PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061831

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061831

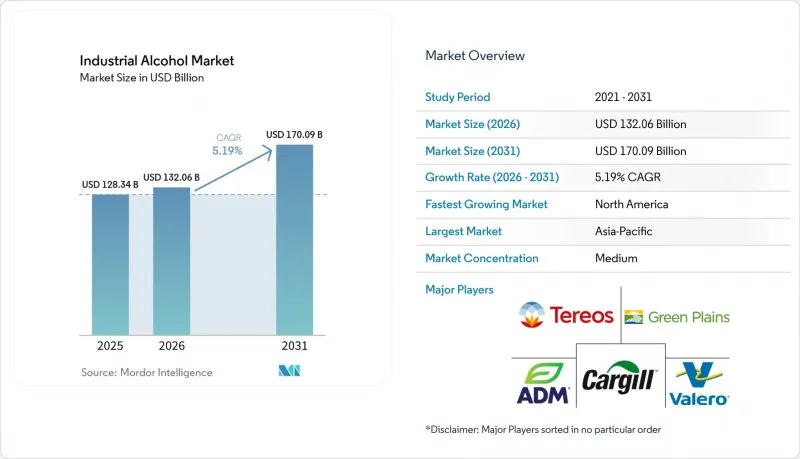

Industrial Alcohol - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the industrial alcohol market size is projected to grow from USD 128.34 billion in 2025 to USD 132.06 billion in 2026, reaching USD 170.09 billion by 2031, with a CAGR of 5.19% during the forecast period of 2026-2031.

This report is Segmented by Type (Ethyl Alcohol, Methyl Alcohol, Isopropyl Alcohol, Isobutyl Alcohol, Others), Source (Corn, Sugar and Molasses, Grains, and More), Application (Cosmetics and Personal Care, Food and Beverages, Fuel and Energy, Pharmaceuticals, Others), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Industrial Alcohol Market Trends and Insights

Increasing demand for industrial alcohol in biofuels

The biofuels market is driving increased demand for industrial alcohol due to mandatory blending requirements and carbon reduction targets in key economies. According to the U.S. Energy Information Administration, fuel ethanol production is projected to reach 1.05 million barrels per day by 2025 . In the European Union, the ReFuelEU Aviation mandate requires a 2% sustainable aviation fuel (SAF) blending by 2025, with a target of 70% by 2050. Similarly, India's goal of achieving 20% ethanol blending by 2025 is expected to generate an annual demand of 240 billion liters, significantly impacting global supply chains. The alcohol-to-jet fuel pathway is also advancing, with LanzaJet's Freedom Pines facility set to produce 10 million gallons of sustainable aviation fuel annually starting in 2025. This rising demand is leading to supply constraints, particularly in corn-based ethanol production, as feedstock costs increase due to competition between food and fuel uses. To address regulatory requirements and access low-carbon fuel markets, ethanol producers are adopting carbon capture technologies, such as Green Plains' project to sequester 800,000 tons of CO2 annually.

Rising technological innovations in extraction processes

Advancements in extraction and purification technologies are enhancing the efficiency of industrial alcohol production while minimizing environmental impact and operational costs. In March 2025, ExxonMobil announced a USD 100 million investment in ultra-pure isopropyl alcohol production at its Baton Rouge facility, aiming for 99.999% purity levels to meet the demands of semiconductor manufacturing. Researchers at the Gwangju Institute of Science and Technology have improved the efficiency of converting CO2 into allyl alcohol using electrochemical processes, setting new performance benchmarks for large-scale production. The integration of artificial intelligence and machine learning in fermentation control systems is optimizing yield rates and reducing processing times, with RCM Technologies introducing capacity enhancement solutions for ethanol plants. Methanol-to-jet technology is emerging as an alternative to traditional Fischer-Tropsch processes, with ExxonMobil developing methods to convert alternative feedstocks into synthetic jet fuel components. These technological advancements are enabling producers to access higher-margin applications while improving resource utilization.

High manufacturing and energy costs

Energy accounts for 25-35% of ethanol production cash costs, making distilleries highly sensitive to fluctuations in natural gas and electricity prices. European producers face electricity costs that are 2-3 times higher than those of their U.S. counterparts, creating a structural disadvantage that has led several facilities to reduce or idle capacity during periods of peak winter pricing. Strategic responses to this challenge vary: large integrated producers are co-locating with renewable natural gas sources or installing on-site solar energy systems, while smaller distillers are either exiting the market or consolidating operations. The volatility in energy costs poses a significant risk, as it can quickly turn a profitable quarter into a loss, especially for producers without long-term utility contracts, where adjustments to feedstock hedges may not be sufficient to offset the impact.

Other drivers and restraints analyzed in the detailed report include:

- Abundant raw material availability

- Government policies and incentives

- Supply chain disruptions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ethyl alcohol accounted for a significant market share of 51.13% in 2025 and is projected to grow at a CAGR of 5.56% through 2031. This growth is attributed to its extensive use in fuel, pharmaceutical, and industrial applications. The segment's development is further supported by regulations promoting sustainable aviation fuel and rising demand for pharmaceutical manufacturing. Companies such as LanzaJet are advancing alcohol-to-jet technologies to convert ethanol into aviation fuel. Meanwhile, isobutyl alcohol and other specialty alcohols continue to cater to niche applications in the solvents, adhesives, and chemical intermediates markets.

The planned opening of European Energy's Kasso e-methanol facility in May 2025 highlights progress in methanol production through the integration of renewable energy and carbon capture technologies. Additionally, Korean researchers have made notable advancements in CO2-to-alcohol conversion efficiency, introducing innovative production methods that could impact the manufacturing costs of methanol and ethanol. Market competition has intensified as producers adopt carbon capture technologies and prioritize high-purity products for premium markets, while also striving to remain competitive in traditional fuel and solvent segments.

Geography Analysis

Asia-Pacific held a 40.41% share of the industrial alcohol market in 2025, driven by the availability of agricultural feedstock, government biofuel mandates, and robust manufacturing capabilities in countries like China, India, and Southeast Asia. India's ethanol production reached 6.35 billion liters in 2024, leading the region's growth in ethanol production through the utilization of sugarcane and grain. The region benefits from competitive advantages such as lower production costs, supportive regulations, and proximity to end-use markets, solidifying its role as a global production hub for industrial alcohol applications.

North America is projected to exhibit the fastest regional growth, with a CAGR of 5.58% through 2031, supported by advancements in carbon capture technologies, sustainable aviation fuel mandates, and premium application development. In 2023, the U.S. biofuels production capacity increased by 7% to 24 billion gallons annually, with renewable diesel and other biofuels rising by 44%, while fuel ethanol capacity reached 18 billion gallons, according to the U.S. Energy Information Administration. ExxonMobil's USD 100 million investment in ultra-pure isopropyl alcohol production at Baton Rouge aims to support semiconductor manufacturing applications. According to Government of Canada data, the excise duty adjustments in Canada, effective April 2025, will limit rate increases to a maximum of 2% for an additional two years, offering regulatory stability for producers .

Europe faces challenges related to feedstock cost pressures and regulatory compliance while advancing sustainable production processes and carbon management systems. The European Union's ReFuelEU Aviation mandate requires sustainable aviation fuel blending, starting at 2% in 2025 and increasing to 70% by 2050, driving demand for alcohol-to-jet conversion technologies. Suntory's collaboration with Tokyo Gas achieved 99.5% CO2 recovery purity during distillation processes at its Hakushu Distillery, showcasing the integration of carbon capture in alcohol production. The region's market position is supported by technological innovation, environmental compliance capabilities, and access to premium markets that prioritize sustainability credentials.

- Archer Daniels Midland Company (ADM)

- Cargill Inc.

- POET LLC

- Valero Energy Corporation

- Green Plains Inc.

- Tereos S.A.

- Cristalco SAS

- Wilmar International Limited

- The Andersons, Inc.

- CropEnergies AG

- Sasol Limited

- Illovo Sugar Africa (Pty) Ltd

- NCP Alcohols (Pty) Ltd

- Grain Processing Corporation

- Godavari Biorefineries Ltd

- Praj Industries Limited

- LyondellBasell Industries Holdings B.V.

- Sekab Biofuels & Chemicals AB

- Mitsubishi Corporation (Chemical Division)

- Manildra Group

- Exxon Mobil Corporation.

- Shree Renuka Sugars Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing demand for industrial alcohol in biofuels

- 4.2.2 Rising technological innovations in extraction processes

- 4.2.3 Abundant raw material availability

- 4.2.4 Government policies and incentives

- 4.2.5 Emerging market expansions

- 4.2.6 Increasing demand for sustainable and renewable products

- 4.3 Market Restraints

- 4.3.1 High manufacturing and energy costs

- 4.3.2 Supply chain disruptions

- 4.3.3 Market fragmentation and intense competition

- 4.3.4 Taxation and price controls

- 4.4 Supply Chian Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Type

- 5.1.1 Ethyl Alcohol

- 5.1.2 Methyl Alcohol

- 5.1.3 Isopropyl Alcohol

- 5.1.4 Isobutyl Alcohol

- 5.1.5 Others

- 5.2 By Source

- 5.2.1 Corn

- 5.2.2 Sugar and Molases

- 5.2.3 Grains

- 5.2.4 Lignocellulosic Biomass

- 5.2.5 Industrial Gas and Waste Streams

- 5.3 By Application

- 5.3.1 Cosmetics and Personal Care

- 5.3.2 Food and Beverages

- 5.3.3 Fuel and Energy

- 5.3.4 Pharmaceuticals

- 5.3.5 Others (Solvents and Chemicals, Laboratory, Adhesives)

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Poland

- 5.4.2.8 Belgium

- 5.4.2.9 Sweden

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Indonesia

- 5.4.3.6 South Korea

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Chile

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Moves

- 6.2 Market Ranking Analysis

- 6.3 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.3.1 Archer Daniels Midland Company (ADM)

- 6.3.2 Cargill Inc.

- 6.3.3 POET LLC

- 6.3.4 Valero Energy Corporation

- 6.3.5 Green Plains Inc.

- 6.3.6 Tereos S.A.

- 6.3.7 Cristalco SAS

- 6.3.8 Wilmar International Limited

- 6.3.9 The Andersons, Inc.

- 6.3.10 CropEnergies AG

- 6.3.11 Sasol Limited

- 6.3.12 Illovo Sugar Africa (Pty) Ltd

- 6.3.13 NCP Alcohols (Pty) Ltd

- 6.3.14 Grain Processing Corporation

- 6.3.15 Godavari Biorefineries Ltd

- 6.3.16 Praj Industries Limited

- 6.3.17 LyondellBasell Industries Holdings B.V.

- 6.3.18 Sekab Biofuels & Chemicals AB

- 6.3.19 Mitsubishi Corporation (Chemical Division)

- 6.3.20 Manildra Group

- 6.3.21 Exxon Mobil Corporation.

- 6.3.22 Shree Renuka Sugars Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK