PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061665

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061665

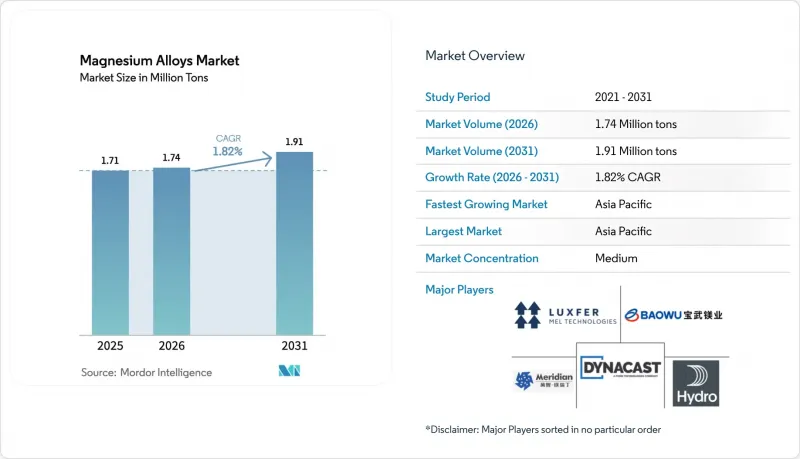

Magnesium Alloys - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the magnesium alloys market size is expected to grow from 1.71 million tons in 2025 to 1.74 million tons in 2026 and is forecast to reach 1.91 million tons by 2031 at a 1.82% CAGR over 2026-2031.

This report is Segmented by Alloy Type (Cast Alloys and Wrought Alloys), Processing Technology (Die Casting, Extrusion, Forging, Powder Metallurgy, and Additive Manufacturing Feedstock), Application (Chassis and Structural Components, and More), End-Use Industry (Automotive, Aerospace, and More), and Geography (Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Global Magnesium Alloys Market Trends and Insights

Mandatory EV Lightweighting Mandates Boost Magnesium Alloy Demand

Battery-electric vehicles (BEVs) are heavier than their combustion counterparts, prompting OEMs to reduce structural mass to reclaim lost range. China's 2027 New Energy Vehicle mandate sets a minimum range of 500 km on the CLTC, effectively necessitating a reduction in body-in-white weight. By utilizing magnesium extrusions and mega-cast subframes, which are lighter than aluminum, automakers can achieve these targets without enlarging their batteries. Following ISO 16220 corrosion-testing standards, certification for AZ31B front-end carriers has streamlined qualification timelines. While premium models currently shoulder the cost disparity, advancements in recycling hint at a broader acceptance of magnesium alloys, potentially penetrating deeper into mid-volume segments.

EU CO2 Fleet-Average Rules Accelerate Wrought Mg Extrusions Adoption

The EU has set a limit for emissions for 2025, which will gradually tighten by 2030. For every gram over the limit, there's a penalty. This has made light-weighting not just an option, but a necessity. Using direct-chill-cast and hot-extruded ZK60 profiles, manufacturers can reduce component mass while still achieving a yield strength of over 200 MPa. Magna has launched a new line in Austria, providing magnesium for each Audi PPE chassis. Coatings free from hexavalent chromium and certified under ISO 10074 not only alleviate REACH pressures but also expedite supplier onboarding, bolstering the growth outlook for the magnesium alloys market.

Galvanic and Pitting Corrosion Challenges in Humid Environments

Magnesium's -2.37 V potential renders it highly anodic. Consequently, when salt-laden moisture connects joints of dissimilar metals, pits develop over time. While plasma-electrolytic oxidation can prolong the salt-spray life, it comes with a significant capital expenditure. Although rare-earth alloying offers some benefits, its susceptibility to price fluctuations poses challenges. As a result, corrosion remains the primary hurdle preventing the broader adoption of magnesium alloys in mainstream vehicles.

Other drivers and restraints analyzed in the detailed report include:

- US FDA Clearances Spur Bio-Resorbable Mg Orthopedic Fixation Demand

- 5G Handset Makers Shift to Mg-Li Casting for EMI Shielding

- Welding Brittleness Versus Al and Ti Alloys

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cast alloys supplied 68.17% of shipments in 2025, reflecting their die-casting efficiency for intricate housings. Nonetheless, wrought grades are sprinting ahead at 6.36% CAGR. BMW's Neue Klasse platform will embed 22 kg of extruded AZ31B and ZK60 per car, sharpening the weight-saving edge essential to lithium-ion range optimization. Beyond cars, helicopter gearbox housings and UAV frames now specify ZK60A extrusions for vibration damping, underscoring broader diversification of the magnesium alloys market. Electronics still favor die-cast LA141 shells for 5G handsets, yet the design window is widening as additive-manufacturing powders enable lattice-filled implants that deliver biomechanical compatibility unmatchable by titanium.

In 2025, patented rare-earth-free wrought compositions emerged, addressing supply concerns and reducing material costs. While niche, the demand for gas-atomized WE43 powders in additive manufacturing enhances profitability and fuels research and development. Regulatory subsidies for recycling feedstock have led to an uptick in re-melting cast scrap into wrought billets. This not only shortens supply loops but also bolsters the sustainability credentials of the magnesium alloys market.

Die casting still commands 55.18% of throughput thanks to 45-90 s cycles and million-shot tooling life. Chinese OEMs are set to trial single-piece magnesium rear underbodies starting in 2027, having placed orders for large presses. Meanwhile, Magna's new line in Austria, catering to Audi's PPE, bolsters extrusions' market share. Additionally, advancements in press lubricants now facilitate the use of long AZ31 profiles.

Additive manufacturing grows at a 6.82% CAGR. EOS M290, utilizing WE43, achieves high density and yield strength directly from the powder bed, making it suitable for load-bearing ankle plates. Safety codes under ATEX 2014/34/EU have spurred investment in inert-gas print farms across Germany and Texas. Forging and powder metallurgy remain niche but benefit from demand in helicopter rotor hubs and lightweight bicycle cranks, keeping the magnesium alloys market diversified across processes.

Geography Analysis

Asia Pacific retains 46.19% of 2025 shipments and posts the fastest 6.87% CAGR through 2031. In 2025, China's Baowu bolstered its dominance by bringing new capacity online and cementing its primary market share. Meanwhile, BYD's Seal sedan is already integrating magnesium components. In a notable collaboration, Japan's Toyota and Panasonic are co-developing magnesium-lithium battery enclosures, hinting at a future cross-industry synergy. South Korea's leading handset manufacturers secured LA alloys in 2025, effectively bridging the supply-demand gap in the magnesium alloys market.

North America's market share is largely driven by industry giants Ford and GM, alongside the growing medical adoption of WE43 screws. US Magnesium's Great Salt Lake facility acts as a buffer for OEMs against geopolitical uncertainties. Highlighting the medical sector's momentum, Syntellix captured a share of the distal-radius fixation market just a year post-FDA approval. In Canada, Bombardier and CAE are utilizing extruded ZK60 for their simulation rigs, while in Mexico, Guanajuato die-casters are embedding magnesium into Q5 e-tron carriers.

Europe is navigating stringent CO2 regulations. In 2025, Germany, bolstered by recycling initiatives from Magna and Hydro that cut carbon footprints, consumed a notable amount of magnesium. The EU's mandate for recycled content is steering OEMs towards secondary feedstock contracts, reinforcing the region's commitment to circularity in the magnesium alloys market.

While South America and the Middle East and Africa may be smaller players, they are making significant strides. Brazil's INMETRO has harmonized local standards with ISO 16220, paving the way for domestic suppliers to cater to OEMs. In a forward-looking move, Saudi Arabia is set to unveil a Jubail smelter by 2028, adding new primary capacity to the market.

- AE Group

- AMACOR

- Baowu Magnesium Technology Co., Ltd.

- Dead Sea Magnesium Ltd.

- Dynacast

- Fugu County Industrial Magnesium Ltd.

- ICL

- Ka Shui International Holdings Ltd

- Luxfer MEL Technologies

- MAGONTEC Group

- Meridian Lightweight Technologies

- m-tec powder GmbH

- NIPPON KINZOKU co.,ltd.

- Norsk Hydro ASA

- Rima Group

- Shanghai Regal Metal Materials Co., Ltd.

- Shanxi Yinguang Huasheng Magnesium Industry Co., LTD

- Smiths Advanced Metals

- US Magnesium LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mandatory EV light-weighting mandates boost Magnesium Alloy demand

- 4.2.2 EU CO2 fleet-average rules accelerate wrought Mg extrusions adoption

- 4.2.3 US FDA clearances spur bio-resorbable Mg orthopedic fixation demand

- 4.2.4 5G handset makers shift to Mg-Li casting for EMI shielding

- 4.2.5 Closed-loop scrap recycling lowers effective cost of Mg alloys

- 4.3 Market Restraints

- 4.3.1 Galvanic and pitting corrosion challenges in humid environments

- 4.3.2 Welding brittleness versus Al and Ti alloys

- 4.3.3 High-strength 6xxx Al extrusions displace Mg for crash-relevant parts

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Alloy Type

- 5.1.1 Cast Alloys

- 5.1.2 Wrought Alloys

- 5.2 By Processing Technology

- 5.2.1 Die Casting

- 5.2.2 Extrusion

- 5.2.3 Forging

- 5.2.4 Powder Metallurgy

- 5.2.5 Additive Manufacturing Feedstock

- 5.3 By Application

- 5.3.1 Chassis and Structural Components

- 5.3.2 Powertrain and Drivetrain Components

- 5.3.3 Interior and Exterior Automotive Parts

- 5.3.4 Electronic Device Housings

- 5.3.5 Orthopedic and Cardiovascular Implants

- 5.3.6 Others

- 5.4 By End-use Industry

- 5.4.1 Automotive

- 5.4.2 Aerospace

- 5.4.3 Electronics

- 5.4.4 Medical

- 5.4.5 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 AE Group

- 6.4.2 AMACOR

- 6.4.3 Baowu Magnesium Technology Co., Ltd.

- 6.4.4 Dead Sea Magnesium Ltd.

- 6.4.5 Dynacast

- 6.4.6 Fugu County Industrial Magnesium Ltd.

- 6.4.7 ICL

- 6.4.8 Ka Shui International Holdings Ltd

- 6.4.9 Luxfer MEL Technologies

- 6.4.10 MAGONTEC Group

- 6.4.11 Meridian Lightweight Technologies

- 6.4.12 m-tec powder GmbH

- 6.4.13 NIPPON KINZOKU co.,ltd.

- 6.4.14 Norsk Hydro ASA

- 6.4.15 Rima Group

- 6.4.16 Shanghai Regal Metal Materials Co., Ltd.

- 6.4.17 Shanxi Yinguang Huasheng Magnesium Industry Co., LTD

- 6.4.18 Smiths Advanced Metals

- 6.4.19 US Magnesium LLC

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Increasing 3D Printing and Additive Manufacturing