PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061736

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061736

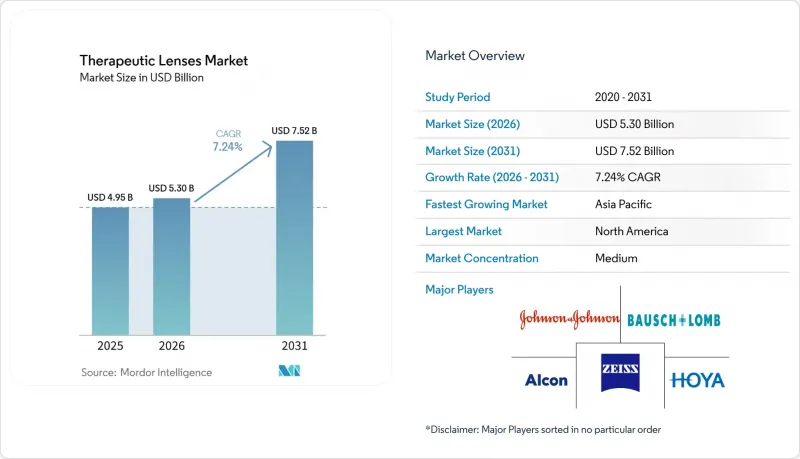

Therapeutic Lenses - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the therapeutic lenses market size is projected to be USD 4.95 billion in 2025, USD 5.30 billion in 2026, and reach USD 7.52 billion by 2031, growing at a CAGR of 7.24% from 2026 to 2031.

This report is Segmented by Lens Type (Bandage Contact Lenses, Drug-Eluting Lenses, Scleral Lenses, and More), Material (Hydrogel, Silicone Hydrogel, and More), Indication (Corneal Ulcer & Injury, Dry-Eye Syndrome, and More), Design (Daily Disposable, Extended Wear, Customized), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Therapeutic Lenses Market Trends and Insights

Rising Myopia Prevalence Among Young Adults

Global myopia climbed from 24.32% in 1990 to 35.81% in 2023, with forecasts placing childhood prevalence at 39.80% by 2050. East Asia reports secondary-school rates exceeding 70%, compelling governments to adopt nationwide screening initiatives that funnel young patients toward dual-focus therapeutic soft lenses. Six-year clinical data show a 71% deceleration in eye growth when these lenses replace conventional correction, extending average wear cycles and deepening recurring-revenue pools for manufacturers. Education-driven near-work habits and limited outdoor exposure ensure the demand curve remains steep, cementing myopia control as the prime catalyst for the therapeutic lens market.

Rapid Adoption of Silicone-Hydrogel Materials

Fourth-generation silicone hydrogels reach 107 Dk/t oxygen transmission, enabling overnight therapy without hypoxia-related complications. Integrated wetting agents curb protein deposition, while embedded vitamin E barriers extend drug release to 30 days, a fifteen-fold improvement versus legacy hydrogels. Global majors are patenting novel macromers that marry permeability with robust drug-loading matrices, ensuring that silicone-based lenses stay at the forefront of therapeutic innovation. Silicone hydrogels advanced from 2.8% of global fits in 2000 to 73.7% by 2023, driven by Dk values above 100 that mitigate hypoxia and enable overnight wear. Surface-energy constraints have been largely solved by plasma oxidation and polyethylene glycol coatings, while embedded silver nanoparticles are now achieving a two-log reduction in Pseudomonas counts during 30-day soak tests.

High Risk of Microbial Keratitis

Therapeutic-lens users experience infection incidents at 52 per 10,000 patient-years, triple the rate of conventional wearers, owing to compromised corneal surfaces and extended use times. Emerging antibiotic resistance among Pseudomonas and Serratia strains intensifies clinical vigilance and elevates regulatory documentation burdens. While antimicrobial coatings and single-use regimens curb incidence, prescribers remain cautious, limiting uptake in high-risk cohorts until long-term surveillance data confirm safety parity with daily disposables.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Insurance Reimbursement for Ocular-Surface Disease

- Surge in Drug-Eluting Lens Clinical Trials

- Price Sensitivity in Emerging Economies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bandage contact lenses accounted for 37.12% of the therapeutic lens market share in 2025, reflecting their role as first-line corneal dressings that also serve as drug-soaked reservoirs for localized therapy. Scleral lenses post the fastest 8.92% CAGR to 2031 because their fluid reservoir supports glaucoma and dry-eye drug delivery while correcting complex refractive errors. Drug-eluting designs are at the forefront of innovation, embedding controlled-release mechanisms that extend therapeutic exposure beyond conventional dosing windows. Soft therapeutic lenses retain steady demand for routine corneal protection and comfort, whereas rigid gas-permeable options address irregular corneas that need precise optical alignment.

The lens-type evolution highlights the convergence of vision correction and pharmacologic delivery, as nanoparticle carriers and molecular imprinting unlock programmable release profiles. Scleral growth benefits from their ability to maintain a stable drug reservoir over the ocular surface, improving bioavailability and patient comfort compared with eye drops. Bandage lens leadership endures because clinicians trust their established protocols for acute corneal protection, postoperative healing, and pain relief. Collectively, these dynamics ensure that each lens type occupies a distinct therapeutic niche within the growing lens market.

Silicone hydrogels supplied 43.12% of 2025 sales, underpinned by unmatched permeability metrics that satisfy overnight therapy safety thresholds. Nevertheless, fluoro-silicone acrylates are expanding at a 9.55% CAGR, combining fluorinated surface energy with silicone channels to elevate wettability while retaining oxygen flow. Traditional hydrogels find niches where higher water content facilitates hydrophilic drug diffusion, though lower Dk/t values limit extended-wear labeling. Material engineers are balancing modulus, water content, and surface chemistry to deliver lenses that maintain mechanical integrity during high drug-load cycles.

Competitive pipelines yield elastomeric silicone variants that embed biosensors without sacrificing optical clarity. As the therapeutic lens market matures, multi-material hybrids with a silicone core and a hydrogel surface may emerge to tailor release kinetics, posing fresh intellectual property opportunities.

Geography Analysis

North America accounted for the highest 42.23% share of the therapeutic lens market in 2024, driven by integrated payer systems and the rapid uptake of drug-device innovations. Regional manufacturers enjoy mature distribution networks and strong optometrist adoption, which underpin premium pricing. Cross-border e-commerce, tele-optometry, and rising myopia-control awareness continue to drive upgrades in volume and mix.

Asia-Pacific remains the fastest-growing region, with a 11.93% CAGR, driven by unprecedented myopia prevalence of 70-90% among urban Chinese teenagers and improving disposable incomes. Governments invest in school-based screening, while private hospitals partner with international brands, e.g., Menicon's 2025 MOU with Dr. Agarwals Eye Hospital to scale myopia-control clinics. Domestic lens makers in China and Korea are challenging incumbents with price-competitive drug-eluting prototypes, accelerating market democratization.

Latin America and the Middle East & Africa post mid-single-digit growth, tempered by limited insurance coverage and price sensitivity. Nonetheless, local distributors report rising adoption of professional lenses in private urban clinics, signaling untapped upside once macro conditions improve. Multinational companies have begun establishing regional finishing labs to circumvent import tariffs and currency volatility, sharpening competitiveness.

Across all regions, the therapeutic lens market benefits from telehealth traction that shortens access gaps; yet regulatory disparities, taxation, and variable sterilization standards require tailored market-entry tactics. Harmonization efforts such as the ASEAN Medical Device Directive promise to streamline approvals, further quickening APAC expansion.

- Alcon

- Art Optical Contact Lens Inc.

- Bausch + Lomb Corp.

- CooperVision Inc.

- Euclid Systems Corp.

- Hoya Corp.

- Johnson & Johnson Vision Care

- Mark'ennovy Personalized Care

- Menicon Co. Ltd.

- Paragon Vision Sciences

- Seed Co. Ltd.

- SynergEyes

- Visioneering Technologies Inc.

- X-Cel Specialty Contacts

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Myopia Prevalence Among Young Adults

- 4.2.2 Rapid Adoption of Silicone-Hydrogel Materials

- 4.2.3 Expanding Insurance Reimbursement for Ocular-Surface Disease

- 4.2.4 Surge in Drug-Eluting Lens Clinical Trials

- 4.2.5 AI-Guided Custom Lens-Fitting Platforms

- 4.2.6 Military R&D for Medicated Field Lenses

- 4.3 Market Restraints

- 4.3.1 High Risk of Microbial Keratitis

- 4.3.2 Price Sensitivity in Emerging Economies

- 4.3.3 Supply-Chain Fragility of Pharma-Grade Silicones

- 4.3.4 Regulatory Uncertainty Around Sustained-Release Devices

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Bargaining Power of Buyers

- 4.7.5 Threat of Substitutes

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Lens Type

- 5.1.1 Bandage Contact Lenses

- 5.1.2 Drug-Eluting Lenses

- 5.1.3 Scleral Lenses

- 5.1.4 Soft Therapeutic Lenses

- 5.1.5 Rigid Gas-Permeable (RGP) Therapeutic Lenses

- 5.2 By Material

- 5.2.1 Hydrogel

- 5.2.2 Silicone Hydrogel

- 5.2.3 Fluoro-Silicone Acrylate

- 5.2.4 PMMA & Others

- 5.3 By Indication

- 5.3.1 Corneal Ulcer & Injury

- 5.3.2 Dry-Eye Syndrome

- 5.3.3 Post-Surgical Healing

- 5.3.4 Glaucoma Drug Delivery

- 5.3.5 Allergic & Inflammatory Conditions

- 5.4 By Design

- 5.4.1 Daily Disposable

- 5.4.2 Extended Wear

- 5.4.3 Customized (Wavefront-Guided, Orthokeratology)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Alcon Inc.

- 6.3.2 Art Optical Contact Lens Inc.

- 6.3.3 Bausch + Lomb Corp.

- 6.3.4 CooperVision Inc.

- 6.3.5 Euclid Systems Corp.

- 6.3.6 Hoya Corp.

- 6.3.7 Johnson & Johnson Vision Care

- 6.3.8 Mark'ennovy Personalized Care

- 6.3.9 Menicon Co. Ltd.

- 6.3.10 Paragon Vision Sciences

- 6.3.11 Seed Co. Ltd.

- 6.3.12 SynergEyes Inc.

- 6.3.13 Visioneering Technologies Inc.

- 6.3.14 X-Cel Specialty Contacts

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment