PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061673

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061673

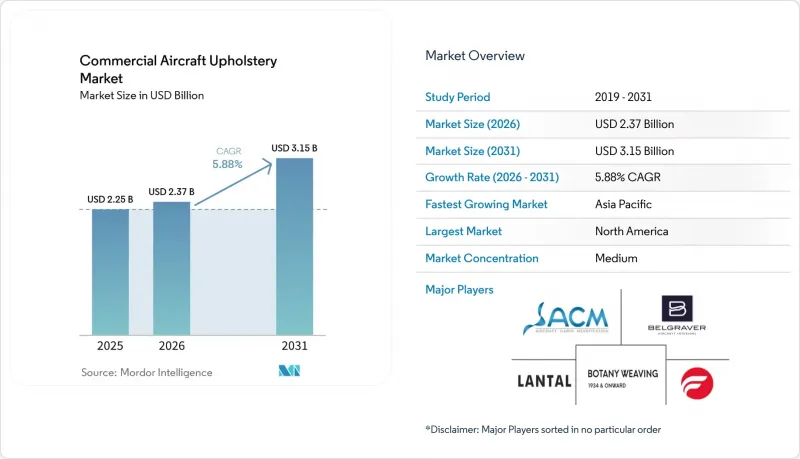

Commercial Aircraft Upholstery - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the commercial aircraft upholstery market size is expected to grow from USD 2.25 billion in 2025 to USD 2.37 billion in 2026 and is forecasted to reach USD 3.15 billion by 2031 at a 5.88% CAGR over 2026-2031.

This report is Segmented by Aircraft Type (Narrowbody, Widebody, Regional Jets, and Business Jets), Seat Type (First Class, Business Class, Premium Economy Class, and Economy Class), Seat Cover Type (Bottom Covers, Back Rests, Headrests, Armrests, and More), End Use (OEM and Aftermarket), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Commercial Aircraft Upholstery Market Trends and Insights

Expansion of Narrowbody Aircraft Fleets and Delivery Backlogs

Airbus plans to raise A320-family output to 75 per month in 2027, while Boeing reported strong net orders in 2025 that underpin sustained linefit demand for seat covers, headrests, armrests, and bottom covers. Airlines in fast-growing Asian markets are set to absorb a large share of these units, which reinforces the tilt of the commercial aircraft upholstery market toward high-usage narrowbody layouts. China's long-range fleet outlook points to large-scale requirements that drive cabin program volume, which steers upholstery specifications toward durable, lightweight synthetics that maintain comfort at higher seat densities. Backlogs and component lead times complicate synchronization between airframe delivery slots and interior kit availability, which lifts short-term demand for certified retrofit packages. The net effect is a steady pull on approved materials and modular assemblies in the commercial aircraft upholstery market as OEM build rates rise and MRO networks turn more airframes within compressed windows.

Rising Frequency of Cabin Refurbishment Cycles with Focus on Passenger Experience

Airlines now plan refresh cycles every 5-7 years to maintain brand consistency and service standards, thereby increasing the throughput of seat dress covers and soft goods in the commercial aircraft upholstery market. First-class and business-class cabins are refurbished every 5-7 years, whereas economy-class cabins are updated every 6-10 years. High-profile cabin upgrade programs by major carriers, including widebody retrofits, highlight the focus on premium experiences and consistent product across fleets. Modular kits that bundle headrests, armrests, and bottom covers enable faster turnarounds and fewer ground days, which reduces revenue loss during refurbishment. Cleaner designs and better foam support have improved seat comfort and durability without weight penalties, which raises passenger satisfaction scores after upgrades. The shift to faster cycles and standardized kits supports stable demand in both OEM and aftermarket channels within the commercial aircraft upholstery market.

Volatility in Raw Material Prices Affecting Cost Stability

Input prices for metals and advanced textiles have risen since 2024, compressing supplier margins and complicating long-term pricing for airframers and airlines. Upholstery specialists have responded by increasing yield from fabrics through better nesting and by substituting lighter, certified alternatives where performance allows. These measures help curb cost spikes but do not remove exposure to swings in aluminum, titanium, or composite inputs used in seat structures and subcomponents that interact with soft goods. Airlines balance these pressures by sequencing cabin refreshes to coincide with planned checks and by locking in material volumes earlier. The result is greater emphasis on digital cutting, robotic sewing, and modular kits that limit waste and rework in the commercial aircraft upholstery market.

Other drivers and restraints analyzed in the detailed report include:

- Proliferation of Premium Economy Seating Across Airlines

- Growing Demand for Antimicrobial and Easy-to-Clean Upholstery Materials

- Burden of Certification and Compliance Requirements for Aviation Textiles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Narrowbody jets commanded a 41.55% revenue share in 2025, positioning single-aisle programs as the core demand engine in the commercial aircraft upholstery market. OEM rate targets and robust order books sustain linefit throughput for seat covers and soft furnishings on A320-family and B737-family programs. Fleet strategies in Asia-Pacific and North America prioritize high-frequency operations with denser seating plans, which push higher-wear material specifications into dress cover programs. Airlines also use shorter refresh cycles to protect brand consistency on popular routes, which drives repeat demand across headrests, bottom covers, and armrests. Suppliers that can pre-certify kits for these platforms gain scheduling flexibility and lower risk of disruption in the commercial aircraft upholstery market.

Business jets are experiencing the fastest expansion, with a 6.15% CAGR through 2031, as corporate travel budgets normalize and premium cabin comfort becomes a priority. The ability to tailor soft goods to bespoke interiors supports higher value per shipset, and refurbishment cycles often align with ownership changes or brand refreshes. OEM and completion centers weigh softness, texture, and durability while meeting fire standards, which improves the demand mix in premium leathers and high-grade synthetics. Integration of antimicrobial treatments has also moved into business aviation, where operators prefer easy-clean solutions that protect cabin quality between frequent short sectors. These dynamics add a stable growth layer alongside narrowbody-led volume in the commercial aircraft upholstery market.

Economy class accounted for 48.34% of revenue in 2025, reflecting its scale across the global fleet in the commercial aircraft upholstery market. Airlines pursue slimline seat designs to reduce weight and preserve comfort through better foams and textiles. Cover materials must retain color and hand feel after repeated cleaning, which favors resilient synthetics with durable coatings. Program managers now structure soft goods to simplify swaps and limit aircraft out-of-service days. These steps preserve uptime and maintain cabin-quality targets in the commercial aircraft upholstery market.

Premium economy is the fastest-growing seat type with a 6.92% CAGR projected through 2031, and it continues to expand across long-haul and selected medium-haul routes. Carriers have publicized deployments that add premium-economy rows and upgraded upholstery with wider armrests and improved lumbar support. Published examples include enhancements by global airlines, such as the rollout of refreshed cabins and premium seating footprints, which direct higher-spec soft goods into the pipeline. Operators report stronger unit revenues from premium-economy zones, which sustains the configuration shift underway. The mix tilt supports a richer margin structure for suppliers in the commercial aircraft upholstery market as premium specifications scale across fleets.

Geography Analysis

North America accounted for 32.87% of revenue in 2025, reflecting the weight of US carriers, MRO infrastructure, and strict fire-retardant compliance under FAR 25.853, which supports premium materials and robust documentation. Fleet-wide refresh programs at major US airlines have been ongoing since late 2024, which raised demand for seat dress covers and complementary soft goods in scheduled checks. FAA certification frameworks require disciplined test evidence for interior materials, which favors incumbents and suppliers with established flammability and toxicity data sets. As airlines install connectivity and new IFE hardware, they tend to refresh soft goods in the same window to reduce downtime. These conditions keep North America a stable anchor of the commercial aircraft upholstery market.

Asia-Pacific leads growth with a projected 7.46% CAGR through 2031, driven by airline expansion and narrowbody fleet additions across domestic and regional networks. China's long-term outlook indicates significant aircraft additions that will require scaled upholstery supply near key hubs, and India's largest carriers are advancing multi-hundred-unit orders that sustain interiors demand. Local certification pathways can add complexity to imported parts, increasing the value of local finishing, testing, and inventory. As airlines densify cabins to meet rising traffic, upholstery specifications tilt toward high-durability synthetics with antimicrobial and easy-clean properties. These dynamics are expected to raise the region's share of the commercial aircraft upholstery market over the forecast period.

Europe benefits from strong OEM and supplier ecosystems, as well as regulatory leadership from EASA and material restrictions under EU REACH, which shift the mix toward inherently flame-resistant wool blends and bio-based synthetics. Premium-economy adoption continues across European flag carriers, which lifts the share of higher-spec covers and armrests in refurbishment programs. The region also supports textile innovators and circular-material platforms, including recycled or composite leather alternatives that meet tactile and sustainability targets. As testing timelines lengthen for new chemistries, suppliers rely on pre-vetted formulations and test data to maintain program schedules. These patterns maintain a balanced demand profile across OEM lines and retrofits in the commercial aircraft upholstery market.

- Aircraft Cabin Modification GmbH

- Belgraver B.V.

- Botany Weaving Mill Limited

- LANTAL TEXTILES AG

- Franklin Products, Inc.

- Perrone Leather LLC

- Spectra Interior Products, Inc.

- MGR Foamtex Ltd.

- Generation Phoenix Limited

- Tapis Corporation

- FU-CHI INNOVATION TECHNOLOGY CO., LTD.

- J&C AERO, UAB

- 4Drive & Aviation

- New United Goderich Inc.

- Duncan Aviation Inc.

- ACC COLUMBIA Jet Service GmbH

- Aerotex Interiors Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of narrowbody aircraft fleets and delivery backlogs

- 4.2.2 Rising frequency of cabin refurbishment cycles with focus on passenger experience

- 4.2.3 Proliferation of premium economy seating across airlines

- 4.2.4 Growing demand for antimicrobial and easy-to-clean upholstery materials

- 4.2.5 Increasing adoption of sustainable, lightweight, and composite leather alternatives

- 4.2.6 Integration of digital and automated manufacturing technologies in upholstery

- 4.3 Market Restraints

- 4.3.1 Volatility in raw material prices affecting cost stability

- 4.3.2 Burden of certification and compliance requirements for aviation textiles

- 4.3.3 Dependence on a concentrated supply chain of certified upholstery materials

- 4.3.4 Industry transition driven by ESG mandates away from animal-based leather

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Aircraft Type

- 5.1.1 Narrowbody

- 5.1.2 Widebody

- 5.1.3 Regional Jets

- 5.1.4 Business Jets

- 5.2 By Seat Type

- 5.2.1 First Class

- 5.2.2 Business Class

- 5.2.3 Premium Economy Class

- 5.2.4 Economy Class

- 5.3 By Seat Cover Type

- 5.3.1 Bottom Covers

- 5.3.2 Back Rests

- 5.3.3 Headrests

- 5.3.4 Armrests

- 5.3.5 Seat Rear Pockets

- 5.4 By End Use

- 5.4.1 Original Equipment Manufacturer (OEM)

- 5.4.2 Aftermarket

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Aircraft Cabin Modification GmbH

- 6.4.2 Belgraver B.V.

- 6.4.3 Botany Weaving Mill Limited

- 6.4.4 LANTAL TEXTILES AG

- 6.4.5 Franklin Products, Inc.

- 6.4.6 Perrone Leather LLC

- 6.4.7 Spectra Interior Products, Inc.

- 6.4.8 MGR Foamtex Ltd.

- 6.4.9 Generation Phoenix Limited

- 6.4.10 Tapis Corporation

- 6.4.11 FU-CHI INNOVATION TECHNOLOGY CO., LTD.

- 6.4.12 J&C AERO, UAB

- 6.4.13 4Drive & Aviation

- 6.4.14 New United Goderich Inc.

- 6.4.15 Duncan Aviation Inc.

- 6.4.16 ACC COLUMBIA Jet Service GmbH

- 6.4.17 Aerotex Interiors Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment