PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061674

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061674

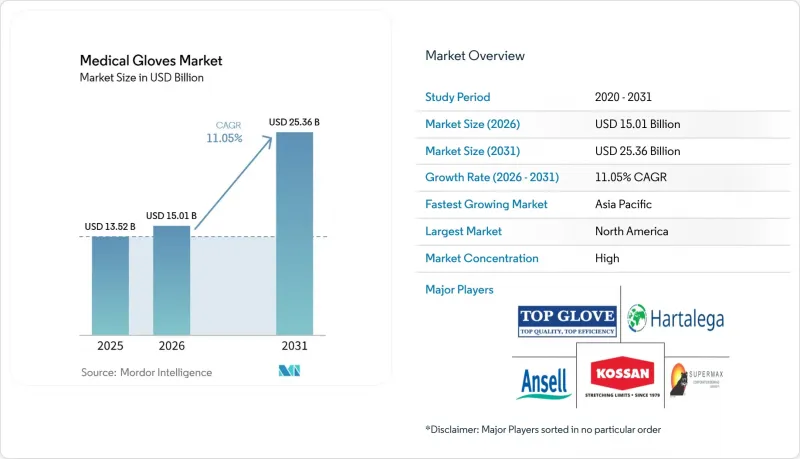

Medical Gloves - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the medical gloves market size was valued at USD 13.52 billion in 2025 and is estimated to grow from USD 15.01 billion in 2026 to reach USD 25.36 billion by 2031, at a CAGR of 11.05% during the forecast period (2026-2031).

This report Segments the Industry Into by Type (Powdered, Non-Powdered), by Material (Natural Rubber Gloves, Nitrile Gloves, Vinyl Gloves, Other Materials), by Application (Medical Examination, Surgery, Chemotherapy, Other Applications), and by Geography (North America, Europe and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Medical Gloves Market Trends and Insights

Global Emphasis on Preventing Hospital-Acquired Infections

Hospitals are tightening glove protocols after the Centers for Disease Control and Prevention confirmed that one in 31 in-patients acquires at least one infection each day. Facilities are moving from simple availability of gloves to procedure-specific selection, which favors indicator products for high-risk surgeries. A 2024 systematic review showing an 80 % drop in inner-glove perforations with double gloving has accelerated uptake of these premium variants. The new focus creates an insight that infection-control committees now analyse glove-use data in electronic dashboards alongside hand-hygiene metrics, embedding glove adherence into daily clinical reporting.

Rebound in Elective and Non-Urgent Surgical Procedures Post-Pandemic

Top Glove reported a 104 % year-on-year jump in sales volume for Q1 FY2025 as hospitals attack procedure backlogs . Orthopedic and cardiovascular cases are rising fastest, each demanding gloves with fine tactile response and high puncture resistance. Surgeons adopting minimally invasive techniques now specify ultra-thin nitrile or polyisoprene layers to improve grip on delicate instruments. A practical inference is that the higher glove consumption per complex case is offsetting slowing growth in routine examinations, keeping overall unit demand on a strong upward slope.

Volatile Natural Rubber Pricing Driven by Climate-Linked Yield Shifts

Climate variability is shrinking latex supply and driving unpredictable price swings that complicate cost forecasts for glove makers. The United States recently issued a waiver noting domestic shortfalls in nitrile-butadiene rubber feedstock, highlighting supply fragility even for synthetic options madeinamerica.gov. Manufacturers with vertical integration into chemical production can buffer these shocks, maintaining steadier pricing for hospital buyers. A clear inference is that access to diversified raw materials is becoming a core competitive moat, influencing lender perceptions of credit risk in the Medical Gloves industry.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Cleanroom Manufacturing Across Semiconductor and Pharma Industries

- Broader Adoption of Universal Health Coverage in Emerging Economies

- Rising Allergic/Hypersensitivity Concerns Prompting Powdered Glove Bans

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Examination gloves hold a 62.94 % Medical Gloves market share in 2025, underpinning daily patient care with cost-effective barrier protection. The segment's volume allows factories to run long continuous lines, achieving economies that keep prices stable even amid feedstock swings. A fresh inference is that home-health kits shipped for telemedicine visits now include single-pair exam gloves, adding a modest but growing consumer channel.

Cleanroom gloves capture a modest slice of Medical Gloves market size yet grow at 11.92 % CAGR, the fastest of all product types. Demand comes from semiconductor and pharma plants that require ISO Class 1-3 compliance and electrostatic control. Manufacturers able to certify both sterility and low particulate generation win premium contracts. An observed implication is that cross-training sales teams for industrial and healthcare accounts boosts utilization of cleanroom lines.

Surgical gloves account for lower volume but higher revenue per thousand pieces because of stricter sterility and tactile demands. A 2025 study found that latex-free surgical gloves are 4.24 times more prone to perforation than latex, driving R&D into composite films doi.org. Hospitals are trialling double-layer polyisoprene designs that combine sensitivity with backup integrity, signaling possible market share shifts within the surgical subset.

Nitrile gloves own a commanding 47.82 % Medical Gloves market share in 2025, prized for broad chemical resistance and the absence of natural-rubber proteins. Their supply chain, however, is sensitive to acrylonitrile and butadiene feedstock prices, which have stayed elevated since late 2023. To insulate margins, top manufacturers are co-locating nitrile plants with glove factories, cutting transit and storage costs. Neoprene gloves, meanwhile, are growing at a 12.22 % CAGR, accelerated by surgical departments seeking latex-like elasticity minus protein allergens. One side effect is that polychloroprene demand is outpacing upstream supply, nudging chemical companies to reopen mothballed capacity.

Latex still holds a niche in procedures that require unmatched tactile fidelity, especially microneurosurgery. Vinyl remains the lowest-cost alternative for non-critical tasks, yet its weak barrier properties confine use to quick-turn applications. Polyisoprene, though premium-priced, is carving out space as a bridge between latex performance and nitrile safety. Regulatory trends under the FDA's Quality Management System Regulation are catalyzing broader adoption of materials with stable supply profiles, encouraging R&D programs that emphasize recyclability and lower carbon intensity.

Geography Analysis

North America contributes 34.45 % of Medical Gloves market size in 2025, supported by advanced infrastructure and stringent infection-control rules. The region is reshaping sourcing after a 10 % tariff on Chinese gloves took effect in February 2025, steering orders toward Malaysian producers mida.gov.my. Distributors increasingly require suppliers to certify recycled content, signaling that green credentials are turning into market-entry tickets. An inference is that North American hospitals are bundling glove purchases within broader personal-protective-equipment contracts to leverage volume discounts.

Asia-Pacific is the fastest-growing geography with a 13.02 % CAGR outlook from 2026-2031. Malaysia alone manufactures 100 billion gloves annually, while Thai and Vietnamese producers expand automated lines. Domestic demand is also climbing as universal health insurance widens access to care across the region. One inference is that Asian governments adding gloves to national stockpiles create a built-in demand floor that cushions producers during global downturns.

Europe commands significant Medical Gloves market share thanks to universal coverage and strict chemical-safety laws. The EU Medical Device Regulation forces suppliers to document the absence of harmful substances, driving uptake of accelerator-free nitrile. Updated EU GMP Annex 1 tightens sterile manufacturing rules for pharma plants, bolstering demand for validated sterile gloves. An inference is that European hospital groups piloting glove-recycling loops could spark similar initiatives in North America once proof of cost savings emerges.

- Top Glove

- Hartalega Holdings

- Ansell

- Kossan Rubber Industries

- Supermax

- Semperit

- Cardinal Health

- Medline Industries

- Molnlycke Health Care

- O&M Halyard (Owens & Minor)

- B. Braun

- 3M

- Mckesson

- Kimberly-Clark Worldwide

- Intco Medical Technology Co. Ltd.

- Shandong Blue Sail Plastic & Rubber Co. Ltd.

- Showa Group

- Rubberex Corp.

- UG Healthcare Corporation

- Renco

- Dynarex

- Kanam Latex Industries Pvt. Ltd.

- Comfort Rubber Gloves Industries Sdn Bhd

- Liberty Glove & Safety

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Global Emphasis on Preventing Hospital-Acquired Infections

- 4.2.2 Rebound in Elective & Non-Urgent Surgical Procedures Post-Pandemic

- 4.2.3 Expansion of Cleanroom Manufacturing Across Semiconductor & Pharma Industries

- 4.2.4 Broader Adoption of Universal Health Coverage in Emerging Economies

- 4.2.5 Rapid Growth of Home-Based Point-of-Care Diagnostics

- 4.2.6 Government Incentives Catalyzing New Glove Manufacturing Capacity

- 4.3 Market Restraints

- 4.3.1 Volatile Natural Rubber Pricing Driven by Climate-Linked Yield Shifts

- 4.3.2 Rising Allergic/Hypersensitivity Concerns Prompting Powdered Glove Bans

- 4.3.3 Regulatory Approval Back-Logs Delaying New Product Launches

- 4.3.4 Increasing Carbon-Footprint Compliance Costs for Manufacturers

- 4.4 Value-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value - USD)

- 5.1 By Product Type

- 5.1.1 Examination Gloves

- 5.1.2 Surgical Gloves

- 5.1.3 Cleanroom Gloves

- 5.2 By Material Type

- 5.2.1 Nitrile

- 5.2.2 Latex

- 5.2.3 Vinyl

- 5.2.4 Neoprene

- 5.2.5 Polyisoprene

- 5.3 By Sterility

- 5.3.1 Sterile

- 5.3.2 Non-Sterile

- 5.4 By End User

- 5.4.1 Hospitals & Clinics

- 5.4.2 Ambulatory Surgery Centers

- 5.4.3 Diagnostic Laboratories

- 5.4.4 Home Healthcare Settings

- 5.4.5 Dental Practices

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Top Glove Corporation Bhd

- 6.4.2 Hartalega Holdings Berhad

- 6.4.3 Ansell Limited

- 6.4.4 Kossan Rubber Industries Bhd

- 6.4.5 Supermax Corporation Berhad

- 6.4.6 Semperit AG Holding

- 6.4.7 Cardinal Health Inc.

- 6.4.8 Medline Industries LP

- 6.4.9 Molnlycke Health Care AB

- 6.4.10 O&M Halyard (Owens & Minor)

- 6.4.11 B. Braun Melsungen AG

- 6.4.12 3M Company

- 6.4.13 McKesson Corporation

- 6.4.14 Kimberly-Clark Corporation

- 6.4.15 Intco Medical Technology Co. Ltd.

- 6.4.16 Shandong Blue Sail Plastic & Rubber Co. Ltd.

- 6.4.17 Showa Group

- 6.4.18 Rubberex Corp.

- 6.4.19 UG Healthcare Corporation

- 6.4.20 Renco Corporation

- 6.4.21 Dynarex Corporation

- 6.4.22 Kanam Latex Industries Pvt. Ltd.

- 6.4.23 Comfort Rubber Gloves Industries Sdn Bhd

- 6.4.24 Liberty Glove & Safety

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment