PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061745

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061745

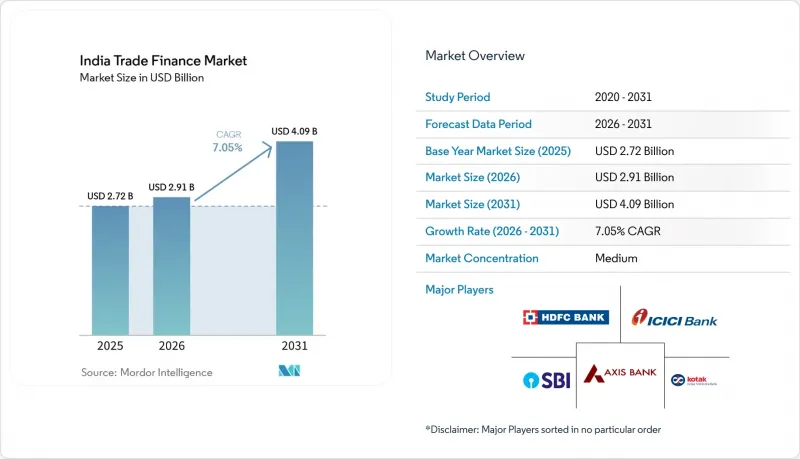

India Trade Finance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the india trade finance market size was valued at USD 2.72 billion in 2025 and estimated to grow from USD 2.91 billion in 2026 to reach USD 4.09 billion by 2031, at a CAGR of 7.05% during the forecast period (2026-2031).

This report is Segmented by Product (Documentary, Non-Documentary), by Service Provider (Banks, Trade Finance Companies, Insurance Companies, and More), by Application (Domestic, International), by Company Size (Large Enterprises, Small and Medium-Sized Enterprises), and by Financing Structure (Structured Trade Finance, Non-Structured Trade Finance). The Market Forecasts are Provided in Terms of Value (USD).

India Trade Finance Market Trends and Insights

Government Export-Push Programs Create Sector-Specific Credit Concentration

PLI outlays-in electronics (INR 41,000 crore), pharmaceuticals (INR 15,000 crore), and automotive components (INR 25,938 crore)-tie working-capital disbursements to export milestones, letting banks price facilities on compliance metrics rather than standalone balance-sheet ratios. FTAs such as the India-UAE pact that lifted bilateral trade to USD 65 billion in 2023 and aims at USD 100 billion by 2030 amplify sudden pre-export funding spikes. Lenders have formed PLI-only desks and built dashboards that track order fulfilment against drawdowns, improving risk visibility and reducing per-transaction costs.

Rapid E-Invoicing and TReDS Adoption Transform Working-Capital Access

Businesses with turnover above INR 5 crore must now issue electronic invoices, creating a standardized data lake for real-time credit scoring. TReDS platforms-RXIL, M1xchange, and A.TREDS-have financed invoices worth more than INR 270 billion, shrinking cash-conversion cycles from 45 days to under a week on average. Dynamic pricing based on buyer credit quality replaces legacy models that priced against seller financials, giving smaller vendors cheaper funding and freeing large buyers to extend payment terms without hurting suppliers' liquidity.

Rising NPA Concerns Constrain Bank Credit Expansion

Unsecured consumer credit now makes up 51.9% of new NPAs, leading regulators to hike risk weights on unsecured portfolios. Although trade-finance defaults remain lower, supply-chain contagion risk elevates caution. Banks require higher collateral margins and shorter tenors, nudging borrowers toward NBFCs that price risk more aggressively but at higher spreads.

Other drivers and restraints analyzed in the detailed report include:

- MSME Working-Capital Gap Creates Sustainable Growth Opportunity

- GIFT City Liberalization Attracts International Trade-Finance Flows

- Complex Multi-Layer Compliance Creates Operational Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

At 58.45% share in 2025, non-documentary receivables finance anchors the India trade finance market and is racing ahead at an 8.31% CAGR. Factoring, forfaiting, and supply-chain finance thrive because standardized e-invoice data shorten risk assessment from days to minutes. Documentary letters of credit retain relevance for bulk commodities, but their growth lags as corporates embrace lower-cost open-account solutions. Payables finance gains traction among large buyers targeting double-digit improvements in cash flow, while guarantees and insurance remain crucial in sectors such as defense, infrastructure, and agro-commodities. Blockchain pilots now embed smart contracts that release funds on verified delivery, trimming fraud risk and supporting higher funding limits.

Banks captured 76.05% of the India trade finance market in 2025 through universal licences that package FX, cash management, and trade credit. Yet alternative platforms are expected to grow at a 10.14% CAGR by serving tickets under USD 25,000, where traditional cost structures are prohibitive. TReDS operators earn auction fees instead of spread, improving economics for thin-margin invoices. Trade-credit insurers like ECGC cover up to 90% of export losses, lengthening credit tenors to 180-360 days. Fintechs plug balance-sheet limits through co-lending; for instance, Axis Bank funds 80% of an approved line, while a partner NBFC carries first-loss risk.

List of Companies Covered in this Report:

- State Bank of India (SBI)

- HDFC Bank

- ICICI Bank

- Axis Bank

- Kotak Mahindra Bank

- Yes Bank

- Bank of Baroda

- Punjab National Bank

- Standard Chartered

- HSBC

- Citi Bank

- IndusInd Bank

- Federal Bank

- EXIM Bank of India

- IDFC First Bank

- Tata Capital Financial Services

- Aditya Birla Finance

- M1xchange (TReDS)

- RXIL (TReDS)

- Credlix

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Govt export-push programmes (PLI, FTAs)

- 4.2.2 Rapid e-Invoicing & TReDS adoption

- 4.2.3 MSME working-capital gap widens

- 4.2.4 GIFT-City/IFSC liberalisation

- 4.2.5 Fintech platforms attracting offshore capital

- 4.2.6 ESG-linked trade-finance mandates

- 4.3 Market Restraints

- 4.3.1 Rising NPA / counter-party-risk concerns

- 4.3.2 Complex multi-layer compliance (KYC/AML)

- 4.3.3 USD liquidity & forex-swap volatility

- 4.3.4 Low SME awareness of factoring/TReDS

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Documentary

- 5.1.1.1 Letter of Credit

- 5.1.1.2 Other Documentary Collections

- 5.1.2 Non-Documentary

- 5.1.2.1 Receivables Finance (Factoring, Forfaiting, Invoice Discounting)

- 5.1.2.2 Payables/Supply Chain Finance (Reverse Factoring, Dynamic Discounting)

- 5.1.2.3 Direct Lending/Open Account-Based Finance (Trade Loans, Buyer's/Seller's Credit)

- 5.1.2.4 Guarantees (Performance, Bid, Financial Guarantees)

- 5.1.2.5 Insurance Products (Trade Credit Insurance, PRI, ECA Cover)

- 5.1.1 Documentary

- 5.2 By Service Provider

- 5.2.1 Banks

- 5.2.2 Trade Finance Companies

- 5.2.3 Insurance Companies

- 5.2.4 Other Service Providers

- 5.3 By Application

- 5.3.1 Domestic

- 5.3.2 International

- 5.4 By Company Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-sized Enterprises (SMEs)

- 5.5 By Financing Structure

- 5.5.1 Structured Trade Finance

- 5.5.2 Non-Structured Trade Finance

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 State Bank of India (SBI)

- 6.4.2 HDFC Bank

- 6.4.3 ICICI Bank

- 6.4.4 Axis Bank

- 6.4.5 Kotak Mahindra Bank

- 6.4.6 Yes Bank

- 6.4.7 Bank of Baroda

- 6.4.8 Punjab National Bank

- 6.4.9 Standard Chartered

- 6.4.10 HSBC

- 6.4.11 Citi Bank

- 6.4.12 IndusInd Bank

- 6.4.13 Federal Bank

- 6.4.14 EXIM Bank of India

- 6.4.15 IDFC First Bank

- 6.4.16 Tata Capital Financial Services

- 6.4.17 Aditya Birla Finance

- 6.4.18 M1xchange (TReDS)

- 6.4.19 RXIL (TReDS)

- 6.4.20 Credlix

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment