PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061682

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061682

Targeting Pods - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

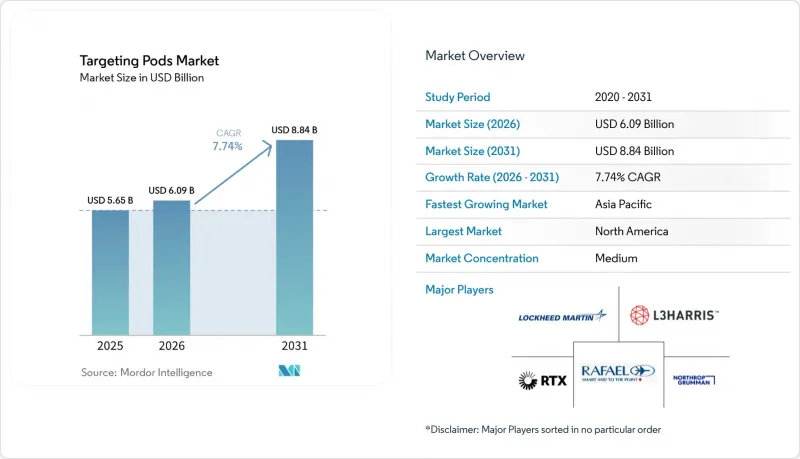

According to Mordor Intelligence, the targeting pods market size in 2026 is estimated at USD 6.09 billion, growing from 2025 value of USD 5.65 billion with 2031 projections showing USD 8.84 billion, growing at 7.74% CAGR over 2026-2031.

This report is Segmented by Platform (Combat Aircraft, Unmanned Combat Aerial Systems, Attack Helicopters, and Bombers), Fit (OEM and Retrofit), Pod Type (FLIR and Laser-Designator Pods, and More), Technology (Electro-Optical Imaging, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Targeting Pods Market Trends and Insights

Growing Procurement of Advanced Combat Aircraft in Emerging Economies

Middle-income nations are expanding fighter inventories to deter regional threats, elevating demand for high-end targeting pods market solutions. The Philippines earmarked USD 35 billion for a ten-year modernization program that includes advanced fighters and associated sensor suites. Southeast Asian air forces are evaluating diversified supply options, such as the UAE's interest in South Korea's KF-21 Boramae priced near USD 65 million per unit. These procurements prioritize precision engagement over fleet size, reinforcing the targeting pods market as a cost-effective force multiplier.

Up-gradation Programs for 4th/5th-Generation Aircraft Fleets

Extensive retrofit initiatives sustain long-term contracts for targeting pod vendors. Poland's USD 90.68 million purchase of Sniper pods for FA-50s illustrates how air forces extend combat relevance without acquiring entirely new fleets. The US Air Force LITENING Large Aperture upgrade boosts resolution and range by 50%, providing incremental capability gains on installed platforms.

High Acquisition and Life-Cycle Costs

Escalating aircraft prices amplify affordability challenges; the F-35 exceeded USD 140 million per unit in earlier lots, and next-generation fighters may cross USD 300 million, making high-spec pods a sizeable additive cost. Long-term sustainment demands specialized software maintenance and sensor recalibration, adding pressure on operating budgets.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Precision-Guided Munitions

- Increasing Global Defense Budgets

- Export-Control/ITAR Restrictions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Combat aircraft are set to command a dominant 62.05% share of the targeting pods market in 2025, driven by increasing defense budgets and the growing need for advanced targeting systems. Yet, unmanned combat aerial systems are set to grow at 9.63% CAGR as of 2026-2031. SkyTower II integration on MQ-9 Reapers exemplifies how lightweight, thermally efficient pods meet stringent size-weight-power limits. General Atomics' airborne-laser pod trials on the MQ-9B further highlight the expanding mission envelope that drives advanced cooling and power-management solutions. Attack helicopters and strategic bombers employ specialized pods for close support and long-range precision strike. At the same time, collaborative teaming-such as MQ-28 Ghost Bat operations alongside E-7A Wedgetail-imposes stringent networking requirements that only next-generation pods can fulfill.

Follow-on demand arises from national drone programs that rely on pods for autonomous targeting. The Marine Corps' smart-sensor package for MQ-9 systems highlights convergence between manned and unmanned mission profiles. Consequently, the targeting pods market continues evolving toward lighter, modular payloads compatible with both traditional aircraft and low-observable drones, ensuring sustained revenues for sensor integrators.

Original-equipment fits represent 68.10% of 2025 revenue, illustrating the baseline integration on newly built platforms. Yet retrofit demand, growing at 8.78% CAGR, signals the air force's preference for phased modernization. The targeting pods market size attached to retrofit installations gains from planned mid-life upgrades such as Singapore's F-16V program, which adds AESA radar and new avionics alongside pod replacements. OEMs supply hardware kits and software patches that convert legacy systems into network-ready assets.

Retrofits compress lead times and reduce pilot-retraining costs. Digital backbones installed on many fighters simplify plug-and-play pod insertion, reinforcing budgetary appeal. As a result, retrofit opportunities will remain a stable revenue pillar within the targeting pods industry despite the emergence of all-new platforms.

Geography Analysis

North America retains leadership with 37.90% 2025 revenue as sustained Pentagon procurement funds next-generation sensor integration and pod upgrades. The FY 2026 US procurement request of USD 205 billion prioritizes high-tech missiles and unmanned systems, expanding the targeting pods market pipeline. Canada's order for MQ-9B drones and the U.K.'s carrier-borne F-35B deployments reiterate ongoing sensor-upgrade cycles throughout allied fleets.

Asia-Pacific is the fastest-growing region at an 8.83% CAGR through 2031. Indonesia's deal for 42 Rafales, Singapore's combined F-16V and F-35B programs, and Japan's invitation to India to join the sixth-generation GCAP fighter underline regional momentum. Targeting pod demand benefits from broader defense-industrial cooperation and technology-transfer agreements that localize sustainment.

Europe maintains steady replacement demand driven by Tornado and older Typhoon retirement cycles. At the same time, Middle Eastern customers diversify their supplier bases to include South Korean and Turkish platforms equipped with advanced targeting capabilities. Latin America shows smaller but consistent retrofits, leveraging US Foreign Military Sales financing mechanisms that often bundle pod upgrades with aircraft maintenance packages. Collectively, regional demand curves affirm a resilient, globally distributed aircraft targeting pods market.

- ASELSAN A.S.

- Teledyne Technologies Incorporated

- Israel Aerospace Industries Ltd.

- L3Harris Technologies Inc.

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Rafael Advanced Defense Systems Ltd.

- RTX Corporation

- Thales Group

- BAE Systems plc

- Leonardo S.p.A

- Elbit Systems Ltd.

- Controp Precision Technologies Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing procurement of advanced combat aircraft in emerging economies

- 4.2.2 Upgrade programs for 4th/5th-generation aircraft fleets

- 4.2.3 Rising demand for precision-guided munitions

- 4.2.4 Increasing global defense budgets

- 4.2.5 Integration of AI-enabled sensor fusion within targeting pods

- 4.2.6 NATO push for networked multi-platform "kill-web" architecture

- 4.3 Market Restraints

- 4.3.1 High acquisition and life-cycle costs

- 4.3.2 Export-control/ITAR restrictions

- 4.3.3 Cooling-technology limits for SWaP-constrained UAV pods

- 4.3.4 Vulnerability to cyber and datalink jamming in contested A2AD zones

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform

- 5.1.1 Combat Aircraft

- 5.1.2 Unmanned Combat Aerial Systems (UCAS)

- 5.1.3 Attack Helicopters

- 5.1.4 Bombers

- 5.2 By Fit

- 5.2.1 Original Equipment Manufacturer (OEM)

- 5.2.2 Retrofit/Upgrade

- 5.3 By Pod Type

- 5.3.1 FLIR and Laser-Designator Pods

- 5.3.2 Laser Spot-Tracker Pods

- 5.3.3 Multispectral/Networked Pods

- 5.3.4 IRST-Integrated Pods

- 5.4 By Technology

- 5.4.1 Electro-Optical Imaging

- 5.4.2 Infrared Imaging

- 5.4.3 Multispectral/Hyperspectral Sensing

- 5.4.4 AI-Enabled Sensor Fusion

- 5.4.5 5G/Mesh Networking Enabled

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Israel

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ASELSAN A.S.

- 6.4.2 Teledyne Technologies Incorporated

- 6.4.3 Israel Aerospace Industries Ltd.

- 6.4.4 L3Harris Technologies Inc.

- 6.4.5 Lockheed Martin Corporation

- 6.4.6 Northrop Grumman Corporation

- 6.4.7 Rafael Advanced Defense Systems Ltd.

- 6.4.8 RTX Corporation

- 6.4.9 Thales Group

- 6.4.10 BAE Systems plc

- 6.4.11 Leonardo S.p.A

- 6.4.12 Elbit Systems Ltd.

- 6.4.13 Controp Precision Technologies Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment