PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061687

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061687

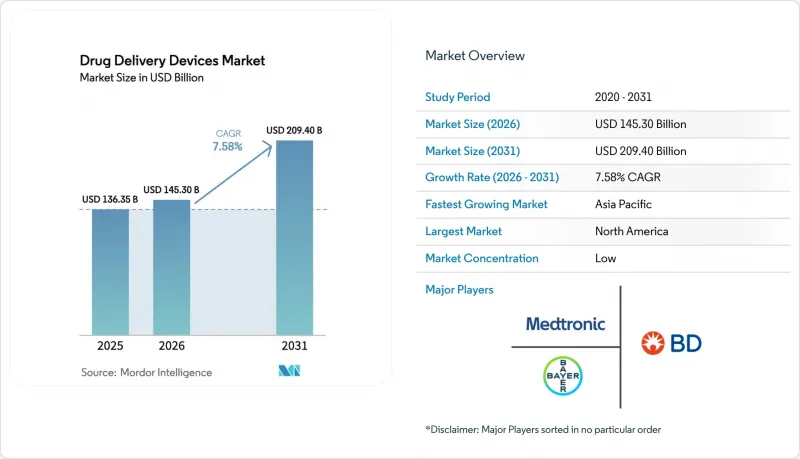

Drug Delivery Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the drug delivery devices market size was valued at USD 136.35 billion in 2025 and is estimated to grow from USD 145.30 billion in 2026 to reach USD 209.40 billion by 2031, at a CAGR of 7.58% during the forecast period (2026-2031).

This report is Segmented by Route of Administration (Oral, Injectable, Inhalation, Transdermal, Nasal, Ocular), Device Type (Prefilled Syringes, Auto-Injectors, Smart/Connected Devices, Inhalers & Nebulizers, and More), End User (Hospitals, and More), Therapeutic Area (Oncology, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Drug Delivery Devices Market Trends and Insights

Rising Chronic-Disease Burden Fueling Long-Term Therapeutics

Non-communicable diseases caused 74% of global deaths in 2024, and their economic burden surpassed USD 7 trillion each year. Diabetes prevalence reached 537 million adults in 2024 and will likely rise to 643 million by 2030, with rapid growth in low- and middle-income countries. Such epidemiology guides drug makers toward maintenance therapies that require frequent administration over decades, creating steady demand in the drug delivery devices market. Health systems already spend 90% of the United States' USD 3.8 trillion annual outlay on chronic-disease care, so payers support devices that cut emergency visits. As different disease clusters prefer distinct modalities, suppliers that offer diverse portfolios-prefilled syringes, transdermal patches, and implantable pumps-capture cross-indication opportunities.

Proliferation of Biologics & Biosimilars Needing Advanced Delivery

Biologics accounted for 30% of pharmaceutical sales in 2025 and are expanding roughly twice as fast as small molecules, propelled by oncology immunotherapies and monoclonal antibodies. Temperature sensitivity and aggregation risk elevate the role of prefilled syringes, autoinjectors, and pumps that assure dose accuracy. Biosimilars amplify device demand because regulators require comparable delivery systems to the originator, locking in device design and creating switching costs. Amgen demonstrates the downside of supply shocks; any syringe shortfall immediately erodes market share because alternative devices are not cross-approved. Device suppliers that can add hidden needles, lower injection force, or dose-confirmation cues gain formulary preference, widening opportunity in the drug delivery devices market.

Stringent Sterility & Regulatory Compliance Costs

Combination products face dual oversight, extending approval cycles and multiplying validation studies. Sterility assurance for prefilled syringes may consume up to 24 months and USD 5 million per line. Twenty-three FDA warning letters in 2024 highlighted sterility lapses, even among incumbents. The EU Medical Device Regulation, fully enforced in 2024, forces manufacturers to re-certify legacy products and has stretched launches by nine months. Smaller firms struggle to fund these processes, which consolidates the drug delivery devices market around multinationals with deep compliance teams.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Self-Administration & Home Healthcare Models

- Smart / Connected Devices Improving Adherence & Traceability

- High R&D and Manufacturing Capital Intensity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The shift toward patches broadens patient access to hormone therapy and vaccines, reflecting users' preference for painless administration. Inhalation remains essential for asthma and COPD, leveraging rapid pulmonary absorption and avoiding hepatically mediated degradation. Nasal delivery earned fresh awareness when the FDA cleared neffy epinephrine spray in 2024, introducing a needle-free anaphylaxis option.

Injectable routes dominate biologics and account for the bulk of cold-chain logistics. However, autoinjector adoption is cannibalizing vial-and-syringe formats because hidden needles and dose confirmation improve adherence. Ocular implants now reduce injection frequency for retinal diseases from monthly to semiannual, enhancing quality of life. Route selection has become a patient-centric exercise, rewarding device firms that validate real-world adherence benefits. As bioavailability data mature, the drug delivery devices market size linked to transdermal technologies is likely to expand further.

Payors value adherence evidence, justifying the 20-30% unit premium for connected autoinjectors. Prefilled syringes underpin biologic launches because they ease regulatory filings, although autoinjectors capture share where dose frequency is high. Transdermal patches benefit from microneedle innovation, while drug-eluting stents face competitive pressure from bioresorbable scaffolds with improved long-term outcomes.

Implantable pumps fill ultra-niche needs such as intrathecal baclofen, yet reimbursement remains favorable due to hospitalization savings. Needle-free jet injectors and on-body pumps occupy an "emerging" category and are advancing through pivotal trials. Device-type competition intensifies as pharmaceutical firms debate whether to build in-house capabilities or license turnkey platforms from specialists like SHL Medical. Vertical integration can protect intellectual property but magnifies regulatory exposure. Strategic choices here will recalibrate the drug delivery devices market size associated with each platform.

Geography Analysis

North America held 41.64% of global revenue in 2025, supported by premium pricing and Medicare policies that routinely expand coverage for connected devices. The FDA Breakthrough Devices Program also accelerates approvals, incentivizing early launches in the region. Canada benefits from U.S. spillover, while Mexican generics producers adopt advanced delivery systems to compete with imports. Growth is moderating as payers impose stricter cost-effectiveness thresholds, but the region remains the profit engine for the drug-delivery devices industry because unit prices are highest there.

Asia-Pacific is the fastest-growing region from 2026-2031, buoyed by China's localization push and India's biosimilar prowess. China approved 47 combination products in 2024 and offers tax credits for domestic production. Indian manufacturers collaborate with SHL Medical to develop pen injectors for emerging markets. Japan shifts toward value-based models that pay premiums for adherence data, creating pull for connected systems. Smaller economies such as South Korea and Australia serve as regulatory gateways to Southeast Asia, shortening go-to-market timelines.

Europe grows more slowly because reimbursement is fragmented and the Medical Device Regulation imposes heavy administrative loads. Germany, France, and the United Kingdom jointly contribute 60% of regional sales, with France's health technology assessment body now demanding real-world evidence before granting premium prices. ESG mandates foster early adoption of polymer syringes, which boosts suppliers that can demonstrate decarbonization. In the Middle East, Gulf Cooperation Council countries buy premium devices backed by oil revenue. Sub-Saharan Africa remains underpenetrated, although Ghana's microneedle vaccine pilots hint at leapfrog potential. South America is led by Brazil's public system, which squeezes margins, while Argentina's economic volatility stalls cold-chain investment. Regulatory harmonization across Mercosur could unlock scale, but timelines remain uncertain.

- Amgen

- Baxter

- Beckton Dickinson

- Eli Lilly and Company

- Enable Injections

- Gerresheimer

- Insulet

- Johnson & Johnson

- medmix AG

- Medtronic

- Nipro

- Novo Nordisk

- Pfizer

- SCHOTT

- SHL Medical

- Stevanato Group

- Teva Pharmaceutical Industries

- Terumo

- West Pharmaceutical Services

- Ypsomed

- Tandem Diabetes Care

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Chronic-Disease Burden Fueling Long-Term Therapeutics

- 4.2.2 Proliferation of Biologics & Biosimilars Needing Advanced Delivery

- 4.2.3 Shift Toward Self-Administration & Home Healthcare Models

- 4.2.4 Smart / Connected Devices Improving Adherence & Traceability

- 4.2.5 Microneedle Patch Rollouts for Mass Vaccination in LMICs

- 4.2.6 ESG-Driven Switch to Polymer & Bio-Based Syringes

- 4.3 Market Restraints

- 4.3.1 Stringent Sterility & Regulatory Compliance Costs

- 4.3.2 High R&D And Manufacturing Capital Intensity

- 4.3.3 Cyber-Security Recalls of Connected Infusion Systems

- 4.3.4 Specialty-Glass Supply Bottlenecks Disrupting Availability

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Route of Administration

- 5.1.1 Oral

- 5.1.2 Injectable

- 5.1.3 Inhalation

- 5.1.4 Transdermal

- 5.1.5 Nasal

- 5.1.6 Ocular

- 5.2 By Device Type

- 5.2.1 Prefilled Syringes

- 5.2.2 Auto-injectors

- 5.2.3 Smart / Connected Devices

- 5.2.4 Inhalers & Nebulizers

- 5.2.5 Transdermal Patches

- 5.2.6 Drug-eluting Stents

- 5.2.7 Implantable Pumps

- 5.2.8 Others

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgery Centers & Clinics

- 5.3.3 Home Healthcare Settings

- 5.3.4 Others

- 5.4 By Therapeutic Area

- 5.4.1 Oncology

- 5.4.2 Diabetes

- 5.4.3 Auto-immune Disorders

- 5.4.4 Cardiovascular Diseases

- 5.4.5 Infectious Diseases

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Amgen Inc.

- 6.3.2 Baxter International Inc.

- 6.3.3 Becton Dickinson & Company

- 6.3.4 Eli Lilly and Company

- 6.3.5 Enable Injections

- 6.3.6 Gerresheimer AG

- 6.3.7 Insulet Corporation

- 6.3.8 Johnson & Johnson

- 6.3.9 medmix AG

- 6.3.10 Medtronic plc

- 6.3.11 Nipro Corporation

- 6.3.12 Novo Nordisk A/S

- 6.3.13 Pfizer Inc.

- 6.3.14 SCHOTT AG

- 6.3.15 SHL Medical

- 6.3.16 Stevanato Group

- 6.3.17 Teva Pharmaceutical Industries

- 6.3.18 Terumo Corporation

- 6.3.19 West Pharmaceutical Services

- 6.3.20 Ypsomed Holding AG

- 6.3.21 Tandem Diabetes Care, Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment