PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061712

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061712

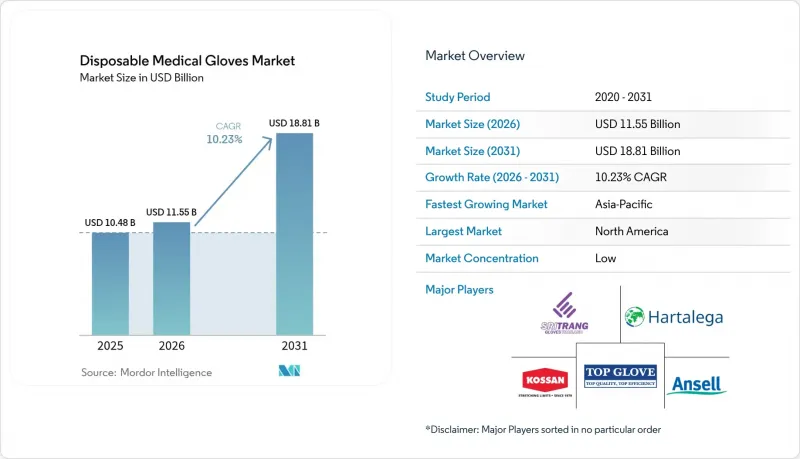

Disposable Medical Gloves - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the disposable medical gloves market size was valued at USD 10.48 billion in 2025 and estimated to grow from USD 11.55 billion in 2026 to reach USD 18.81 billion by 2031, at a CAGR of 10.23% during the forecast period (2026-2031).

This report is Segmented by Application (Surgical, Examination, Chemotherapy, and Clean-Room), Material (Nitrile, Latex, and More), Form (Powder-Free and Powdered), Sterility (Sterile and Non-Sterile), End-User (Hospitals, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Global Disposable Medical Gloves Market Trends and Insights

Stricter Global Infection-Control Standards Across Healthcare Facilities

Healthcare systems are tightening glove usage protocols, moving from generic examination gloves to highly task-specific variants. According to updated American Red Crossguidelines released in November 2024, first-aid responders must don medical examination gloves for every patient interaction, a recommendation now echoed in many national protocols. Intensive-care audits under Australia's 2024 safety frameworkshow average consumption of 30 pairs per patient per 12-hour shift, underscoring how protocols translate into volume. The shift obliges procurement teams to diversify SKUs, and that complexity spurs hospitals to adopt inventory-management software that flags impending stock-outs in real time.

Rising Surgical & Diagnostic Procedure Volumes Driven by Aging & Chronic-Disease Burden

Procedure growth remains a pillar of the Disposable Medical Gloves market expansion. Medicare data indicate 56 new ambulatory surgical centers certified in one recent quarter, illustrating how outpatient capacity absorbs rising surgical demand from the 65+ age cohort. Journal of Medicine, Surgery, and Public Health projections show patients over 65 could account for 39% of all U.S. surgeries by 2034, translating directly into higher sterile-glove pull-through. A similar demographic trend in Europe, where the senior population could approach 30% by mid-century, suggests that procedure-linked glove volumes will stay elevated even if per-procedure glove counts stabilize.

Volatility in Natural Rubber & Nitrile-Butadiene Feedstock Prices

Flooding in Thailand nudged natural latex prices higher in late 2024, forcing smaller glove makers to renegotiate supply contracts on shorter cycles. At the same time, a weakening USD versus Asian currencies narrowed export margins, prompting leading Malaysian producers to discuss average selling-price increases toward USD 21-22 per 1,000 pieces for Q4 2024. Acrylonitrile prices eased, giving nitrile-focused manufacturers brief margin relief, yet petrochemical volatility remains a planning headache. The pattern incentivizes vertical integration into raw-material streams and fuels R&D into alternative elastomers that display less commodity price sensitivity.

Other drivers and restraints analyzed in the detailed report include:

- Industry-Wide Shift to Synthetic (Nitrile/Neoprene) Gloves for Allergy Compliance

- Expansion of Healthcare Infrastructure & Insurance Coverage in Emerging Economies

- Intensifying Environmental & Sustainability Regulations on Single-Use Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Examination gloves hold a 57.70% market share in the Disposable Medical Gloves market in 2025, reflecting their universal role across clinical and non-clinical settings. Hospitals report that standard examination SKUs account for nearly three-quarters of monthly glove lines on purchase orders, illustrating entrenched baseline demand. A growing share now features chemo-tested nitrile to satisfy broader formularies, subtly blending categories and lifting average selling prices. That shift suggests incremental revenue upside even within a mature subsegment.

Chemotherapy gloves post the fastest forecast expansion at 11.15% CAGR through 2031, propelled by oncology service growth and ASTM D6978 breakthrough-time requirements. Contract wins in large U.S. cancer networks show that suppliers offering full chemo-drug permeation panels secure multi-year agreements. Surgical gloves, growing at a significant percentage, benefit from rising procedure counts, while clean-room gloves gain from semiconductor fab expansions that impose stricter contamination thresholds. The specialized nature of these uses makes regulatory compliance a practical barrier that protects pricing power for qualified producers.

Nitrile commands 53.10% Disposable Medical Gloves market share and remains the mainstream choice due to hypoallergenic properties and chemical resistance. Purchasing databases indicate that nitrile volume surged nearly fivefold from 2010 to 2024, suggesting that the material shift is durable. Increased line-speed automation brings average unit cost down, enabling nitrile producers to defend share against lower-priced vinyl in cost-sensitive accounts. Stable nitrile demand, paired with moderate feedstock relief, underpins supplier cash flows for further capacity upgrades.

Neoprene exhibits the highest growth at 11.98% CAGR, mainly because its latex-like comfort eases clinician transition from legacy materials. Premium dental and surgical users note that neoprene's elasticity reduces hand-fatigue complaints during long procedures, subtly influencing brand loyalty. Latex keeps a shrinking but sizeable foothold in regions where allergy policies are less stringent, while vinyl (PVC) and polyethylene serve budget-constrained or non-critical tasks. Sustainability considerations are steering R&D toward biodegradable nitrile blends that meet both performance and environmental criteria, indicating likely portfolio rebalancing in the next product-cycle.

Geography Analysis

North America leads with a 33.85% Disposable Medical Gloves market share, supported by high per-capita healthcare spending and rigorous infection-control regulations. The Centers for Medicare & Medicaid Services' proposal to adjust payments for domestically manufactured PPE narrows the cost disadvantage of U.S.-made gloves by approximately USD 0.13 per unit. That policy momentum spurs existing producers to expand capacity in states such as Texas and Alabama, and early evidence shows shorter lead times influencing hospital sourcing choices. The region also exhibits strong adoption of task-specific glove protocols, contributing to SKU proliferation within hospital formularies.

Asia Pacific's 11.05% CAGR rests on healthcare infrastructure expansion, rising insurance coverage, and thriving medical tourism. Malaysian plants incorporate Industry 4.0 robotics to raise line speeds above 45,000 pieces per hour, cushioning wage inflation. Trade policy shifts, especially higher U.S. duties on Chinese gloves, benefit Southeast Asian exporters through order diversion. India's government investment in 157 new medical colleges accelerates demand for examination and surgical gloves, and localized warehousing in Tier-2 cities reduces last-mile costs for distributors.

Europe sustains a notable share, underpinned by stringent environmental directives that elevate demand for eco-friendly glove alternatives. National health systems are piloting procurement frameworks that weigh carbon footprint alongside price, nudging suppliers toward biodegradable nitrile. The Middle East and Africa show rising penetration as governments invest in tertiary hospitals and universal health coverage schemes. In South America, Brazil leads adoption, and state purchase programs increasingly include training on correct glove disposal, an element contributing to broader infection-prevention capacity building.

- Ansell

- Cardinal Health

- Dynarex Corp.

- Hartalega Holdings Bhd

- Kimberly-Clark Corp.

- Kossan Rubber Industries

- Molnlycke Health Care

- Rubberex Bhd

- Semperit

- Supermax Corp. Bhd

- Top Glove Corp. Bhd

- American Nitrile LLC

- Sri Trang Gloves PLC

- Medline Industries

- Intco Medical Technology

- Mercator Medical SA

- Careplus Group Bhd

- Showa Group

- Winner Medical Co. Ltd.

- Zhonghong Pulin Medical

- Smart Glove Corp.

- Eagle Protect PBC

- Shield Scientific BV

- Adenna LLC

- Honeywell International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter Global Infection-Control Standards Across Healthcare Facilities

- 4.2.2 Rising Surgical & Diagnostic Procedure Volumes Driven by Aging & Chronic-Disease Burden

- 4.2.3 Industry-Wide Shift to Synthetic (Nitrile/Neoprene) Gloves for Allergy Compliance

- 4.2.4 Expansion of Healthcare Infrastructure & Insurance Coverage in Emerging Economies

- 4.2.5 Process & Automation Advances Delivering High-Volume, Low-Cost Production

- 4.2.6 E-procurement Platforms Enabling Bulk Ordering by Small Clinics in Emerging Markets

- 4.3 Market Restraints

- 4.3.1 Volatility in Natural Rubber & Nitrile-Butadiene Feed-stock Prices

- 4.3.2 Intensifying Environmental & Sustainability Regulations on Single-Use Plastics

- 4.3.3 Global Overcapacity Post-Pandemic Triggering Persistent Price Competition

- 4.3.4 U.S. Withhold-Release Orders (WRO) on Labor Practices Creating Import Uncertainty

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Application

- 5.1.1 Surgical

- 5.1.2 Examination

- 5.1.3 Chemotherapy

- 5.1.4 Clean-Room

- 5.2 By Material

- 5.2.1 Nitrile (NBR)

- 5.2.2 Latex (Natural Rubber)

- 5.2.3 Vinyl (PVC)

- 5.2.4 Neoprene (Polychloroprene)

- 5.2.5 Polyethylene (CPE/TPE)

- 5.3 By Form

- 5.3.1 Powder-Free

- 5.3.2 Powdered

- 5.4 By Sterility

- 5.4.1 Sterile

- 5.4.2 Non-Sterile

- 5.5 By End-User

- 5.5.1 Hospitals

- 5.5.2 Diagnostic Laboratories

- 5.5.3 Ambulatory Surgical Centers

- 5.5.4 Dental Clinics

- 5.5.5 Home-Care Settings

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Ansell Ltd.

- 6.3.2 Cardinal Health Inc.

- 6.3.3 Dynarex Corp.

- 6.3.4 Hartalega Holdings Bhd

- 6.3.5 Kimberly-Clark Corp.

- 6.3.6 Kossan Rubber Industries Bhd

- 6.3.7 Molnlycke Health Care AB

- 6.3.8 Rubberex Bhd

- 6.3.9 Semperit AG Holding

- 6.3.10 Supermax Corp. Bhd

- 6.3.11 Top Glove Corp. Bhd

- 6.3.12 American Nitrile LLC

- 6.3.13 Sri Trang Gloves PLC

- 6.3.14 Medline Industries LP

- 6.3.15 Intco Medical Technology

- 6.3.16 Mercator Medical SA

- 6.3.17 Careplus Group Bhd

- 6.3.18 Showa Group

- 6.3.19 Winner Medical Co. Ltd.

- 6.3.20 Zhonghong Pulin Medical

- 6.3.21 Smart Glove Corp.

- 6.3.22 Eagle Protect PBC

- 6.3.23 Shield Scientific BV

- 6.3.24 Adenna LLC

- 6.3.25 Honeywell International Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment