PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061886

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061886

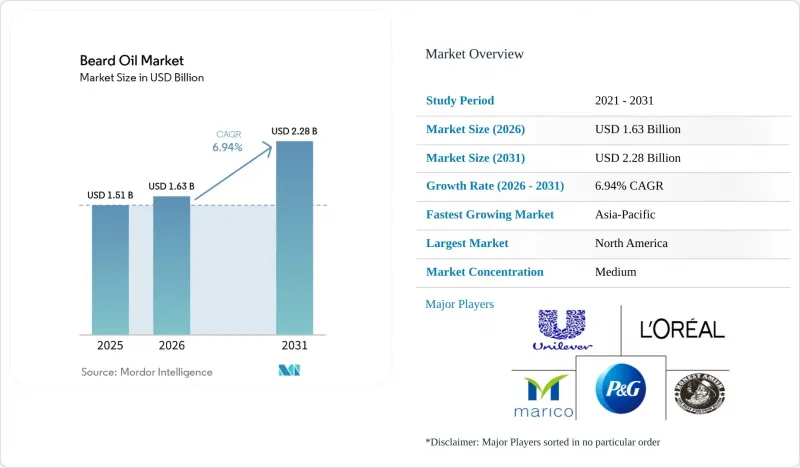

Beard Oil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the beard oil market size is expected to grow from USD 1.51 billion in 2025 to USD 1.63 billion in 2026 and is forecast to reach USD 2.28 billion by 2031 at a 6.94% CAGR over 2026-2031.

This report is Segmented by Category (Natural and Conventional), Ingredient (Carrier Oils and Carrier Oils With Essential Oil Mix), Distribution Channel (Online Retail Stores, Supermarkets and Hypermarkets, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Beard Oil Market Trends and Insights

Celebrity and Social Media-Driven Beard Fashion Trend

Beard fashion, once a niche aesthetic, has surged into the mainstream, thanks to celebrity endorsements and viral social media campaigns. In Q4 2025, Viking Revolution harnessed the power of TikTok, rolling out 18,000 creator videos and raking in a notable USD 1.5 million in sales via TikTok Shop. This underscores the platform's prowess in driving both discovery and sales for grooming products. Dr. Squatch's strategic partnerships with icons like Sydney Sweeney and brands such as SpongeBob SquarePants and Call of Duty highlight the potency of pop-culture collaborations in broadening market reach, extending well beyond the conventional male grooming audience. Meanwhile, social-first marketing is leveling the playing field: micro-brands are now challenging FMCG behemoths by cultivating genuine communities and harnessing user-generated content, which often strikes a more resonant chord than traditional TV advertisements. This evolving landscape is also influencing product development: brands are unveiling limited-edition scents, teaming up with influencers for unique blends, and employing social listening to pinpoint and address unmet consumer needs. Scotch Porter, with a remarkable growth rate surpassing 70% annually, attributes its success to a keen focus on multicultural grooming demands and strategic alliances with Black influencers, effectively carving out a unique space in a saturated market.

Rapid Growth of E-Commerce Grooming Product Sales

Subscription models, tailored recommendations, and the ease of home delivery have propelled e-commerce to the forefront of beard oil sales. In 2025, online retail stores commanded a 45.72% share of the market, a lead they are poised to retain as digital-first brands expand and traditional retailers bolster their omnichannel strategies. Direct-to-consumer subscription models not only ensure steady revenue but also enhance customer lifetime value. For instance, Beardbrand, after revamping its fulfillment and manufacturing processes, surged its subscriber count from 1,500 to 11,000 in 2025, bouncing back to profitability after a challenging 2023-2024. In China's bustling male grooming e-commerce scene, Douyin (the Chinese equivalent of TikTok) claimed 32.9% of online beard care sales, while Tmall secured 34.8% in the first half of 2025. This shift to e-commerce is paving the way for precision marketing: brands can now tailor offerings based on beard type, skin sensitivity, and scent preference, delivering customized product bundles and content that outperform traditional retail in conversion rates.

Substitution Threat from Multifunctional Beard Balms and Serums

Time-constrained consumers are increasingly gravitating towards multifunctional grooming products that seamlessly blend conditioning, styling, and skincare benefits, sidelining traditional single-purpose beard oils. The U.S. beard balm market is witnessing a notable upswing, with surveys revealing a clear preference among male grooming enthusiasts for multifunctional products. These products streamline routines by reducing the number of SKUs. Furthermore, 35% of consumers are leaning towards lightweight textures, spurring innovation in water-based hybrid balms that deliver oil-like conditioning without the added weight. Beard serums, known for their concentrated active ingredients like biotin, caffeine, and peptides, are emerging as performance-driven alternatives to conventional carrier-oil blends. This shift is particularly pronounced in mature markets, where consumers, having embraced basic beard care, are now opting for premium, efficacy-focused products. To navigate this evolving landscape, brands can bundle oils with complementary items like balms and washes in subscription boxes or reformulate oils to incorporate functional actives, enhancing their standalone appeal. Highlighting this trend, BIC's February 2026 debut of the Flex 5 Trim and Shave, a versatile 2-in-1 tool, underscores the growing consumer demand for consolidated, multi-use solutions.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Natural and Organic Formulations

- Demand for Halal-Certified Beard Oils in Muslim-Majority Markets

- Climate-Induced Supply Volatility for Premium Carrier Oils

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, conventional beard oil formats command a dominant 59.59% share of the market revenue. Their stronghold is attributed to widespread consumer familiarity, prime shelf placements, and competitive pricing, making them the preferred choice for newcomers. Bolstered by a stable supply chain and decades of demonstrated effectiveness, these products have cultivated deep consumer trust, solidifying their pivotal role in daily grooming. Despite intensifying competition, the reliability of conventional oils ensures their continued prominence. Many users, especially in budget-sensitive markets, are drawn to these formulations for their affordability and consistent performance. Thus, conventional beard oils stand as the cornerstone of the segment, integral to the grooming rituals of many.

Natural beard oil products are emerging as the fastest-growing segment in the category, boasting a projected CAGR of 7.08%. This surge is fueled by a rising consumer appetite for clean-label and eco-friendly choices. Shoppers, ready to invest more, link organic certifications with safer, sustainably sourced ingredients. Brands spotlighting transparent sourcing, ethical ingredient choices, and eco-friendly packaging are reaping the rewards of this trend. Moreover, natural beard oils are poised to chip away at the market share of traditional products, nudging established brands towards reformulation and innovation. As the beauty industry increasingly embraces sustainability and health, established brands are reshaping their portfolios to align with today's discerning, ingredient-savvy consumers. Meanwhile, regulatory shifts are easing the path for natural products, offering them lenient scrutiny and straightforward labeling. In contrast, traditional formulations grapple with heightened mandates, facing stricter allergen disclosures and rigorous safety testing requirements.

Geography Analysis

In 2025, North America held a dominant 35.40% market share, driven by a deep-rooted grooming culture, a flurry of product launches, and robust disposable incomes. The U.S. led the regional turnover, capitalizing on celebrity endorsements and a vast retail network. Canada closely trailed, influenced by shared cultural cues and active cross-border e-commerce. Meanwhile, Mexico, despite its smaller size, is witnessing growth as its middle class increasingly engages with influencer content, aspiring to refined grooming standards.

Asia-Pacific, with a rapid 7.92% CAGR, is drawing significant attention. In China and South Korea, beauty-centric digital platforms and livestream shopping are driving momentum. Urban millennials are particularly keen on beard oil supplements. Southeast Asian nations are contributing to the growth as cross-border platforms simplify access to imported brands. Additionally, the region's preference for localized scents and lighter textures, tailored for humid conditions, is gaining traction.

Europe's growth is steady but more measured, influenced by strict safety regulations and a consumer tilt towards certified natural products. Germany and the UK spearhead consumption, while France's rich perfume legacy champions scent-centric blends. Eastern European nations, starting from a modest base, are expanding as economic recovery and Western media exposure reshape male grooming views. Furthermore, the EU Cosmetics Regulation's harmonized standards set a benchmark, ensuring non-European exporters elevate their product quality to meet these thresholds.

- L'Oreal S.A.

- Unilever PLC

- Procter & Gamble Co.

- Marico Limited (Beardo)

- Honest Amish LLC

- Viking Revolution LLC

- Edgewell Personal Care (Bulldog Skincare)

- Mountaineer Brand Products.

- Grave Before Shave

- Beardbrand Inc.

- Wild Willies (Manscape Labs)

- Bossman Brands Inc

- Zeus Beard LLC

- Seven Potions Ltd

- Scotch Porter LLC

- Reuzel USA, Inc.

- Beardilizer

- Murdock London Ltd

- Ranger Grooming Company

- Ludovico Martelli srl (Proraso)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising male grooming awareness

- 4.2.2 Celebrity and social media-driven beard fashion trend

- 4.2.3 Rapid growth of e-commerce grooming product sales

- 4.2.4 Shift toward natural and organic formulations

- 4.2.5 Direct-to-consumer micro-brand subscription models

- 4.2.6 Demand for halal-certified beard oils in Muslim-majority markets

- 4.3 Market Restraints

- 4.3.1 Substitution threat from multifunctional beard balms and serums

- 4.3.2 Price sensitivity in developing regions

- 4.3.3 Allergic reactions triggering stricter essential-oil regulations

- 4.3.4 Climate-induced supply volatility for premium carrier oils

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Category

- 5.1.1 Natural

- 5.1.2 Conventional

- 5.2 Ingredient

- 5.2.1 Carrier Oils

- 5.2.2 Carrier Oils with Essential Oil Mix

- 5.3 Distribution Channel

- 5.3.1 Supermarkets/Hypermarkets

- 5.3.2 Health and Beauty Stores

- 5.3.3 Online Retail Stores

- 5.3.4 Other Distribution channels

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Sweden

- 5.4.2.7 Belgium

- 5.4.2.8 Poland

- 5.4.2.9 Netherlands

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Thailand

- 5.4.3.5 Singapore

- 5.4.3.6 Indonesia

- 5.4.3.7 South Korea

- 5.4.3.8 Australia

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Peru

- 5.4.4.5 Chile

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 South Africa

- 5.4.5.3 Saudi Arabia

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 L'Oreal S.A.

- 6.4.2 Unilever PLC

- 6.4.3 Procter & Gamble Co.

- 6.4.4 Marico Limited (Beardo)

- 6.4.5 Honest Amish LLC

- 6.4.6 Viking Revolution LLC

- 6.4.7 Edgewell Personal Care (Bulldog Skincare)

- 6.4.8 Mountaineer Brand Products.

- 6.4.9 Grave Before Shave

- 6.4.10 Beardbrand Inc.

- 6.4.11 Wild Willies (Manscape Labs)

- 6.4.12 Bossman Brands Inc

- 6.4.13 Zeus Beard LLC

- 6.4.14 Seven Potions Ltd

- 6.4.15 Scotch Porter LLC

- 6.4.16 Reuzel USA, Inc.

- 6.4.17 Beardilizer

- 6.4.18 Murdock London Ltd

- 6.4.19 Ranger Grooming Company

- 6.4.20 Ludovico Martelli srl (Proraso)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK