PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061656

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061656

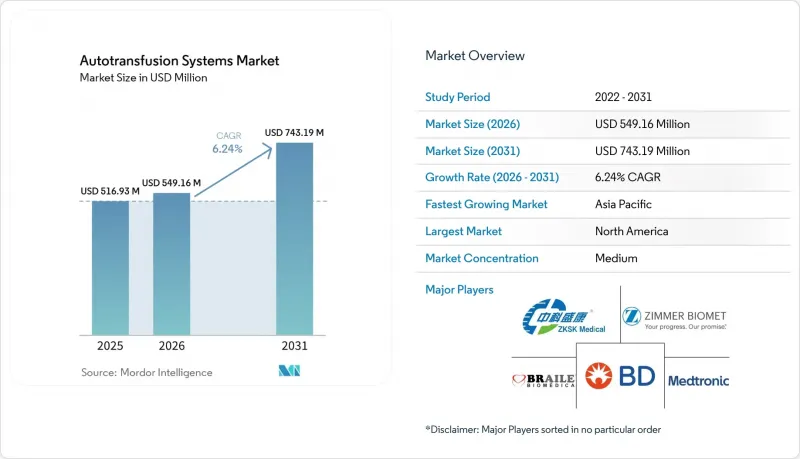

Autotransfusion Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the autotransfusion systems market size was valued at USD 516.93 million in 2025 and is estimated to grow from USD 549.16 million in 2026 to reach USD 743.19 million by 2031, at a CAGR of 6.24% during the forecast period (2026-2031).

This report is Segmented by Product Type (Devices and Consumables), Application (Cardiac Surgeries, Orthopedic Surgeries, Organ Transplantation, and Others), End-User (Hospitals, Ambulatory Surgical Centers, and Others), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Report Offers the Value (in USD Million) for the Above Segments.

Global Autotransfusion Systems Market Trends and Insights

Rising Volume & Complexity of Cardiac and Orthopedic Surgeries

Cardiac and orthopedic procedures grow in complexity, generating sizeable blood-loss volumes that make cell salvage indispensable. Cardiac operating rooms alone created 38.75% of 2024 demand, buoyed by uptake of transcatheter aortic valve replacements and multi-level spinal reconstructions. European trauma guidelines now instruct teams to deploy cell-salvage in severe bleeding, formalizing best practice . Aging populations amplify case volumes even as donor pools contract. Meta-analysis confirms a 39% cut in allogeneic transfusions when salvage is used across specialties. Consequently, the autotransfusion systems market becomes foundational operating-room infrastructure rather than an elective add-on.

Global Shortfall of Donor Blood and Stricter Transfusion Guidelines

The World Health Organization's patient-blood-management framework elevates autologous conservation to first-line status, compelling providers to adopt salvage systems as routine rather than contingency. In many African and Asian nations, annual donation deficits exceed 200,000 units, forcing hospitals to conserve every milliliter. Salvaged blood delivers fresher red cells and fewer immune reactions than stored alternatives, a benefit validated in controlled trials. Economically, each avoided unit saves hospitals upward of USD 500 in acquisition and complication costs, and full programs can return USD 1,367 per patient. With reimbursement aligning, the autotransfusion systems market benefits from a rare overlap of clinical, economic, and regulatory imperatives.

High Upfront Cost of Devices & Consumables Bundles

Turn-key systems range from USD 50,000 to USD 150,000, a steep outlay for budget-constrained clinics. Consumables add USD 200-400 per case, straining margins where reimbursement lags. Leasing and pay-per-use models mitigate sticker shock, yet adoption slows in smaller and public hospitals until such financing scales. Transitional Medicare coverage can offset risk, but global diffusion depends on broader payer alignment. The paradox remains: the sites that most need autotransfusion, those with severe donor shortages, often lack funds, tempering near-term market acceleration.

Other drivers and restraints analyzed in the detailed report include:

- Cost-Containment Pressures in Hospitals

- Technological Shift to Fully Automated, Low-Volume Cell-Salvage Devices

- Additive-Manufactured Disposables Lowering Device Capex

- Lack of Skilled Perfusionists or Technicians in Emerging Markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Devices contributed 61.72% of 2025 revenue, underscoring hospitals' reliance on durable capital platforms. Meanwhile, consumables are projected to deliver a 7.03% CAGR, reflecting rising procedure counts and razor-and-blade pricing. The autotransfusion systems market size attributed to devices reached USD 319.07 million in 2025, whereas consumables reached USD 197.86 million. Manufacturers invest in miniaturization and intuitive user interfaces, removing elective hardware features to lower prices without compromising safety. On the consumables side, printable reservoirs and color-coded tubing sets simplify setup and cut waste. Over the forecast horizon, widespread installed bases will create predictable repeat demand that underwrites R&D returns.

Second-order growth stems from the alignment of flexible financing with consumable contracts. Hospital networks increasingly prefer low-commitment device leases that scale to volume, a model that simultaneously locks in consumable supply at negotiated rates. This combination stabilizes revenue and shields providers from one-time capital hits, fueling expansion of the autotransfusion systems market among community hospitals.

Intraoperative salvage delivered 35.42% of 2025 revenue, validating its entrenched role during high-blood-loss cases. Yet proactive strategies-preoperative autologous donation and acute normovolemic hemodilution-are climbing at 6.79% CAGR, an indicator that surgical teams aim to curb allogeneic exposure before the first incision. Hospitals that integrate preoperative modules report double-digit declines in transfusion volume and smoother OR workflows. The autotransfusion systems market share for preoperative solutions remains modest but is widening as evidence crystallizes.

Post-operative drainage recovery sees steady uptake in cardiac and joint replacement wards where chest-tube or wound-vac outputs justify the incremental effort. Standardizing salvage across the perioperative continuum maximizes patient blood management, preparing institutions for heightened scrutiny under value-based reimbursement.

Geography Analysis

North America retained 42.78% revenue share in 2025 thanks to entrenched clinical protocols, Medicare reimbursement, and measured ASC expansion that generated USD 57.6 billion in projected savings over the next decade . U.S. hospitals documented USD 2 million in annual savings from comprehensive patient-blood-management initiatives, justifying continued investment in advanced salvage hardware. Canada exhibits parallel uptake within its publicly funded system as provinces set provincial blood-management targets.

Asia-Pacific is the growth locomotive, with an 8.53% CAGR projected through 2031. China's maternity hospitals demonstrate successful cell-salvage rollouts that halve allogeneic transfusions. Japan pioneers hemoglobin-vesicle substitutes now in human trials, a potential adjunct to, rather than replacement for, salvage systems by 2030. India, Indonesia, and Vietnam allocate development funds to equip tier-2 cities with modular ORs, creating prospects for entry-level but upgradeable devices.

Europe sustains mid-single digit growth as unified trauma and anesthesiology guidelines cement salvage as standard of care. Re-certification under the EU Medical Device Regulation spurs suppliers to update quality systems, weeding out non-compliant legacy equipment and favoring modern, automation-rich models.

The Middle East & Africa and South America remain under-penetrated but attract humanitarian and development-bank funding aimed at blood-security self-sufficiency. Portable, battery-operated kits gain traction in conflict-affected zones where donor pools are unstable. Over time, skill-building alliances between global manufacturers and local nursing schools will unlock these frontier markets.

- Haemonetics

- LivaNova

- Medtronic

- Beckton Dickinson

- Fresenius

- Zimmer Biomet

- Beijing ZKSK Technology

- Braile Biomedica

- Redax S.p.A.

- Gen World Medical Devices

- Teleflex

- Soma Tech INTL

- Terumo Cardiovascular Systems

- Brightwake Ltd (Hemosep)

- SARSTEDT AG & Co.

- Atrium Medical (Getinge)

- Vascular Solutions (Teleflex)

- Stryker

- Fresenius

- Johnson & Johnson

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Volume & Complexity Of Cardiac And Orthopedic Surgeries

- 4.2.2 Global Shortfall Of Donor Blood And Stricter Transfusion Guidelines

- 4.2.3 Cost-Containment Pressures In Hospitals Encouraging Blood-Conservation Technologies

- 4.2.4 Technological Shift To Fully Automated, Low-Volume Cell-Salvage Devices

- 4.2.5 Additive-Manufactured (3-D-Printed) Disposables Lowering Device Capex

- 4.2.6 Military & Disaster-Medicine Protocols Mandating Portable Autotransfusion Kits

- 4.3 Market Restraints

- 4.3.1 High Upfront Cost Of Devices & Consumables Bundles

- 4.3.2 Lack Of Skilled Perfusionists/Or Technicians In Emerging Markets

- 4.3.3 Haemolysis Risk In Haemolytic-Anemia & Paediatric Cohorts

- 4.3.4 Limited Clinical Evidence & Reimbursement In Obstetrics / Low-Resource Settings

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value - USD Million)

- 5.1 By Product Type

- 5.1.1 Devices

- 5.1.2 Consumables

- 5.2 By Procedure Phase

- 5.2.1 Intra-operative

- 5.2.2 Post-operative

- 5.2.3 Pre-operative (PAD & ANH)

- 5.3 By Application

- 5.3.1 Cardiac Surgeries

- 5.3.2 Orthopedic Surgeries

- 5.3.3 Organ Transplantation

- 5.3.4 Trauma Procedures

- 5.3.5 Others

- 5.4 By End-User

- 5.4.1 Hospitals

- 5.4.2 Ambulatory Surgical Centers

- 5.4.3 Specialty & Orthopedic Clinics

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Haemonetics Corporation

- 6.3.2 LivaNova PLC

- 6.3.3 Medtronic plc

- 6.3.4 Becton, Dickinson and Company

- 6.3.5 Fresenius Kabi AG

- 6.3.6 Zimmer Biomet

- 6.3.7 Beijing ZKSK Technology

- 6.3.8 Braile Biomedica

- 6.3.9 Redax S.p.A.

- 6.3.10 Gen World Medical Devices

- 6.3.11 Teleflex Incorporated

- 6.3.12 Soma Tech INTL

- 6.3.13 Terumo Cardiovascular Systems

- 6.3.14 Brightwake Ltd (Hemosep)

- 6.3.15 SARSTEDT AG & Co.

- 6.3.16 Atrium Medical (Getinge)

- 6.3.17 Vascular Solutions (Teleflex)

- 6.3.18 Stryker Corporation

- 6.3.19 Fresenius Medical Care

- 6.3.20 Johnson & Johnson (DePuy Synthes)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment