PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061910

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061910

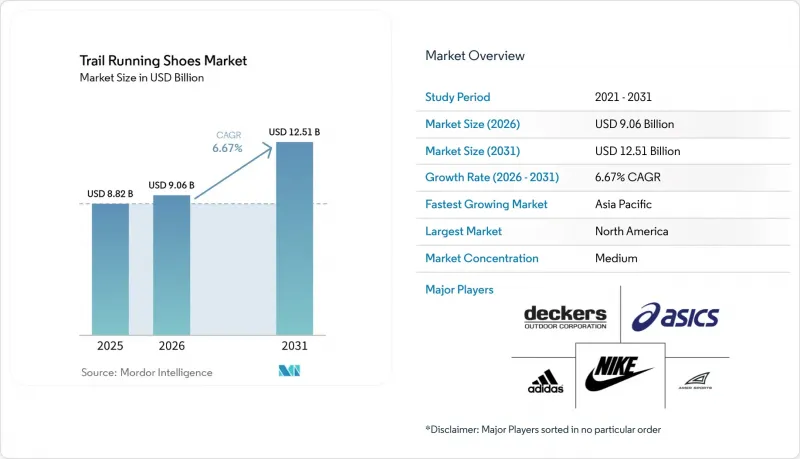

Trail Running Shoes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the trail running shoes market size is expected to increase from USD 9.06 billion in 2026 to USD 12.51 billion by 2031, growing at a CAGR of 6.67% over 2026-2031.

This report is Segmented by Product Type (Light Trail Shoes and Rugged/Technical Trail Shoes), End User (Men, Women, and Kids), Category (Mass and Premium), Distribution Channel (Online Retail Stores, Specialty Stores, Supermarkets/Hypermarkets, and Others), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Trail Running Shoes Market Trends and Insights

Rising Health-and-Wellness Focus

Health-driven motivations are reshaping the trail running demographic, drawing participants from sedentary lifestyles and road running into technical outdoor environments. In 2024, the U.S. saw 15.1 million trail running participants, marking an 8.5% year-over-year increase. Female participation rose from 51.9% to 53.2%, with Gen Z and Millennials making up the bulk of newcomers, as reported by the Sports & Fitness Industry Association. In 2025, Japan's trail running community, as noted by the Japan Trail Running Association, highlighted health improvement as a key motivator. The country is witnessing a "third wave" of growth, characterized by younger generations and an increasing number of women joining the sport. This demographic shift is significant; it alters product demands from elite-performance features to a focus on comfort, injury prevention, and adaptability for both road and trail use. Brands that incorporate cushioning, wider toe boxes, and lower drop profiles at accessible price points stand to gain the most from this wellness-focused group. In contrast, brands that remain solely race-centric may lose ground to competitors who cater to a more lifestyle-oriented audience.

Outdoor Recreation and Trail-Race Participation on the Rise

Trail racing, once a niche ultra-distance event, has evolved into a global phenomenon with multiple entry tiers, driving a consistent demand for specialized footwear. In 2025, the UTMB World Series saw 146,933 runners participate in 55 events across 28 countries, with female runners making up 30% of the total, a rise from 25% in 2022. France, as reported by European Athletics, recorded 1.44 million trail race results in 2025, marking a 150% surge over the last decade, and played host to around 6,000 trail races. China's trail racing scene has seen a meteoric rise, expanding to about 500 events in 2025, up from just 65 in 2014. This sevenfold growth has been bolstered by domestic brands like KAILAS, which boasted a wear rate surpassing 40% at major races. The International Trail Running Association highlighted a significant leap in ITRA-sanctioned events, jumping from roughly 1,300 in 2012 to over 7,000 globally in 2024. This growth underscores trail racing's organizational maturity, paving the way for sustained year-over-year participant increases. Brands that strategically sponsor event series, engage in athlete-testing feedback, and synchronize product launches with race calendars stand to gain heightened visibility and conversion rates.

Proliferation of Counterfeit and Grey-Market Products

Counterfeit trail running shoes not only undermine brand equity and erode profit margins but also expose consumers to substandard materials, heightening the risk of injuries. This situation creates both regulatory challenges and reputational damage for legitimate manufacturers. In a significant crackdown, the European Union Intellectual Property Office's Operation Fake Star II led to the seizure of over 8 million counterfeit products, resulting in 264 arrests and involving over 500 brands. Notably, footwear constituted a substantial portion of the confiscated items. In 2025, authorities at Dublin Port intercepted 9,156 counterfeit Nike pairs, with a valuation of EUR 1.6 million (around USD 1.7 million), as reported by the Revenue Commissioners of Ireland. An investigation by Indonesia's Trade Ministry uncovered a monthly import of 5,000 to 8,000 counterfeit footwear pairs and a staggering USD 392 million discrepancy in trade data. This pointed to sophisticated supply chains, tracing back to origins in Putian and Guangzhou. Furthermore, a briefing from the International Trademark Association underscored the evolution of counterfeit networks, which have now embraced advanced manufacturing techniques. This advancement complicates visual detection, prompting brands to pivot towards blockchain-based authentication, RFID tagging, and heightened consumer education initiatives. Meanwhile, the U.S. Shop Safe Act, as proposed by Congress, aims to make e-commerce platforms accountable for counterfeit listings. While this move could curtail grey-market availability, it also threatens to escalate compliance costs for online marketplaces.

Other drivers and restraints analyzed in the detailed report include:

- Continuous Innovation in Lightweight and Traction Tech

- Expansion of Online and Specialty Retail Channels

- High Average Selling Point Compared to Road-Running Footwear

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, light trail shoes dominate the trail running footwear market, capturing 63.59% of the segment revenue. These shoes are the go-to choice for newcomers to trail running, especially those transitioning from urban settings to occasional wooded trails. Priced competitively, thanks to efficient production scales, they align closely with everyday trainers, appealing to a mass-market audience. Fashion trends, notably the media-driven "gorpcore," have heightened the demand for these lightweight, urban-centric designs, leading to rapid sales turnover, particularly in cities. Capitalizing on this trend, industry players have broadened their product lines, enabling consumers to transition smoothly from lighter models to more technical ones as their running expertise grows. The light trail category thrives on its widespread appeal, value-centric offerings, and prominent visibility in both fashion and running circles.

The rugged or technical trail shoe segment is on an impressive upswing, with projections indicating a 7.08% compound annual growth rate through 2031. This growth is driven by innovations like Carbitex DFX plates and rock-shield constructions, which enhance stability and protection on rugged terrains, catering to the rising number of ultra-marathoners. High-profile events, such as the UTMB World Series, boost demand for specialized features, including advanced lug patterns and hybrid foams. Premium sub-categories in this segment, with average selling prices exceeding USD 190, boast features like water-resistant knit collars, vibration-damping plates, and 3D-printed midsoles. Investments in abrasion-resistant rubber compounds facilitate the production of exclusive limited editions, generating excitement and fostering brand loyalty among dedicated users. Collaborative designs between brands and top athletes further drive innovation, solidifying the technical segment's prominence and its pivotal role in shaping industry standards and brand value.

Trail running shoe sales are led by men, who command a 56.69% share of the market's revenue. While men still dominate sales figures, the women's segment is catching up, showing a faster year-on-year growth. Shoes designed for men often boast a diverse array of performance features and styles, appealing to both seasoned and casual runners. Marketing campaigns frequently spotlight endurance, durability, and cutting-edge technology, resonating with the brand's loyal male audience. Even with this slower growth pace, men's trail running shoes hold a robust position, spanning both entry-level and premium offerings. Given the high participation rates and deep-rooted brand loyalty among men, this segment is poised to continue its revenue dominance for the foreseeable future.

Women are rapidly emerging as a dominant force in the trail running shoes market, with their segment growing at an impressive 6.97% CAGR, outstripping the industry's overall pace. Brands are fine-tuning their products to align with female biomechanics, introducing features like wider forefoot platforms and tailored heel-to-toe drops. Marketing campaigns are increasingly showcasing female athletes conquering ultra and sub-ultra races, effectively breaking down psychological barriers and boosting participation. Retail insights reveal that women tend to replace their shoes 15% sooner than men, a trend linked to their higher mileage on varied terrains, leading to more frequent purchases. Moving away from conventional male-centric designs, brands are now offering inclusive sizing and a broader spectrum of colors. Partnerships with women's trail running groups facilitate swift feedback and innovation, while initiatives targeting younger audiences cultivate early brand loyalty. Consequently, the women's segment is on track to grow, signaling a broader market reach and bolstering the industry's resilience.

Geography Analysis

In 2025, North America accounted for 35.40% of global revenue, driven by a robust outdoor infrastructure and high discretionary spending. College-level cross-country programs are now integrating trail intervals into their training, introducing athletes to off-road footwear and fostering familiarity with trail-specific gear. According to the American Trail Running Association, nearly 48% of North American consumers run 3 to 5 times a week, highlighting a strong culture of recreational and competitive running. While proposed import tariffs introduce short-term volatility, brands are proactively diversifying their sourcing strategies by reducing reliance on single-country suppliers and expanding assembly operations within North America. These measures aim to cushion potential price shocks and maintain market stability.

Europe is witnessing a pronounced shift towards sustainability, with consumers increasingly opting for premium products that align with environmental norms. In 2024, ASICS launched its circular-design NIMBUS MIRAI shoe and the NEOCURVE sneaker, crafted from reclaimed deadstock, both making their debut in Europe. These innovations reflect the region's growing demand for eco-friendly and high-performance footwear. PUMA, capitalizing on trust built through stringent third-party certifications, has integrated 90% recycled materials into its footwear line, setting a benchmark for sustainable practices in the industry. Additionally, the alpine trail networks in France, Italy, and Switzerland are driving demand for technical footwear, especially those with advanced lug patterns tailored for diverse terrains like scree, snow, and forest paths. These networks not only support recreational activities but also attract professional athletes, further boosting the market.

Asia-Pacific is emerging as the fastest-growing region, boasting a 7.82% CAGR. Japan's Onitsuka Innovative Factory project underscores the region's dedication to high-value production and craftsmanship, facilitating agile manufacturing for limited-series trail shoes. This initiative highlights the region's focus on blending traditional expertise with modern manufacturing techniques. Urbanization, coupled with government-backed fitness initiatives like city-trail campaigns in Beijing and Seoul, is broadening access to nearby trailheads, encouraging more individuals to adopt trail running. Furthermore, cross-border e-commerce platforms are bridging the gap, enabling Asian consumers to snag new models just days after their Western launches. This streamlined access to global product releases is significantly amplifying demand and fostering a more connected consumer base.

- Amer Sports

- Decker's Outdoor Corporation

- Nike Inc

- Adidas AG (Hoka)

- ASICS Corporation

- Norda Run

- VF Corporation

- Wolverine Worldwide (Saucony)

- New Balance Athletics, Inc.

- On AG

- La Sportiva

- Inov-8

- Skechers USA, Inc

- Columbia Sportswear

- Scarpa

- Mizuno Corporation

- Under Armour

- Decathlon Lts

- Topo Athletic

- Galaxy Universal (Avia)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising health-and-wellness focus

- 4.2.2 Outdoor recreation and trail-race participation on the rise

- 4.2.3 Continuous innovation in lightweight and traction tech

- 4.2.4 Expansion of online and specialty retail channels

- 4.2.5 Shift toward eco-friendly and recycled uppers

- 4.2.6 New SKUs driven by women-centric trail communities

- 4.3 Market Restraints

- 4.3.1 Proliferation of counterfeit and grey-market products

- 4.3.2 Specialty-rubber supply volatility (e.g., Megagrip)

- 4.3.3 Concerns over injury-liability and technical terrain

- 4.3.4 High average selling point compared to road-running footwear

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 Product Type

- 5.1.1 Light Trail Running Shoes

- 5.1.2 Rugged Trail Running Shoes

- 5.2 End User

- 5.2.1 Men

- 5.2.2 Women

- 5.2.3 Kids

- 5.3 Category

- 5.3.1 Mass

- 5.3.2 Premium

- 5.4 Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Specialty Stores

- 5.4.3 Online Retail Stores

- 5.4.4 Other Distribution channels

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Sweden

- 5.5.2.7 Belgium

- 5.5.2.8 Poland

- 5.5.2.9 Netherlands

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Thailand

- 5.5.3.5 Singapore

- 5.5.3.6 Indonesia

- 5.5.3.7 South Korea

- 5.5.3.8 Australia

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Peru

- 5.5.4.5 Chile

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles

- 6.4.1 Amer Sports

- 6.4.2 Decker's Outdoor Corporation

- 6.4.3 Nike Inc

- 6.4.4 Adidas AG (Hoka)

- 6.4.5 ASICS Corporation

- 6.4.6 Norda Run

- 6.4.7 VF Corporation

- 6.4.8 Wolverine Worldwide (Saucony)

- 6.4.9 New Balance Athletics, Inc.

- 6.4.10 On AG

- 6.4.11 La Sportiva

- 6.4.12 Inov-8

- 6.4.13 Skechers USA, Inc

- 6.4.14 Columbia Sportswear

- 6.4.15 Scarpa

- 6.4.16 Mizuno Corporation

- 6.4.17 Under Armour

- 6.4.18 Decathlon Lts

- 6.4.19 Topo Athletic

- 6.4.20 Galaxy Universal (Avia)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK