PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061725

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061725

Tall Oil Fatty Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

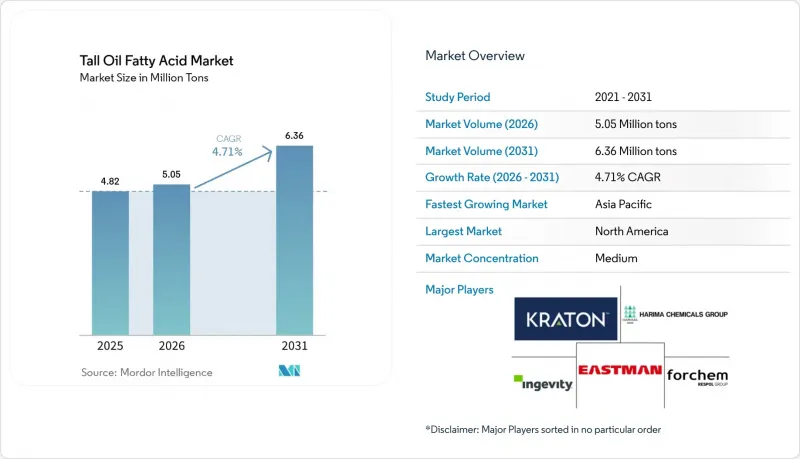

According to Mordor Intelligence, the tall oil fatty acid market size is projected to be 4.82 Million tons in 2025, 5.05 Million tons in 2026, and reach 6.36 Million tons by 2031, growing at a CAGR of 4.71% from 2026 to 2031.

This report is Segmented by Product Type (Oleic Acid, Linoleic Acid, Linolenic Acid, Palmitic Acid, and Other Product Types), Application (Alkyd Resins, Dimer Acids, Fatty Acid Esters, and Other Applications), End-User Industry (Soaps and Detergents, Paints and Coatings, and More), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Global Tall Oil Fatty Acid Market Trends and Insights

Escalating Demand for Bio-based Lubricants

Original equipment manufacturers in automotive and industrial equipment are switching to bio-based lubricants that satisfy stringent eco-label criteria. Tall Oil Fatty Acid market participants position TOFA esters as drop-in basestocks that offer high lubricity, rapid biodegradation, and reliable low-temperature flow. Elevated CTO costs temporarily prompted formulators to revert to vegetable fatty acids in 2023, but multi-year supply contracts have since stabilized pricing. New demand pockets include electric-vehicle thermal fluids and wind-turbine gearbox oils, both of which need high-purity, hydrogenated grades. Producers are upgrading hydrotreating and fractionation units to meet oxidative-stability targets. As OEM sustainability targets tighten, volume commitments for certified, traceable TOFA are growing across Europe and the United States.

Expanding Alkyd-Resin Consumption in Architectural Coatings

Architectural coatings dominate the consumption of alkyd resins, leveraging their binders for enhanced leveling, gloss retention, and a cost-effective solids content. Certification schemes like LEED and BREEAM incentivize paints with renewable carbon content, and notably, TOFA-based alkyds boast a bio-based carbon content. The Asia-Pacific region, propelled by urban housing initiatives in India and China, witnesses growth in its coatings segment. While acrylic and polyurethane dispersions are gaining traction in premium exterior coatings, hybrid alkyd-acrylic systems are rapidly bridging the performance divide. Producers collaborating with coating companies to co-develop these hybrids stand to secure lucrative long-term offtake agreements. As a result, the Tall Oil Fatty Acid market is shifting focus towards these value-added binder applications, moving away from its traditional commodity esters.

Dependence on Softwood Kraft-Pulping Capacity

Global output of softwood kraft pulp limits the availability of Tall Oil Fatty Acid (TOFA). Since 2020, a shift in digital media and packaging towards hardwood fibers has resulted in the closure of several mills across North America. Meanwhile, as renewable diesel expansions eye a larger share of CTO, competition intensifies between chemical producers and fuel customers. The TOFA market faces a persistent feedstock challenge, especially in the absence of new softwood mills emerging in South America or Southeast Asia.

Other drivers and restraints analyzed in the detailed report include:

- Rising Use of TOFA-based Dimer Acids in Adhesives and Oil-field Chemicals

- Government Incentives for Low-Carbon Feedstocks

- Stricter Forestry Regulations on Logging

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oleic Acid held 42.74% of volume in 2025, the largest slice of Tall Oil Fatty Acid market share, while Linolenic Acid is projected to register the fastest 5.92% CAGR through 2031. Oleic Acid's C18:1 profile underpins metalworking fluids, surfactants, and alkyd resins. Its esters with glycerol and polyols fortify emulsifiers across personal-care and agrochemical formulations, keeping demand stable even amid feedstock fluctuations. Linolenic Acid, rich in triple unsaturation, enables rapid oxidative crosslinking, making it valuable in high-performance coatings and adhesive polyamides. Automotive lightweighting and wind-turbine blade production require such adhesives for fatigue resistance, explaining the segment's momentum.

Growth in Linolenic Acid also reflects refiners' move toward high-margin specialties. Investments in nitrogen-blanketed storage and antioxidant packages mitigate its oxidation sensitivity, supporting longer supply chains. Palmitic and other saturated acids fulfill soap, rubber, and fragrance niches but lack the reactivity to capture dynamic demand. SunPine's diversification into a-Pinene and Kraton's focus on yield optimization illustrate how Tall Oil Fatty Acid market participants are upgrading product slates to offset commodity price volatility.

Geography Analysis

North America contributed 35.38% of the 2025 volume, led by Southeastern United States kraft-pulp mills that supply integrated refineries. Renewable diesel mandates have escalated CTO bidding wars, lifting prices substantially between 2022 and 2023. Ingevity's divestment of its North Charleston refinery removed integrated capacity, while Kraton's tower upgrade aims to claw back regional share. Canada exports CTO to U.S. refiners, and Mexico's demand sits mostly in detergents.

Asia-Pacific is forecast to post a 7.51% CAGR through 2031, bolstered by China's bio-materials roadmap and India's construction boom, which multiplies coatings demand. Russia-to-China timber curbs raised costs for Chinese TOFA buyers, redirecting procurement to Nordic and U.S. mills. Japan and South Korea stabilize regional demand through automotive lubricants, whereas Indonesia and Vietnam add kraft capacity, albeit mostly hardwood.

Europe benefits from Sweden and Finland's integrated kraft complexes that feed CTO to both chemical and biofuel plants. RED III double-counting sustains refinery order books even after SunPine's revenue dip, while UPM's Leuna project highlights the capital intensity of backward integration. France's CTO blend cap and Germany's phase-out of double counting introduce cross-border arbitrage, nudging Tall Oil Fatty Acid market participants to route cargoes toward more favorable jurisdictions.

- Ataman Kimya

- Eastman Chemical Company

- Fintoil Hamina Oy

- Forchem Oyj

- Foreverest Resources Ltd.

- Georgia-Pacific Chemicals

- Harima Chemicals Group, Inc.

- Ilim Group

- Imperial Industrial Minerals Company

- Ingevity

- Kraton Corporation

- Lascaray S.A.

- Pasand Speciality Chemicals

- Pine Chemical Group

- Segezha Group

- SunPine AB

- Univar SolutionsLLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating demand for bio-based lubricants

- 4.2.2 Expanding alkyd-resin consumption in architectural coatings

- 4.2.3 Rising use of TOFA-based dimer acids in adhesives and oil-field chemicals

- 4.2.4 Government incentives for low-carbon feedstocks

- 4.2.5 Regional CTO-refinery closures driving price premiums and new capacity

- 4.3 Market Restraints

- 4.3.1 Dependence on softwood kraft-pulping capacity

- 4.3.2 Stricter forestry regulations on logging

- 4.3.3 Competition from lower-cost vegetable-oil fatty acids

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Product Type

- 5.1.1 Oleic Acid

- 5.1.2 Linoleic Acid

- 5.1.3 Linolenic Acid

- 5.1.4 Palmitic Acid

- 5.1.5 Other Product Types (Stearic Acid, etc.)

- 5.2 By Application

- 5.2.1 Alkyd Resins

- 5.2.2 Dimer Acids

- 5.2.3 Fatty Acid Esters

- 5.2.4 Other Applications (Lubricant Additives, etc.)

- 5.3 By End-user Industry

- 5.3.1 Soaps and Detergents

- 5.3.2 Paints and Coatings

- 5.3.3 Automotive

- 5.3.4 Metalworking Fluids

- 5.3.5 Oil and Gas

- 5.3.6 Other End User Industries (Adhesives and Sealants, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Ataman Kimya

- 6.4.2 Eastman Chemical Company

- 6.4.3 Fintoil Hamina Oy

- 6.4.4 Forchem Oyj

- 6.4.5 Foreverest Resources Ltd.

- 6.4.6 Georgia-Pacific Chemicals

- 6.4.7 Harima Chemicals Group, Inc.

- 6.4.8 Ilim Group

- 6.4.9 Imperial Industrial Minerals Company

- 6.4.10 Ingevity

- 6.4.11 Kraton Corporation

- 6.4.12 Lascaray S.A.

- 6.4.13 Pasand Speciality Chemicals

- 6.4.14 Pine Chemical Group

- 6.4.15 Segezha Group

- 6.4.16 SunPine AB

- 6.4.17 Univar SolutionsLLC

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment