PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061740

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061740

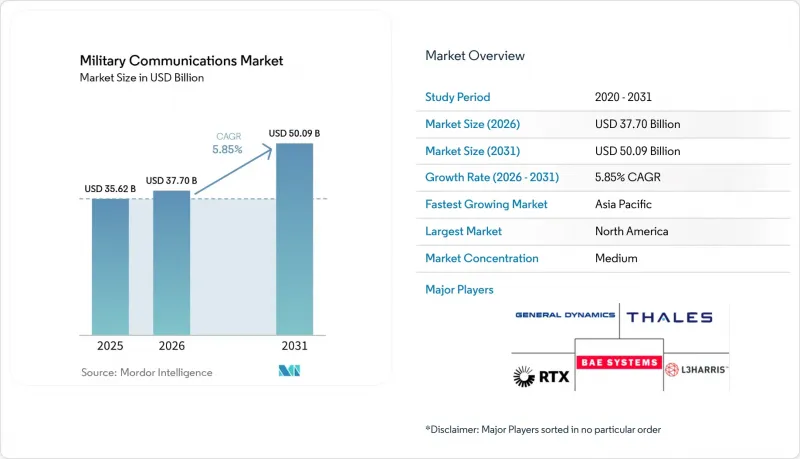

Military Communications - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, military communications market size in 2026 is estimated at USD 37.7 billion, growing from 2025 value of USD 35.62 billion with 2031 projections showing USD 50.09 billion, growing at 5.85% CAGR over 2026-2031.

This report is Segmented by Communication Type (Shipborne, Ground-Based, and More), Component (Military SATCOM Systems, Military Radio Systems, and More), Application (Command and Control, Intelligence Surveillance and Reconnaissance, and More), Platform (Land Forces, Naval Forces, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Military Communications Market Trends and Insights

DoD Joint All-Domain Command and Control (JADC2) Roll-outs

The USD 13.8 billion JADC2 initiative transforms force structure by merging sensor data from ground, air, space, and cyber sources into a single operational picture. Real-time fusion raises the bar on throughput, latency, and security, forcing suppliers to deliver software-defined terminals that support multiple simultaneous waveforms and rapid over-the-air updates. L3Harris and Palantir field demonstrations show that leveraging existing sensors with AI analytics can shorten decision loops without adding congestive data channels. As open-architecture standards spread among allies, the military communications market gains momentum from procurement reforms that favor interoperability and lifecycle cost savings.

Proliferation of Low-Earth-Orbit Defense Constellations

Hundreds of small satellites in LEO reduce latency and extend path diversity, keeping links alive when single nodes face kinetic or cyber attacks. The US Space Force's plan to launch more than 100 satellites in 2025 sets the tone for other nations. Multi-band user terminals must hand off between satellites every few minutes, driving demand for adaptive antennas and beam-steering modules. Cloud-based mission-control software coordinates traffic, balancing classified and commercial channels on the fly. Suppliers can certify these mixed links and secure long-run service contracts. As resilient space layers mature, armed forces view proliferated architectures as baseline rather than niche.

Congested and Contested Spectrum Causing Interoperability Bottlenecks

Civil 5G, mega-constellations, and adversary jammers crowd bands once reserved for defense, forcing coalition forces to deconflict frequencies in real time. NATO standards lag behind the pace of waveform proliferation, causing mission-critical handoffs to stall when incompatible radios meet on joint operations. Vendors must embed spectrum-sense functions and cross-band gateways, yet these add cost and complexity that dampen near-term adoption.

Other drivers and restraints analyzed in the detailed report include:

- Demand Spike for Jam-Resilient SATCOM on the Move

- AI-Enabled Radio Resource Management in Contested Spectrum

- Cost Over-runs in Multi-Domain Integration Programs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Underwater communications recorded the highest 9.12% CAGR outlook as navies close gaps in covert maritime connectivity. Though still holding 35.78% of the military communications market share in 2025, ground-based nodes evolve into mesh architectures that reroute automatically under fire. Armored vehicle radio upgrades and brigade-level 5G nodes anchored the military communications market size for ground systems. Acoustic modems and laser-based blue-green links enable submarines to share situational awareness without surfacing, a capability spotlighted by the AUKUS innovation challenge. Shipborne platforms adopt multi-band SATCOM and L-band antennas to maintain links during high-sea-state maneuvers. Air-ground interoperability improves through AN/PRC-158 installations on CH-47 Chinook helicopters, linking rotary fleets directly into tactical IP networks.

Advances in low-probability-detection waveforms boost airborne adoption despite stringent size and power constraints. As spectrum becomes contested, aircraft radios integrate adaptive coding and directional antennas to minimize emissions. Meanwhile, coastal HF stations provide fallback paths if satellites or cellular links are denied, cementing hybrid resilience across the military communications market.

Military radio systems accounted for 30.22% of the military communications market size in 2025. Still, cybersecurity subsystems posted the fastest 8.02% CAGR as encryption, zero-trust access, and endpoint detection merged with transport hardware. Smartphone-style rugged devices under the US Army's Next Generation Command and Control program introduce intuitive user interfaces while leveraging SDR cores for waveform agility. Integrated antenna apertures cover UHF through Ka-band with one panel, shrinking mast footprints and accelerating vehicle-mount retrofits.

Across fixed sites, photonic links and hardened fiber replace copper for high data volumes and reduced electromagnetic leakage. Tactical data links such as Link-16 and MADL migrate to IP overlays, easing interface with cloud applications. As proliferated LEO traffic surges, multiband RF front ends learn to arbitrate between GEO and LEO assets, maximizing uptime inside the military communications market.

Geography Analysis

North America retained 41.11% of the military communications market share in 2025, driven by the Pentagon's JADC2 and a USD 8.6 billion 2025 budget line for communications and electronics. Defense primes headquartered in the region house vertically integrated design, manufacturing, and sustainment streams, accelerating speed-to-field. Canada advances Arctic SATCOM and HF gateways that join NORAD networks, while Mexico procures secure border-monitoring radios. The region's leadership in AI-enabled spectrum tools and private 5G architectures cements its status as a global technology hub in the military communications market.

Asia-Pacific posts the highest 6.45% CAGR through 2031. China and India's channel budget rises into indigenous software-defined radio programs to cut reliance on foreign encryption chips. Taiwan's NTD 7.81 billion (USD 238.44 million) Field Information Communications System illustrates regional appetite for resilient, interoperable backbones amid rising Strait tensions. Japan and South Korea fund underwater and space-relay projects to secure supply lanes, while Australia's AUKUS partnership spurs acoustic submarine links that plug directly into US tactical IP nets. These multi-layer investments solidify Asia-Pacific as the second growth pillar of the military communications market.

Europe benefits from NATO interoperability mandates and elevated defense budgets after the Ukraine conflict. Germany's EUR 3.2 billion (USD 3.7 billion) digital transformation and the Netherlands' USD 1.42 billion AN/PRC radio order exemplify momentum toward standardized, coalition-ready radios. The UK continues to overhaul land-force networks under Morpheus despite delays. Nordic states prioritize Arctic outreach, trialing high-latitude L-band satellites and HF fallback mesh. Southern European nations focus on maritime SATCOM to monitor critical sea lanes. Collectively, Europe sustains mid-single-digit growth within the military communications market.

- BAE Systems plc

- Northrop Grumman Corporation

- RTX Corporation

- General Dynamics Corporation

- Lockheed Martin Corporation

- L3Harris Technologies, Inc.

- Thales Group

- Leonardo S.p.A.

- Elbit Systems Ltd.

- Israel Aerospace Industries Ltd.

- ASELSAN A.S.

- Viasat Inc.

- Rohde & Schwarz USA, Inc.

- Saab AB

- Airbus SE

- Curtiss-Wright Corporation

- Frequentis AG

- Honeywell International Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 DoD "Joint All-Domain Command and Control" roll-outs

- 4.2.2 Proliferation of low-earth-orbit (LEO) defense constellations

- 4.2.3 Demand spike for jam-resilient SATCOM on the Move (SOTM)

- 4.2.4 AI-enabled radio resource management in contested spectrum

- 4.2.5 Private 5G/6G tactical mesh networks for brigade-level autonomy

- 4.2.6 Increased Arctic and Indo-Pacific deployments requiring beyond-line-of-sight (BLOS) links

- 4.3 Market Restraints

- 4.3.1 Congested and contested spectrum causing interoperability bottlenecks

- 4.3.2 Cost over-runs in multi-domain integration programs

- 4.3.3 Export-control limits on crypto-grade components

- 4.3.4 Reliance on legacy waveforms delaying software-defined upgrades

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Communication Type

- 5.1.1 Shipborne

- 5.1.2 Ground-based

- 5.1.3 Underwater

- 5.1.4 Air to Ground

- 5.1.5 Airborne

- 5.2 By Component

- 5.2.1 Military SATCOM Systems

- 5.2.2 Military Radio Systems

- 5.2.3 Military Security/Cyber Systems

- 5.2.4 Tactical Data-Links

- 5.2.5 Integrated Antenna and RF Front-Ends

- 5.2.6 Fiber-optic and Photonic Links

- 5.3 By Application

- 5.3.1 Command and Control (C2/C3)

- 5.3.2 Intelligence, Surveillance, and Reconnaissance (ISR)

- 5.3.3 Routine Operations and Logistics

- 5.3.4 Electronic Warfare (EW) Support

- 5.3.5 Humanitarian and Disaster Relief

- 5.4 By Platform

- 5.4.1 Land Forces

- 5.4.2 Naval Forces

- 5.4.3 Air Forces

- 5.4.4 Space Forces

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 Israel

- 5.5.5.1.3 United Arab Emirates

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 Egypt

- 5.5.5.2.2 South Africa

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BAE Systems plc

- 6.4.2 Northrop Grumman Corporation

- 6.4.3 RTX Corporation

- 6.4.4 General Dynamics Corporation

- 6.4.5 Lockheed Martin Corporation

- 6.4.6 L3Harris Technologies, Inc.

- 6.4.7 Thales Group

- 6.4.8 Leonardo S.p.A.

- 6.4.9 Elbit Systems Ltd.

- 6.4.10 Israel Aerospace Industries Ltd.

- 6.4.11 ASELSAN A.S.

- 6.4.12 Viasat Inc.

- 6.4.13 Rohde & Schwarz USA, Inc.

- 6.4.14 Saab AB

- 6.4.15 Airbus SE

- 6.4.16 Curtiss-Wright Corporation

- 6.4.17 Frequentis AG

- 6.4.18 Honeywell International Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment