PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061817

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061817

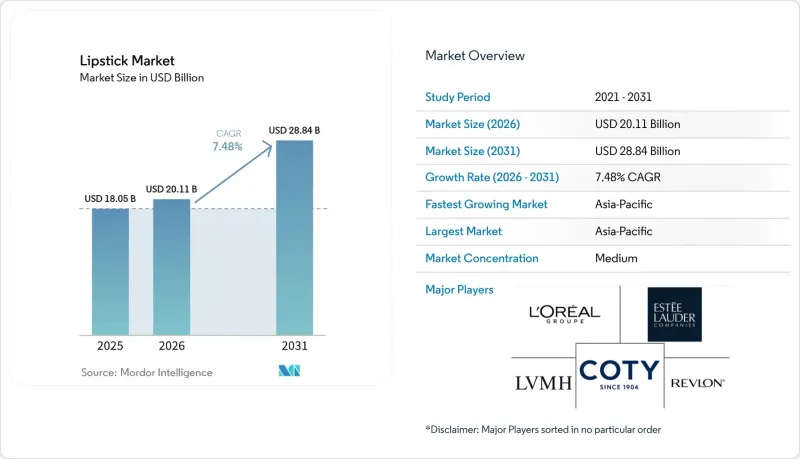

Lipstick - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the lipstick market was valued at USD 18.05 billion in 2025, and is expected to reach USD 20.11 billion in 2026, and is projected to grow to USD 28.84 billion by 2031, registering a CAGR of 7.48% during the forecast period.

This report is Segmented by Finish (Matte, Satin/Cream, and More), Form (Stick, Liquid, Crayon, and Palette), Price Range (Mass, and Premium and Luxury), Ingredient Type (Conventional and Clean Label), Distribution Channel (Supermarkets/Hypermarkets, Specialty Stores, Online Retail Stores, and Others), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Lipstick Market Trends and Insights

Rising beauty consciousness and personal grooming

The post-pandemic recovery in makeup consumption highlights the "lipstick effect," a consumer behavior trend where individuals opt for affordable luxury items during periods of economic uncertainty. This phenomenon occurs as consumers shift their spending from high-end luxury goods to more accessible indulgences, particularly cosmetics. For instance, John Lewis reported a 14% rise in lip product sales, with these items emerging as status symbols akin to luxury accessories. The trend is also broadening its reach, with male consumers, especially in China, increasingly purchasing cosmetics. Lip products have become entry-level items for makeup experimentation, signifying a broader movement toward self-expression and personal branding. This pattern is particularly pronounced in emerging markets, where rising disposable incomes are driving higher expenditure on beauty products.

Product innovation and texture Diversification

Recent advancements in lipstick formulation technology address consumer concerns by combining color cosmetics with skincare benefits. Shiseido's "Automatic Veil Technology" enhances product durability by enabling lipstick films to self-repair minor damage caused by regular use. This technology incorporates specialized polymers that respond to mechanical stress, redistributing the product to maintain an even layer on the lips, potentially extending the product's lifespan. Similarly, Global Bioenergies has introduced plant-based isododecane, offering a sustainable alternative to petroleum-derived ingredients while maintaining performance standards. This plant-based isododecane is produced through a fermentation process using renewable resources, resulting in a molecularly identical substitute for conventional petroleum-based components. Additionally, consumer demand for extended-wear products continues to drive growth in the long-lasting cosmetics market. These innovations are significant as companies strive to replace synthetic waxes with plant-based alternatives.

Health concerns around PFAS and heavy-metal pigments

Regulatory actions targeting per- and polyfluoroalkyl substances (PFAS) in cosmetics are causing notable market disruptions and increasing reformulation costs across various regions. In May 2025, the FDA rejected 89 batches of imported cosmetics, with 50 batches classified as "unapproved new drugs" due to ingredient safety classification issues. New Zealand's Environmental Protection Authority has announced a PFAS ban in cosmetics, set to take effect in December 2026. Similarly, the European Union's evaluation of PFAS restrictions under REACH, following France's implementation of a ban in January 2026, has introduced diverse compliance requirements impacting global supply chain operations. Companies are now required to invest in alternative formulation technologies while addressing performance challenges, such as developing plant-based substitutes for synthetic waxes that preserve product quality. These regulatory changes are creating market uncertainty and increasing development costs, particularly for smaller brands with limited research and development capabilities to meet varying regulatory demands.

Other drivers and restraints analyzed in the detailed report include:

- Demand for natural, vegan, and sustainable products

- Influence of social media and beauty influencers and celebrity brands

- Increasing availability of counterfeit products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The satin/cream finish lipsticks accounted for a dominant market share of 44.34% in 2025, while the matte lipstick segment is projected to grow at a CAGR of 7.59% during 2026-2031. The growth of the matte lipstick segment is driven by increasing demand for long-lasting, transfer-resistant products that align with consumer preferences. Advances in formulation technology have contributed to this growth by addressing traditional comfort challenges. Manufacturers are introducing hybrid formulations that combine the matte finish with improved wearability and moisturizing properties.

Satin finish lipsticks continue to be popular due to their versatility and appeal across various age groups. These lipsticks offer a balanced combination of color intensity and comfortable wear without feeling heavy on the lips. Their formulation ensures easy application and long-lasting results, making them suitable for both professional settings and casual occasions. The moderate sheen of satin finishes provides a natural-looking appearance while maintaining vibrant color throughout the day. The "Others" category, which includes glossy, metallic, and specialty finishes, presents emerging opportunities for differentiation. Brands are exploring innovative textures and effects, leveraging the visual-first culture of social media to attract consumers.

Stick formats maintained a dominance with a 59.18% market share in 2025, while the liquid lipstick segment is expected to grow at a CAGR of 7.81% during 2026-2031. This growth is driven by innovations in applicator technology and the influence of viral social media trends showcasing dramatic color transformations. Liquid formulations offer superior color intensity and longevity compared to traditional stick formats, appealing to consumers seeking professional-quality results and extended wear. Market growth reflects advancements in liquid lipstick formulations that address issues such as drying, flaking, and uneven application through improved chemical compositions and applicator designs.

Stick formats continue to dominate the market due to their convenience, portability, and ease of application, particularly for consumers requiring quick touch-ups and on-the-go solutions. Crayon formats attract younger consumers looking for user-friendly products, while palette formats cater to professional makeup artists and enthusiasts who prioritize color customization and blending options. The market reflects a division between traditional formats emphasizing convenience and innovative liquid formulations focusing on performance. Companies are increasingly offering hybrid products that combine features from multiple formats to appeal to a broader consumer base.

Geography Analysis

Asia-Pacific dominated the global lipstick market with a 34.40% share in 2025 and is projected to experience the fastest regional growth at a CAGR of 8.01% from 2026 to 2031. This growth is attributed to the expanding middle-class population, rising disposable incomes, and cultural shifts toward beauty consciousness in key markets such as China, India, and Japan. The region's growth is further supported by the success of local brands, exemplified by Chinese brand Florasis, which achieved top-seller status on Amazon Japan through culturally-inspired collections. This highlights the potential for regional brands to achieve cross-border success. Additionally, the region's digital-first consumer behavior is transforming distribution channels, with social commerce and livestream selling gaining significant traction in markets like China and South Korea.

North America and Europe are characterized as mature markets with established infrastructure and sophisticated consumer preferences. Growth in these regions is driven by trends such as premiumization, the adoption of clean beauty products, and advancements in retail technology. However, these markets face significant regulatory pressures related to ingredient safety. For instance, PFAS restrictions in the United States and European Union REACH evaluations are creating compliance challenges, favoring larger brands with robust research and development capabilities to navigate these regulatory landscapes.

The Middle East and Africa lipstic market is experiencing growth driven by social reforms that empower women and foster new consumption patterns. The region's unique climate conditions are encouraging the development of specialized formulations designed to withstand extreme weather, creating opportunities for brands that can meet these specific performance requirements. South America presents significant growth potential in the beauty market. Regional companies such as Natura and O Boticario maintain strong domestic market positions, while international brands are expanding their presence through digital platforms and strategic partnerships. Growth in this region is fueled by improved e-commerce infrastructure and increased social media usage, which facilitate brand discovery and influence purchasing behavior, particularly among younger consumers.

- L'Oreal Group

- Estee Lauder Companies

- Coty Inc.

- Revlon Inc.

- LVMH (Parfums & CosmA(C)tiques)

- Shiseido Co.

- Chanel SAS

- Procter & Gamble (Max Factor)

- Avon Products

- Purplle.(Faces Canada)

- Kao Corp. (Kanebo)

- Sugar Cosmetics

- Oriflame Holding

- Huda Beauty

- Kylie Cosmetics

- ColourPop (CPD LLC)

- Glossier Inc.

- Rare Beauty

- Hindustan Unilever Limited (Lakme)

- Colorbar Cosmetics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising beauty consciousness and personal grooming

- 4.2.2 Product innovation and texture Diversification

- 4.2.3 Demand for natural, vegan, and sustainable products

- 4.2.4 Influence of social media and beauty influencers and celebrity brands

- 4.2.5 Premiumization and aspirational consumption

- 4.2.6 Innovative, sustainable packaging enhancing user experience and brand appeal

- 4.3 Market Restraints

- 4.3.1 Health concerns around PFAS and heavy-metal pigments

- 4.3.2 Increasing availability of counterfeit products

- 4.3.3 Regulatory challenges

- 4.3.4 Sustainability and environmental issues

- 4.4 Supply Chain Analysis

- 4.5 Consumer Behavior Analysis

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Finish

- 5.1.1 Matte

- 5.1.2 Satin/Cream

- 5.1.3 Gloss

- 5.1.4 Others

- 5.2 By Form

- 5.2.1 Stick

- 5.2.2 Liquid

- 5.2.3 Crayon

- 5.2.4 Palette

- 5.3 By Price Range

- 5.3.1 Mass

- 5.3.2 Premium and Luxury

- 5.4 By Ingredient Type

- 5.4.1 Conventional

- 5.4.2 Clean Label

- 5.5 By Distribution Channel

- 5.5.1 Supermarkets/Hypermarkets

- 5.5.2 Specialty Stores

- 5.5.3 Online Retail Stores

- 5.5.4 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.1.4 Rest of North America

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 Italy

- 5.6.2.4 France

- 5.6.2.5 Spain

- 5.6.2.6 Netherlands

- 5.6.2.7 Poland

- 5.6.2.8 Belgium

- 5.6.2.9 Sweden

- 5.6.2.10 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 Australia

- 5.6.3.5 Indonesia

- 5.6.3.6 South Korea

- 5.6.3.7 Thailand

- 5.6.3.8 Singapore

- 5.6.3.9 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Colombia

- 5.6.4.4 Chile

- 5.6.4.5 Peru

- 5.6.4.6 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 South Africa

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 Nigeria

- 5.6.5.5 Egypt

- 5.6.5.6 Morocco

- 5.6.5.7 Turkey

- 5.6.5.8 Rest of Middle East and Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share for key companies, Products, and Recent Developments)

- 6.4.1 L'Oreal Group

- 6.4.2 Estee Lauder Companies

- 6.4.3 Coty Inc.

- 6.4.4 Revlon Inc.

- 6.4.5 LVMH (Parfums & CosmA(C)tiques)

- 6.4.6 Shiseido Co.

- 6.4.7 Chanel SAS

- 6.4.8 Procter & Gamble (Max Factor)

- 6.4.9 Avon Products

- 6.4.10 Purplle.(Faces Canada)

- 6.4.11 Kao Corp. (Kanebo)

- 6.4.12 Sugar Cosmetics

- 6.4.13 Oriflame Holding

- 6.4.14 Huda Beauty

- 6.4.15 Kylie Cosmetics

- 6.4.16 ColourPop (CPD LLC)

- 6.4.17 Glossier Inc.

- 6.4.18 Rare Beauty

- 6.4.19 Hindustan Unilever Limited (Lakme)

- 6.4.20 Colorbar Cosmetics

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK