Stigma

- 4.3.2 Post-Operative Complications & Device Recalls

- 4.3.3 Shortage Of Specialised Uro-Gyne Surgeons In Low- and Middle-Income Countries

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Urethral & Vaginal Slings

- 5.1.2 Artificial Urinary Sphincters

- 5.1.3 Electrical / Neuromodulation Devices

- 5.1.4 Urinary Catheters

- 5.1.5 Penile Clamps & Pessary Devices

- 5.1.6 Urinary Drainage Bags & Accessories

- 5.1.7 Pelvic Floor Training Systems

- 5.2 By Incontinence Type

- 5.2.1 Stress

- 5.2.2 Urge

- 5.2.3 Mixed

- 5.2.4 Overflow & Functional

- 5.3 By Device Category

- 5.3.1 Internal Devices

- 5.3.2 External Devices

- 5.4 By End User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centres

- 5.4.3 Specialty / Uro-Gyn Clinics

- 5.4.4 Home-care & Long-term Care Settings

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Coloplast A/S

- 6.3.2 Boston Scientific Corporation

- 6.3.3 Becton, Dickinson and Company

- 6.3.4 Medtronic Plc

- 6.3.5 Johnson & Johnson (Ethicon)

- 6.3.6 Hollister Incorporated

- 6.3.7 B. Braun SE

- 6.3.8 ConvaTec Group plc

- 6.3.9 PROMEDON GmbH

- 6.3.10 AMI GmbH

- 6.3.11 Caldera Medical Inc.

- 6.3.12 Zephyr Surgical Implants

- 6.3.13 Teleflex Incorporated

- 6.3.14 Cardinal Health

- 6.3.15 UroMems SA

- 6.3.16 Neuspera Medical Inc.

- 6.3.17 Uroplasty Inc.

- 6.3.18 Kimberly-Clark Corporation

- 6.3.19 Essity AB

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment