PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061813

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061813

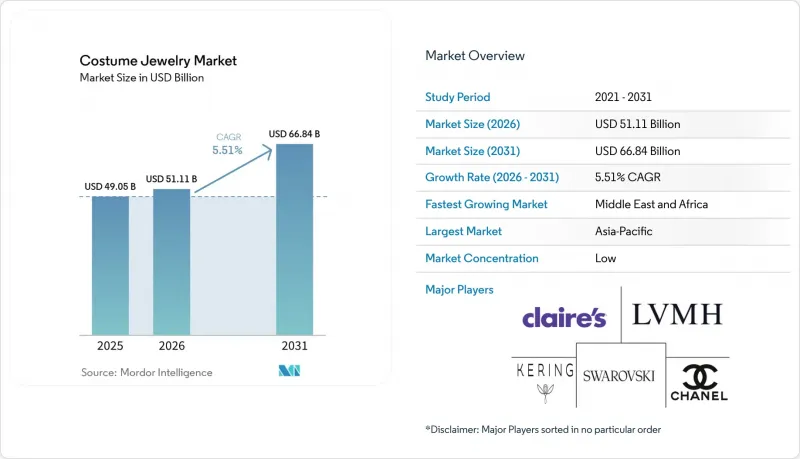

Costume Jewelry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the costume jewelry market was valued at USD 49.05 billion in 2025, reached USD 51.11 billion in 2026, and is projected to grow to USD 66.84 billion by 2031, registering a compound annual growth rate (CAGR) of 5.51% during the forecast period.

This report is Segmented by Product Type (Rings, Necklace and Chains, and More), Material (Metal-Based, Plastics and Acrylics, Glass and Crystal, and Others), End User (Women, Men, and Unisex), Distribution Channel (Offline Retail Stores, and Online Retail Stores), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Costume Jewelry Market Trends and Insights

Affordability compared to fine jewelry

Price-conscious consumers view costume jewelry as a way to manage economic uncertainty, directing discretionary spending toward items that provide aesthetic appeal without the financial commitment of precious metals. This approach aligns with the economics of fast-fashion apparel, where unit costs under USD 50 encourage trend experimentation without significant financial concern. Costume jewelry offers consumers the flexibility to stay updated with changing trends without the long-term financial implications associated with fine jewelry. The use of lab-grown diamonds and recycled metals further narrows the price difference with fine jewelry, enabling costume jewelry brands to deliver gemstone-like aesthetics at a lower cost. These materials not only reduce production costs but also address growing consumer demand for sustainable and ethically sourced products. This aligns with the preferences of 78% of U.S. consumers who prioritize ethical sourcing in their purchasing decisions, reflecting a broader shift toward responsible consumption.

Fast fashion and trend-driven consumption

Fast fashion and trend-driven consumption serve as key structural drivers of the global costume jewelry market by shortening fashion cycles and accelerating the rate at which consumers update their personal style. As apparel brands quickly replicate runway and social media trends, consumers increasingly seek complementary accessories to complete their outfits, positioning costume jewelry as an affordable and essential component of fast fashion wardrobes. The rapid spread of trends through platforms such as TikTok and Instagram further reduces the time between trend emergence and mass adoption, promoting frequent, impulse-driven purchases over occasional buying. Industry data indicates that fast fashion brands frequently launch new collections, heavily relying on trend replication and rapid production cycles. This creates a consumption environment where novelty and immediacy dominate purchasing behavior. Consequently, demand becomes highly responsive to trend cycles, with purchase decisions driven more by aesthetics, influencer culture, and social validation than by durability or intrinsic value, supporting sustained volume growth in the costume jewelry market.

Volatile base-metal commodity prices squeezing margins

Base-metal commodity price fluctuations create a significant constraint for the global costume jewelry market, as metals like brass, copper, steel, and nickel remain fundamental in manufacturing affordable pieces. Supply chain disruptions, stemming from geopolitical tensions, mining operations, and tariff changes, generate cost increases, reducing manufacturer and retailer margins. According to the World Bank, in November 2024, the average monthly price for copper reached over USD 9,000 per metric ton, increasing from USD 8,000 per metric ton in November 2023, impacting production costs for manufacturers using copper-based alloys in their designs . These market conditions require manufacturers to implement cost management strategies: absorbing material expenses, adjusting consumer prices, or selecting alternative materials. Fast-fashion jewelry retailers like Claire's and H&M, which maintain low-margin operations, experience direct profit impacts from price variations. Cost increases affect supply agreements and production schedules, limiting market responsiveness. As a result, base-metal price risk management has become a strategic requirement, with companies implementing hedging strategies and material diversification to maintain operational stability in the market.

Other drivers and restraints analyzed in the detailed report include:

- Rising influence of social media and fashion influencers

- Adoption of short-run 3-D printing enabling mass-customized pieces

- Proliferation of inexpensive counterfeits diluting brand equity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Necklaces and chains accounted for 42.34% of the revenue in 2025, highlighting their versatility and suitability as gifts. The rings sub-category is expected to grow at a CAGR of 5.59%, contributing to the expansion of the fashion jewelry market size between 2026 and 2031. Stackable ring sets are particularly popular among younger consumers due to their layering flexibility. Earrings continue to be everyday essentials, while chains and pendants benefit from layering trends influenced by styling videos from social media influencers. Additionally, smart-sensor modules integrated into pendants demonstrate the merging of accessories with wearable technology, creating new value opportunities.

Transformable jewelry pieces, such as those that can shift from chokers to double-wrap bracelets, cater to consumer demand for multifunctionality and further expand the fashion jewelry market. Additive printing supports niche product launches, allowing designers to experiment with innovative shapes without the need for costly molds. Gender-neutral chains with geometric links appeal to a broad demographic, reinforcing inclusivity themes. Limited-edition releases tied to pop-culture events create a sense of scarcity, driving full-price sales and supporting profit margins.

Metal-based jewelry held the largest market share in the global costume jewelry market, accounting for 35.18% of total revenue in 2025. This demand is driven by consumer preferences for durability and long-term value retention. Companies are expanding their product portfolios by combining traditional metals with modern designs to enhance market penetration across various customer segments. Manufacturers are adopting advanced plating technologies and hypoallergenic finishes to improve product quality and user experience. Additionally, the segment is experiencing growth through strategic collaborations with fashion designers and influencers, aimed at maintaining market presence and increasing consumer engagement.

The glass and crystal jewelry segment is projected to grow at a CAGR of 5.81% through 2031, supported by advancements in facet-cutting technologies that mimic the properties of natural gemstones. Swarovski's synthetic-diamond revenue doubled in 2024, reflecting growing market acceptance of alternative materials in core product lines. Companies like H&M and Zara are utilizing plastic, acrylic, and resin materials to streamline production cycles, while brands such as Wolf Circus and SOKO are incorporating recycled wood, textile composites, and bio-based PLA polymers. These material innovations are expanding manufacturing capabilities while addressing the rising demand for sustainable and differentiated jewelry products.

Geography Analysis

Asia-Pacific maintained its leadership in the costume jewelry market, accounting for 36.40% of global revenue in 2025. This dominance is driven by China's well-established supplier infrastructure and India's growing middle-income consumer base, which support cost-effective production and market adaptability. Additionally, Japan's manufacturing capabilities and design expertise enhance regional product quality standards. The growth of e-commerce and targeted marketing strategies further improves market penetration. Urbanization, evolving consumer preferences, and cultural influences continue to sustain market growth, attracting both multinational and regional manufacturers.

The Middle East and Africa region is expected to record the highest CAGR of 6.01% through 2031, driven by increased female labor force participation and growing consumer interest in alternative metals and contemporary designs. According to the General Authority for Statistics (GASTAT), Saudi Arabia's female labor force participation rate reached 36.2% in the third quarter of 2024. Retail sector reforms in Saudi Arabia have expanded retail spaces and facilitated the entry of international brands. Rising demand for affordable accessories among younger consumers and market expansion by global retailers are reshaping competitive dynamics. Additionally, evolving regulations and increased digital market penetration are creating new revenue opportunities for both established firms and new entrants.

North America and Europe remain critical markets for premium segments and innovation in fashion jewelry. These developed regions are home to established luxury brands and e-commerce companies that influence sustainability practices, product customization, and multi-channel retail operations. In the United States, customs enforcement regulations help reduce counterfeit imports, protecting authorized manufacturers and ensuring market quality. In Europe, consumer demand for certified responsible materials compels companies to provide supply chain documentation and enhance operational transparency. Both regions serve as primary testing grounds for retail initiatives, such as remote consultations and product return programs, before global implementation, underscoring their strategic importance in the fashion jewelry market.

- LVMH (Moet Hennessy Louis Vuitton)

- Kering S.A.

- Swarovski AG

- Clairea's Holdings LLC

- Billig Jewelers, Inc.

- Richemont SA

- Fossil Group Inc.

- BaubleBar Inc.

- H&M Group (H&M Accessories)

- Inditex (Zara Accessories)

- Authentic Brands Group, LLC

- Lovisa Holdings Ltd.

- Natura &Co Holding S.A.

- Chanel Limited

- Tory Burch LLC

- Stella & Dot LLC

- Buckle Inc.

- Giorgio Armani S.p.A

- The Colibri Group

- Pandora A/S

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Affordability compared to fine jewelry

- 4.2.2 Fast fashion and trend-driven consumption

- 4.2.3 Rising influence of social media and fashion influencers

- 4.2.4 Adoption of short-run 3-D printing enabling mass-customized pieces

- 4.2.5 Rise of genderless/unisex jewelry

- 4.2.6 Design innovation and material versatility

- 4.3 Market Restraints

- 4.3.1 Volatile base-metal commodity prices squeezing margins

- 4.3.2 Proliferation of inexpensive counterfeits diluting brand equity

- 4.3.3 Perceived lower quality and durability

- 4.3.4 Skin sensitivity and health concerns

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Rings

- 5.1.2 Necklace and Chains

- 5.1.3 Earrings

- 5.1.4 Bracelets and Bangles

- 5.1.5 Pendants

- 5.1.6 Other Product Types (Brooches and Pins, and Cufflinks and Studs, etc)

- 5.2 By Material

- 5.2.1 Metal-based

- 5.2.2 Plastics and Acrylics

- 5.2.3 Glass and Crystal

- 5.2.4 Others (Wood, Resin, Leather and Fabric, etc)

- 5.3 By End User

- 5.3.1 Women

- 5.3.2 Men

- 5.3.3 Unisex

- 5.4 By Distribution Channel

- 5.4.1 Offline Retail Stores

- 5.4.2 Online Retail Stores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 LVMH (Moet Hennessy Louis Vuitton)

- 6.4.2 Kering S.A.

- 6.4.3 Swarovski AG

- 6.4.4 Clairea's Holdings LLC

- 6.4.5 Billig Jewelers, Inc.

- 6.4.6 Richemont SA

- 6.4.7 Fossil Group Inc.

- 6.4.8 BaubleBar Inc.

- 6.4.9 H&M Group (H&M Accessories)

- 6.4.10 Inditex (Zara Accessories)

- 6.4.11 Authentic Brands Group, LLC

- 6.4.12 Lovisa Holdings Ltd.

- 6.4.13 Natura &Co Holding S.A.

- 6.4.14 Chanel Limited

- 6.4.15 Tory Burch LLC

- 6.4.16 Stella & Dot LLC

- 6.4.17 Buckle Inc.

- 6.4.18 Giorgio Armani S.p.A

- 6.4.19 The Colibri Group

- 6.4.20 Pandora A/S

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK