PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061808

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061808

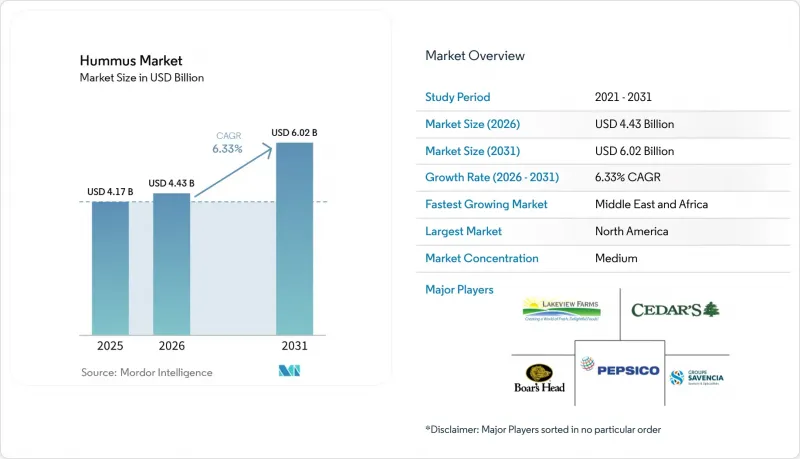

Hummus - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the hummus market size is expected to grow from USD 4.17 billion in 2025 to USD 4.43 billion in 2026 and is forecast to reach USD 6.02 billion by 2031 at 6.33% CAGR over 2026-2031.

This report is Segmented by Category (Chickpea-Based Hummus, Alternative Base Hummus), Flavor Type (Roasted Garlic, Red Pepper, Black Olive, and More), Packaging Type (Cups/Tubs/Jars, Bottles, Pouches, Others), Distribution Channel (On-Trade and Off-Trade), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Hummus Market Trends and Insights

Increasing consumer preference for plant-based and vegan foods

The increasing consumer preference for plant-based and vegan foods is a key driver of the hummus market, as these diets align closely with the product's natural, protein-rich, and plant-based profile. According to the Good Food Institute 2024 report, around 60% of U.S. households purchased some type of plant-based food, indicating a significant shift toward plant-forward eating habits. In Europe, the trend is similarly strong, with the ProVeg International 2024 report noting that approximately 27% of Europeans identify as flexitarians, while nearly 40% of consumers in Germany follow a flexitarian diet, making it one of the largest plant-based consumer markets in the region. This growing adoption of plant-forward and vegan diets is driving demand for convenient, nutritious, and versatile products like hummus, which can serve as a healthy snack, spread, or dip. Manufacturers are responding by expanding product lines, offering innovative flavors, and emphasizing clean-label and natural ingredients. The rise in plant-based awareness is particularly influencing retail, online, and foodservice channels, further boosting hummus consumption

Rising awareness of health benefits of chickpeas, such as high protein and fiber content

The rising awareness of the health benefits of chickpeas, particularly their high protein and fiber content, is a key driver of the hummus market. Chickpeas provide 19-25% protein, 12-17% fiber, and essential micronutrients such as iron, zinc, and folate, making hummus a nutrient-dense, plant-based snack that aligns well with dietary guidelines emphasizing legume consumption. Despite these benefits, European dietary guidelines across 11 countries recommend 1-3 servings of legumes per week, yet studies from 2023-2024 indicate that only 37% of European adults meet these targets, highlighting a gap between recommendations and actual intake. This gap underscores significant untapped market potential, especially if consumer education and convenience barriers are addressed. As awareness grows, more health-conscious consumers are turning to hummus as an easy, tasty way to increase legume intake, particularly in snacks, spreads, and meal accompaniments, further strengthening the hummus market.

Raw material price volatility and supply shortages

Raw material price volatility and supply shortages pose a significant restraint on the hummus market, affecting both production costs and profit margins. Chickpeas, the primary ingredient in hummus, are subject to fluctuations in global agricultural output due to weather variability, crop diseases, and changing cultivation patterns. Sudden increases in chickpea prices or disruptions in supply chains can lead to higher manufacturing costs, which may be passed on to consumers, potentially affecting demand. Additionally, reliance on imported chickpeas in key markets like North America and Europe makes manufacturers vulnerable to trade restrictions, transportation delays, and geopolitical factors. Limited availability of other key ingredients, such as tahini and olive oil, can further compound supply challenges. These factors create operational uncertainties for both large-scale producers and smaller regional brands, impacting production planning and inventory management.

Other drivers and restraints analyzed in the detailed report include:

- Rising global ethnic cuisine interest, leading to new product launches and flavor innovation

- Rising adoption of Mediterranean diet trends across Europe and North America

- Product adulteration and recalls

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The chickpea-based hummus segment dominated the hummus market in 2025, capturing 85.01% of the total share, reflecting its status as the traditional and most widely consumed variant. Chickpeas are a rich source of protein, fiber, and essential nutrients, which enhances the nutritional appeal of hummus and drives consumer preference. This segment benefits from strong familiarity among consumers across North America, Europe, and the Middle East, where chickpea-based hummus has long been a staple in diets. Its versatility in sandwiches, dips, spreads, and snack recipes further supports consistent demand. In addition, the growing trend of plant-based and protein-rich diets has reinforced chickpea hummus's popularity among health-conscious consumers. Manufacturers continue to innovate within this segment by introducing flavored and fortified varieties, expanding product offerings while maintaining its dominant market position.

In contrast, the alternative-base hummus segment is expected to register the fastest growth, with a projected CAGR of 7.89% through 2031, driven by increasing consumer interest in diverse plant-based ingredients. These variants use ingredients such as lentils, beans, peas, or vegetables as primary bases, catering to those seeking gluten-free, allergen-friendly, or novel flavor profiles. Rising awareness of dietary restrictions and clean-label preferences is encouraging experimentation with non-traditional bases, creating opportunities for product differentiation. Innovative formulations, such as beetroot, pumpkin, or black bean hummus, are attracting younger consumers and the flexitarian population. Additionally, the growth of specialty retail channels and online marketplaces has made alternative-base products more accessible to a wider audience.

The original hummus segment dominated the global hummus market in 2025, accounting for 38.11% of total revenue, reflecting its widespread popularity and status as the classic variant. Consumers prefer the original profile for its authentic taste, smooth texture, and versatility as a dip, spread, or accompaniment in meals. Its strong presence in both retail and foodservice channels has reinforced steady demand, particularly in regions with established hummus consumption such as North America, Europe, and the Middle East. The original flavor also serves as a base for recipe experimentation, allowing manufacturers to introduce new variants and meal pairings while maintaining consumer trust. Health-conscious and plant-based consumers further favor this variant for its natural ingredients and protein-rich content.

Conversely, black-olive flavored hummus is projected to be the fastest-growing segment, expanding at a CAGR of 8.03% through 2031, driven by increasing consumer interest in gourmet and bold flavors. This variant appeals to adventurous and premium-focused consumers seeking novel taste experiences and Mediterranean-inspired profiles. Its growth is supported by rising demand in foodservice outlets, specialty stores, and online retail platforms, where flavor diversity is highly valued. Black-olive hummus also benefits from the trend of incorporating functional ingredients, as olives are associated with antioxidants and heart-healthy properties. Manufacturers are expanding their flavor portfolio to include black-olive and other Mediterranean-inspired variants to capture this emerging demand.

Geography Analysis

North America held a commanding 38.45% share of the global hummus market in 2025, driven by strong consumer acceptance of ready-to-eat and plant-based products. The region benefits from high awareness of health and wellness trends, with hummus being popular as a protein-rich, low-calorie snack. Supermarkets, hypermarkets, and online grocery platforms dominate distribution, providing convenient access to a wide variety of flavors and packaging formats. Innovation in flavored hummus, portion-controlled packs, and clean-label products has further strengthened demand in the hummus market. Additionally, the rising popularity of Mediterranean and Middle Eastern cuisine has made hummus a staple in many households. North America's well-established retail and foodservice infrastructure supports consistent growth and maintains its position as the largest regional market.

The Middle East and Africa region is projected to grow at the fastest pace, with a CAGR of 8.47% between 2026 and 2031, reflecting both cultural affinity and rising consumer demand. Hummus is traditionally popular in many Middle Eastern countries, and expanding urbanization, modern retail development, and international food trends are driving growth. The rise of convenience-oriented lifestyles and the adoption of packaged and ready-to-eat variants are further boosting sales across the hummus market. Foodservice channels, including restaurants, cafes, and catering services, are increasingly offering hummus as part of appetizers and meal accompaniments. Additionally, product innovation, including flavored and gourmet variants, is attracting younger consumers.

Other regions, including Asia-Pacific, Europe, and South America, are experiencing steady growth, though at a relatively moderate pace. In Europe, demand is supported by rising health-conscious eating habits, plant-based diets, and clean-label trends, particularly in Western countries. Asia-Pacific is witnessing growing adoption in urban centers, supporting expansion of the hummus market through increasing awareness of international cuisines and the expansion of retail and e-commerce channels. South America is gradually adopting hummus in foodservice and retail, driven by rising interest in protein-rich snacks and plant-based alternatives.

- Pepsico, Inc. (Sabra Dipping Company)

- Lakeview Farms (Tribe Hummus)

- Cedar's Mediterranean Foods Inc.

- Boar's Head Brand Provision Co., Inc.

- Groupe Savencia

- Hope Foods LLC

- Bakkavor Group Plc

- Strauss Group Ltd

- Lantana Foods

- Haliburton International Foods Inc

- Obela

- Deldiche N.V.

- MeToo! Foods

- Lazy Foods

- Labeyrie Fine Foods

- Belies

- Orexis Fresh Foods Ltd

- Ithaca Hummus

- Hummus Goodness

- Roots Hummus

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing consumer preference for plant-based and vegan foods

- 4.2.2 Rising awareness of health benefits of chickpeas, such as high protein and fiber content

- 4.2.3 Rising global ethnic cuisine interest, leading to new product launches and flavor innovation

- 4.2.4 Rising adoption of Mediterranean diet trends across Europe and North America

- 4.2.5 Growth in fast-casual and QSR outlets offering hummus-based products

- 4.2.6 Demand for clean-label and preservative-free hummus

- 4.3 Market Restraints

- 4.3.1 Raw material price volatility and supply shortages

- 4.3.2 Product adulteration and recalls

- 4.3.3 Competition from alternative dips and spreads

- 4.3.4 Limited consumer awareness in emerging markets

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Category

- 5.1.1 Chickpea- Based Hummus

- 5.1.2 Alternative Base Hummus

- 5.2 By Flavor Type

- 5.2.1 Roasted Garlic

- 5.2.2 Red Pepper

- 5.2.3 Black Olive

- 5.2.4 Original Hummus

- 5.2.5 Others

- 5.3 By Packaging Type

- 5.3.1 Cups/Tubs/Jars

- 5.3.2 Bottles

- 5.3.3 Pouches

- 5.3.4 Others

- 5.4 By Distribution Channel

- 5.4.1 On-trade

- 5.4.2 Off-trade

- 5.4.2.1 Supermarkets/Hypermarkets

- 5.4.2.2 Convenience/Grocery Stores

- 5.4.2.3 Online Retail Stores

- 5.4.2.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Pepsico, Inc. (Sabra Dipping Company)

- 6.4.2 Lakeview Farms (Tribe Hummus)

- 6.4.3 Cedar's Mediterranean Foods Inc.

- 6.4.4 Boar's Head Brand Provision Co., Inc.

- 6.4.5 Groupe Savencia

- 6.4.6 Hope Foods LLC

- 6.4.7 Bakkavor Group Plc

- 6.4.8 Strauss Group Ltd

- 6.4.9 Lantana Foods

- 6.4.10 Haliburton International Foods Inc

- 6.4.11 Obela

- 6.4.12 Deldiche N.V.

- 6.4.13 MeToo! Foods

- 6.4.14 Lazy Foods

- 6.4.15 Labeyrie Fine Foods

- 6.4.16 Belies

- 6.4.17 Orexis Fresh Foods Ltd

- 6.4.18 Ithaca Hummus

- 6.4.19 Hummus Goodness

- 6.4.20 Roots Hummus

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK