PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061669

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061669

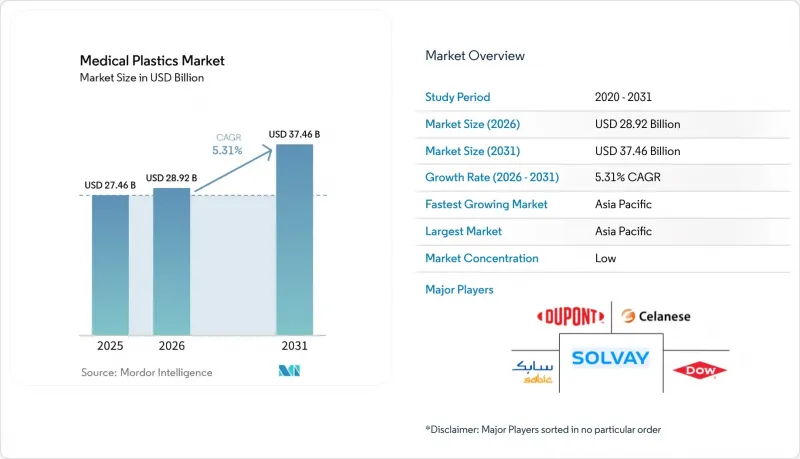

Medical Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the medical plastics market size is expected to grow from USD 27.46 billion in 2025 to USD 28.92 billion in 2026 and is forecast to reach USD 37.46 billion by 2031 at 5.31% CAGR over 2026-2031.

This report Segments the Industry by Type (Traditional Plastics and Engineering Plastics), Process (Injection Molding, Extrusion, Blow Molding, and More), Application (Disposables, Sterilization Trays, Surgical Instruments, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Medical Plastics Market Trends and Insights

Shift toward Home-Based Care Requiring Lightweight Single-Use Devices

Healthcare delivery is moving from hospital wards to living rooms, urging designers to prioritize portability, intuitive interfaces, and strict infection control. Lightweight, single-use polypropylene, polycarbonate, and PEEK components tolerate steam, ethylene oxide, and radiation cycles while keeping weight low, a vital attribute for wearable pumps and point-of-care diagnostics. The PDA Miniverse Conference 2025 emphasized that home-care models also catalyze digital monitoring solutions, compelling polymers to protect sensitive sensors and batteries. Single-use product expansion answers infection-prevention protocols but makes waste management a parallel priority. Suppliers that can balance sterility, strength, and recyclability position themselves for long-term gains in the medical plastics market.

Miniaturization of Catheters and Wearables Elevating Demand for High-Purity Polycarbonate

Cardiovascular and neurovascular surgeons favor slimmer, more flexible catheters that navigate tortuous anatomy. High-purity polycarbonate, such as Covestro's Makrolon, delivers transparency, dielectric strength, and dimensional stability, supporting catheter walls below 0.4 mm without compromising burst pressure. Wearable heart monitors increasingly embed optical sensors and micro-batteries; polycarbonate's clarity and sterilization compatibility allow extended use in ambulatory settings. The resulting material pull-through strengthens the market across diagnostic and therapeutic devices alike.

Environmental Concerns Regarding Medical Plastics

Healthcare facilities generate 70% of sanitary waste by volume, mostly single-use plastics. The EU Single-Use Plastics Directive is already restricting certain polymer formats, while the U.S. Environmental Protection Agency aims to eliminate plastic leakage by 2040. These policies encourage material substitution, lower packaging weights, and drive audits of scope-3 emissions. Manufacturers that invest early in compostable resins, mono-material designs, and take-back schemes mitigate compliance risk, yet face margin pressure. Sustainability metrics will therefore shape procurement decisions and could temper traditional volume growth in the medical plastics market.

Other drivers and restraints analyzed in the detailed report include:

- Government Incentives for Domestic Medical-Device Manufacturing in Asia

- Rapid Adoption of 3-D-Printed Patient-Specific Implants Accelerating PEEK Utilization

- Limited Recycling Infrastructure for Medical-Grade Plastics Heightens Disposal Expenses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polypropylene accounted for 25.83% of the medical plastics market share in 2025, anchored in syringes, IV bags, and catheter hubs that require chemical resistance and steam-autoclave tolerance. The material's density of 0.9 g/cm3 supports lighter shipping loads, reinforcing its cost advantage. Polymer scientists are exploring catalytic depolymerization to transform spent PP masks into ECG electrodes, an initiative that could lower landfill volumes while adding value.

PEEK is projected to log a 5.62% CAGR to 2031, outpacing all other engineering resins. Demand stems from spinal cages, dental abutments, and cranial plates printed to patient CT data. The medical plastics market size for PEEK-based implants is poised to expand as material suppliers commercialize high-flow grades that shorten print cycles without sacrificing crystallinity. Radiolucency and modulus matching make PEEK attractive versus titanium, and emerging recycling programs for machining scraps enhance its sustainability profile.

Geography Analysis

Asia-Pacific captured 41.12% of the market in 2025 and is forecast to widen its lead at a 5.76% CAGR. China's export of medical devices to ASEAN hit USD 4.4 billion in 2023, a testament to regionalized supply chains. Japan contributes precision molding know-how that supports high-end diagnostic components. These dynamics position Asia as both a manufacturing hub and a consumption epicenter for the medical plastics market.

North America remains the innovation nucleus, especially for 3-D-printed implants and connected therapeutics. Stringent FDA class-II and class-III standards drive the adoption of resins with well-documented biocompatibility, and hospital construction trends favor modular outpatient clinics needing lightweight, recyclable fixtures.

Europe approaches the market through a sustainability prism. The Single-Use Plastics Directive pressures device makers to switch from styrenics to lower-impact copolymers or biodegradable alternatives. In Germany and the Netherlands, pilot recycling hubs are testing closed-loop programs for PET tracer vials and PVC masks. Academic-industry consortia funded under Horizon Europe add to the research pipeline that targets circular medical plastics market solutions. Meanwhile, South America and the Middle-East and Africa expand baseline healthcare infrastructure, prioritizing affordable disposables and basic diagnostic kits as entry points.

- BASF

- Celanese Corporation

- Covestro

- Dow

- dsm-firmenich

- DuPont

- Eastman Chemical Company

- Ensinger

- Evonik Industries AG

- Mitsubishi Chemical Group Corporation

- Nolato AB

- RAUMEDIC AG

- Rochling SE & Co. KG

- RTP Company

- SABIC

- Saint-Gobain

- Solvay

- Teknor Apex

- Westlake Plastics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift Toward Home-Based Care Requiring Lightweight Single-Use Devices

- 4.2.2 Miniaturization of Catheters and Wearables Elevating Demand for High-Purity Polycarbonate in Cardiovascular Applications

- 4.2.3 Government Incentives for Domestic Medical-Device Manufacturing in Asia

- 4.2.4 Rapid Adoption of 3-D Printed Patient-Specific Implants Accelerating PEEK Utilization Globally

- 4.2.5 Growth of Connected Drug-Delivery Pumps Driving Use of Transparent, Chemically-Resistant Polymers

- 4.3 Market Restraints

- 4.3.1 Environmental Concerns Regarding Medical Plastics

- 4.3.2 Limited Recycling Infrastructure for Medical-Grade Plastics Heightening Disposal Expenses

- 4.3.3 Increasing Competition from Alternative Materials

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Traditional Plastics

- 5.1.1.1 Polyethylene (PE)

- 5.1.1.2 Polypropylene (PP)

- 5.1.1.3 Polystyrene (PS)

- 5.1.1.4 Polyvinyl Chloride (PVC)

- 5.1.2 Engineering Plastics

- 5.1.2.1 Acrylonitrile-Butadiene-Styrene (ABS)

- 5.1.2.2 Polycarbonate (PC)

- 5.1.2.3 Polymethyl-Methacrylate (PMMA)

- 5.1.2.4 Polyether-Ether-Ketone (PEEK)

- 5.1.2.5 Polyoxymethylene (POM)

- 5.1.2.6 Polyphenylene Oxide (PPO)

- 5.1.2.7 Other Engineering Plastics

- 5.1.1 Traditional Plastics

- 5.2 By Process

- 5.2.1 Injection Molding

- 5.2.2 Extrusion

- 5.2.3 Blow Molding

- 5.2.4 3-D Printing / Additive Manufacturing

- 5.2.5 Others (Compression, Thermoforming)

- 5.3 By Application

- 5.3.1 Disposables

- 5.3.2 Sterilization Trays

- 5.3.3 Surgical Instruments

- 5.3.4 Diagnostic Instruments

- 5.3.5 Anasthetics and Imagining Equipments

- 5.3.6 Others (Drug-Delivery Devices, Pharmaceutical and Device Packaging)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacifc

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 BASF

- 6.4.2 Celanese Corporation

- 6.4.3 Covestro

- 6.4.4 Dow

- 6.4.5 dsm-firmenich

- 6.4.6 DuPont

- 6.4.7 Eastman Chemical Company

- 6.4.8 Ensinger

- 6.4.9 Evonik Industries AG

- 6.4.10 Mitsubishi Chemical Group Corporation

- 6.4.11 Nolato AB

- 6.4.12 RAUMEDIC AG

- 6.4.13 Rochling SE & Co. KG

- 6.4.14 RTP Company

- 6.4.15 SABIC

- 6.4.16 Saint-Gobain

- 6.4.17 Solvay

- 6.4.18 Teknor Apex

- 6.4.19 Westlake Plastics

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment

- 7.2 Increasing Investment in 3-D Printing and Imaging Technologies