PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061701

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061701

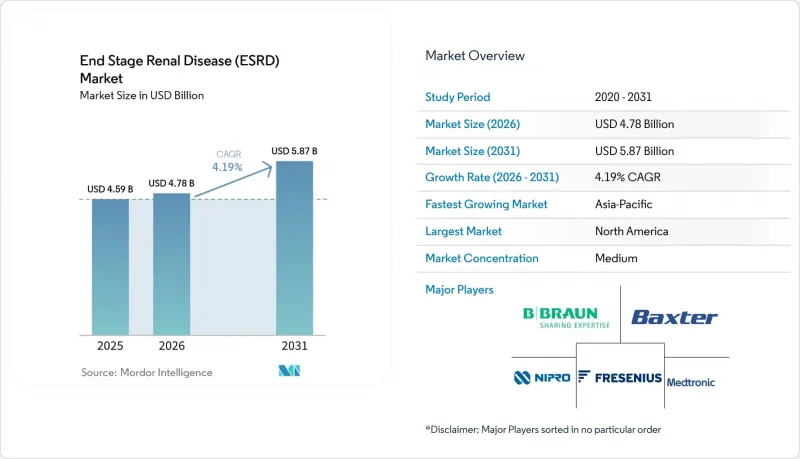

End Stage Renal Disease (ESRD) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the end stage renal disease (ESRD) market size is projected to expand from USD 4.59 billion in 2025 and USD 4.78 billion in 2026 to USD 5.87 billion by 2031, registering a CAGR of 4.19% between 2026 to 2031.

This report is Segmented by Treatment (Kidney Transplantation, Dialysis, and Conservative Kidney Management), Diagnosis (Blood Tests, Urine Tests, and More), End User ( Hospitals, Dialysis Centers, and More), Product Type (Hemodialysis Equipment, Dialysis Consumables, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global End Stage Renal Disease (ESRD) Market Trends and Insights

CKD Patient Pool Expansion Through Demographic and Lifestyle Convergence

The rising proportion of elderly citizens and the persistent spread of lifestyle diseases are enlarging the CKD base that ultimately progresses to end-stage renal disease, thereby broadening the ESRD market. Thirty-one percent of CKD cases remain undiagnosed in primary care, creating lost intervention opportunities and a USD 6.7 billion annual burden. Prevalence peaks at 50.94% in patients aged 90 years and older, while male incidence rates surpass female rates. AI-enabled biomarker panels and contrast-enhanced ultrasound tools are closing diagnostic gaps and paving the way for earlier treatment starts, which supports sustained growth in the ESRD market.

Rising Diabetes and Hypertension as Primary ESRD Catalysts

Diabetes and hypertension together underpin most ESRD admissions and are climbing fastest in urbanizing Asia-Pacific markets. Poorly controlled HbA1c levels accelerate CKD progression, necessitating earlier entry into the ESRD market. Medtronic's Symplicity Spyral renal denervation catheter obtained CMS transitional pass-through status in late 2024, highlighting how adjunct technologies for hypertension management are aligning with renal care pathways.

Late and Under-Diagnosis of CKD Limiting Market Potential

Systematic screening deficits keep a third of CKD patients undetected until advanced stages, delaying referral and raising emergency initiation rates. This late presentation curtails the volume of early-stage interventions that generate recurring revenue across the ESRD market, and it pushes up health-system costs due to higher morbidity.

Other drivers and restraints analyzed in the detailed report include:

- Government Infrastructure Investment Accelerating Access

- Technological Innovation in High-Flux and Wearable Hemodialysis

- Kidney Transplant Shortage Creating Systemic Treatment Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dialysis contributed 70.02% of revenue in the ESRD market during 2025, upholding its central role despite reimbursement pressures. Conservative Kidney Management is the rising alternative, expanding at a 8.88% CAGR on the strength of evidence showing comparable quality of life for frail elderly cohorts. Hemodialysis and peritoneal dialysis continue to split the modality mix, with PD gaining ground in countries that operate "PD First" policies.

Conservative care programs integrate symptom control, nutritional counseling, and palliative components, which align with patient-centred objectives and alleviate hospital utilization. Transplant uptake remains hindered by donor scarcity, although FDA-sanctioned xenotransplant trials could disrupt the treatment hierarchy in the long run. High-flux dialyzers and automated cyclers are broadening the technical capabilities underpinning modality choice and adding value layers within the ESRD market.

Blood Tests generated 45.10% of diagnostic revenue in 2025 as eGFR and creatinine remain the gateway markers for CKD staging. Imaging tools are advancing fastest at a 9.42% CAGR, fueled by AI platforms that reach 97.41% accuracy in kidney pathology identification, making them a powerful addition to the ESRD market toolbox.

Contrast-enhanced ultrasound and low-dose CT are detecting early structural changes before laboratory markers rise. Urine assays and emerging biomarker panels continue to play a complementary role. Integration of imaging outputs with electronic health records accelerates clinical workflow and supports risk-based patient stratification, reinforcing diagnostic ecosystem value creation.

Geography Analysis

North America represented 35.20% of global revenue in 2025, reflecting robust Medicare funding that covers 67% of dialysis spend. DaVita treated about 200,800 patients across 2,675 outpatient centers and facilitated 8,000 transplants in 2023, illustrating the scale advantages in place. CMS value-based purchasing is reshaping provider incentives and encouraging modality diversification, while staffing shortages accelerate adoption of automated technologies and tele-nephrology.

Asia-Pacific is the fastest-growing territory with a 9.02% CAGR through 2031, propelled by demographic aging, growing health coverage, and concerted government investment in dialysis infrastructure. Japan treats 334,505 dialysis patients and exports best-practice protocols to Southeast Asia, demonstrating knowledge diffusion that widens regional bandwidth. China faces a sizable CKD burden and deploys blended reimbursement to spur therapy uptake, reinforcing expansion prospects for the ESRD market.

Europe, the Middle East and Africa, and South America present heterogeneous growth profiles. European markets benefit from universal reimbursement and established clinic networks yet confront capacity strains from aging populations. The ISN Global Kidney Health Atlas highlights that only 32% of patients in low-income countries within MEA can access dialysis despite technical availability, exposing a financing gap. South America is developing coverage models that stretch public budgets but still sees treatment costs exceed per capita income in many nations, making low-cost devices and micro-insurance important adoption drivers.

- Fresenius

- Baxter

- Nipro

- B. Braun

- Medtronic

- Asahi Kasei

- Nikkiso Co. Ltd.

- Beckton Dickinson

- STERIS plc (Cantel)

- Toray Medical Co. Ltd.

- Terumo

- DaVita

- Diaverum AB

- Satellite Healthcare

- U.S. Renal Care

- Rockwell Medical

- AWAK Technologies

- Outset Medical

- Quanta Dialysis Technologies

- Biocon Ltd. (Immunosuppressants)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 CKD Patient Pool Expansion (Aging & Lifestyle)

- 4.2.2 Rising Diabetes & Hypertension Prevalence

- 4.2.3 Government Funding For Dialysis Infrastructure

- 4.2.4 Technological Advances - High-Flux & Wearable HD

- 4.2.5 Growth In Home-Based Dialysis Reimbursement

- 4.2.6 Artificial Kidney & Xenotransplant R&D Momentum

- 4.3 Market Restraints

- 4.3.1 Late/Under-Diagnosis Of CKD

- 4.3.2 Shortage Of Donor Kidneys & Transplant Backlog

- 4.3.3 High Treatment Cost Burden In Lmics

- 4.3.4 Dialysis Clinic Staffing Shortages

- 4.4 Porter's Five Forces

- 4.4.1 Bargaining Power of Buyers/Consumers

- 4.4.2 Bargaining Power of Suppliers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Treatment

- 5.1.1 Kidney Transplantation

- 5.1.2 Dialysis

- 5.1.2.1 Hemodialysis

- 5.1.2.2 Peritoneal Dialysis

- 5.1.3 Conservative Kidney Management

- 5.2 By Diagnosis

- 5.2.1 Blood Tests (eGFR, Creatinine)

- 5.2.2 Urine Tests (ACR, protein)

- 5.2.3 Imaging (Ultrasound, CT/MRI)

- 5.2.4 Other Diagnostics

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Dialysis Centers

- 5.3.3 Home-care Settings

- 5.4 By Product Type

- 5.4.1 Hemodialysis Equipment

- 5.4.2 Dialysis Consumables (Dialyzers, AV sets)

- 5.4.3 Peritoneal Dialysis Solutions & Sets

- 5.4.4 Transplant Immunosuppressants

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Fresenius SE & Co. KGaA

- 6.3.2 Baxter International Inc.

- 6.3.3 Nipro Corporation

- 6.3.4 B. Braun SE

- 6.3.5 Medtronic plc

- 6.3.6 Asahi Kasei Medical Co. Ltd.

- 6.3.7 Nikkiso Co. Ltd.

- 6.3.8 Becton, Dickinson & Company

- 6.3.9 STERIS plc (Cantel)

- 6.3.10 Toray Medical Co. Ltd.

- 6.3.11 Terumo BCT

- 6.3.12 DaVita Inc.

- 6.3.13 Diaverum AB

- 6.3.14 Satellite Healthcare

- 6.3.15 U.S. Renal Care

- 6.3.16 Rockwell Medical

- 6.3.17 AWAK Technologies

- 6.3.18 Outset Medical

- 6.3.19 Quanta Dialysis Technologies

- 6.3.20 Biocon Ltd. (Immunosuppressants)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment