PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061836

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061836

Plus Size Clothing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

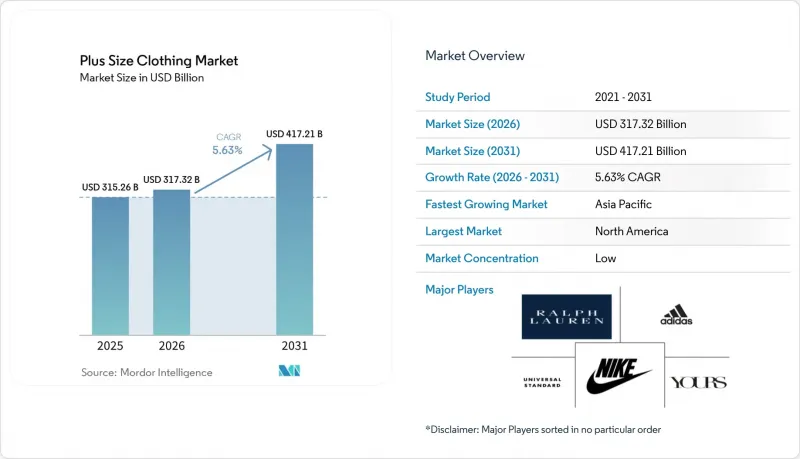

According to Mordor Intelligence, the plus-size clothing market size is projected to expand from USD 315.26 billion in 2025 and USD 317.32 billion in 2026 to USD 417.21 billion by 2031, registering a 5.63% CAGR between 2026 and 2031.

This report is Segmented by Product Type (Formal Wear, Casual Wear, Sportswear, Nightwear and More), End User (Women, Men, Unisex), Price Range (Mass, Premium/Luxury), Distribution Channel (Online Retail Stores, Offline Retail Stores), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Plus Size Clothing Market Trends and Insights

Body positivity movement

Cultural shifts toward body acceptance are reconfiguring demand patterns, particularly among millennial and Gen Z consumers who reject traditional beauty standards. The young consumers actively seek brands that feature diverse body types in marketing campaigns, translating advocacy into purchasing power. This movement has compelled legacy brands to expand size ranges not as a corporate social responsibility gesture but as a revenue imperative. The impact extends beyond marketing; it influences product development cycles, with brands now designing for extended sizes from the outset rather than scaling up standard patterns, which historically resulted in poor fit and higher return rates. Regulatory bodies like the Federal Trade Commission in the United States have begun scrutinizing size-labeling practices, adding compliance pressure that reinforces the business case for authentic inclusivity.

Expanded brand sizing programs

Responding to consumer demand and competitive pressures, major apparel companies are expanding their size ranges. Nike's women's activewear in extended sizes has seen revenue growth surpassing the company's overall apparel growth. These initiatives extend beyond merely adding SKUs (Stock Keeping Units); they encompass retooling supply chains, retraining fit models, and fine-tuning inventory algorithms to avert stockouts in popular extended sizes. This heightened focus on size inclusivity signals a significant shift in the apparel market, where consumer demands for diversity and representation are reshaping product strategies. The trend highlights the growing importance of catering to a broader demographic, as consumers increasingly prioritize brands that reflect their values. The message is clear: brands that delay may cede ground to digitally native competitors like Universal Standard, which has built its entire value proposition around size inclusivity from the outset.

Limited shelf space for extended sizes

Physical retail environments impose strict limits on assortment breadth, compelling merchandisers to balance size range with style variety. This challenge arises from a cautious approach to inventory; historically, extended sizes have seen higher return rates and slower turnover, prompting buyers to limit their exposure. This limitation creates a cycle: a restricted selection pushes consumers online, reinforcing retailers' hesitance to broaden in-store offerings. In response, brands are testing "endless aisle" models, showcasing one size in-store while providing the full range through in-store tablets for home delivery. However, this method forgoes the tactile assessment crucial for apparel purchases. Retailers are also exploring hybrid approaches, such as offering limited in-store inventory for trial while integrating online fulfillment to cater to broader preferences. These strategies aim to strike a balance between operational efficiency and customer satisfaction.

Other drivers and restraints analyzed in the detailed report include:

- Social-media driven demand spikes

- Increasing demand for luxury and premium plus-size clothing

- Higher fabric and logistics costs per garment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Casual wear retained the largest slice at 31.22% of plus size clothing market share in 2025, thanks to joggers, oversized tees, and hoodies that anchor everyday wardrobes. Elevated time at home during and after the pandemic entrenched comfort-first dressing habits, generating frequent replenishment cycles. Yet commoditization pressures margins, pushing mid-range retailers to experiment with elevated trims, gender-neutral styling, and limited-edition drops to sustain newness. Formal, nightwear, intimate, and maternity segments remain smaller but are diversifying quickly as brands recognize profit potential in well-served niches.

Sportswear's contribution to the plus-size clothing market size climbed steadily and is projected to expand at 7.65% CAGR during 2026-2031, the highest across categories. Performance-grade leggings, moisture-wicking tops, and high-support sports bras are now engineered up to 6XL, closing the quality gap that once deterred active consumers. Nike and Adidas have partnered with plus-size athletes to validate technical credibility, while upstarts like Girlfriend Collective leverage recycled fabrics to capture eco-conscious shoppers. This wave lifts average selling prices and fortifies brand storytelling around empowerment and wellness.

Men dominated revenue with 69.32% plus size clothing market share in 2025, supported by higher average order values and longer product lifecycles for shirts, denim, and outerwear. This trend is underscored by CDC (Centers for Disease Control and Prevention) data revealing that over 40% of United States adults grapple with obesity, with men notably more affected in various statesSpecialty chains such as DXL and Johnny Bigg curate deep assortments that mainstream retailers rarely match, bolstering loyalty and reducing return risk.

Women's apparel is the plus-size clothing market's fastest-advancing end-user segment, registering a 7.58% CAGR for 2026-2031. Social-media personalities spotlight aspirational styling, amplifying demand for trend-driven blazers, slip dresses, and statement denim in sizes up to 40. Digitally native brands like Universal Standard embed "fit liberty" guarantees that let shoppers exchange garments as body shapes evolve, reinforcing trust. Unisex lines add modest incremental sales, attracting Gen Z consumers who value gender-fluid expression.

Geography Analysis

North America contributed the largest regional block, holding 45.12% of plus size clothing market share in 2025. High obesity prevalence, robust discretionary income, and advanced e-commerce ecosystems together sustain top-line momentum. United States regulators have begun scrutinizing deceptive size labeling, nudging brands toward transparent measurement charts that ease cross-brand shopping. Canada mirrors these trends, with domestic labels like Addition Elle leveraging local fit data to improve pattern accuracy, while Mexico offers untapped upside as middle-income consumers seek branded alternatives to bespoke tailoring.

Asia-Pacific is projected to log the fastest regional growth at a 5.48% CAGR during 2026-2031, underpinned by rapid urbanization and evolving diets. China's rising middle class demands Western-inspired streetwear extended to 6XL, whereas India's nascent segment benefits from indigenous brands adapting kurtas and saree blouses for larger frames. Japan and South Korea show smaller absolute opportunity given lower obesity rates but exhibit outsized social-commerce uptake, which boosts visibility for inclusive labels. Australia, aligned culturally with North America, already houses specialty retailers like City Chic that export expertise throughout the region.

Europe, South America, and the Middle East and Africa collectively supply the remaining revenue. Europe's stringent consumer-protection climate and initiatives such as the SizeEU project push companies toward standardized sizing, gradually building trust for cross-border digital sales. Brazil leads South America on the back of a vibrant influencer scene promoting body diversity, while Chile and Colombia follow. The Middle East's opportunity is clustered in cosmopolitan centers like Dubai where international chains pilot inclusive offerings, though cultural sensibilities still moderate marketing approaches. Africa remains early stage, but textile capacity in countries like Ethiopia may emerge as a sourcing alternative for global players seeking cost efficiencies in the plus size clothing market.

- Nike Inc.

- Adidas AG

- Ralph Lauren Corporation

- Yours Clothing Limited

- Bloom Exim Pvt. Ltd. (John Pride)

- Power Sutra Clothing Pvt. Ltd.

- Lane Bryant Brands Opco LLC

- ASOS plc

- You and All

- Leonisa S.A.

- Kohl's Corporation

- Urban Outfitters Inc.

- Donovan Apparels Pvt. Ltd. (bigbanana)

- Big Bud Press

- Weft Apparel

- Universal Standard Inc.

- FullBeauty Brands Operations LLC

- Torrid Holdings Inc.

- House of Flint

- plusS

- Boohoo Group plc

- Gap Inc.

- Dia & Co

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Body-positivity movement

- 4.2.2 Expanded brand sizing programs

- 4.2.3 Social-media driven demand spikes

- 4.2.4 Increasing Demand for Luxury and Premium Plus-Size Clothing

- 4.2.5 Rise of adaptive plus-size apparel for people with disabilities

- 4.2.6 Sports and Activewear Inclusivity

- 4.3 Market Restraints

- 4.3.1 Limited shelf space for extended sizes

- 4.3.2 Higher fabric and logistics costs per garment

- 4.3.3 Inconsistent international sizing standards

- 4.3.4 Supply Chain and Inventory Management

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Value / Supply-Chain Analysis

- 4.8 Porter's Five Forces

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Formal Wear

- 5.1.2 Casual Wear

- 5.1.3 Sportswear

- 5.1.4 Nightwear and Loungewear

- 5.1.5 Intimate and Shapewear

- 5.1.6 Maternity Wear

- 5.2 By End-user

- 5.2.1 Women

- 5.2.2 Men

- 5.2.3 Unisex

- 5.3 By Price Range

- 5.3.1 Mass

- 5.3.2 Premium /Luxury

- 5.4 By Distribution Channel

- 5.4.1 Online Retail Stores

- 5.4.2 Offline Retail Stores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Nike Inc.

- 6.4.2 Adidas AG

- 6.4.3 Ralph Lauren Corporation

- 6.4.4 Yours Clothing Limited

- 6.4.5 Bloom Exim Pvt. Ltd. (John Pride)

- 6.4.6 Power Sutra Clothing Pvt. Ltd.

- 6.4.7 Lane Bryant Brands Opco LLC

- 6.4.8 ASOS plc

- 6.4.9 You and All

- 6.4.10 Leonisa S.A.

- 6.4.11 Kohl's Corporation

- 6.4.12 Urban Outfitters Inc.

- 6.4.13 Donovan Apparels Pvt. Ltd. (bigbanana)

- 6.4.14 Big Bud Press

- 6.4.15 Weft Apparel

- 6.4.16 Universal Standard Inc.

- 6.4.17 FullBeauty Brands Operations LLC

- 6.4.18 Torrid Holdings Inc.

- 6.4.19 House of Flint

- 6.4.20 plusS

- 6.4.21 Boohoo Group plc

- 6.4.22 Gap Inc.

- 6.4.23 Dia & Co

7 Market Opportunities and Future Outlook