PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061946

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061946

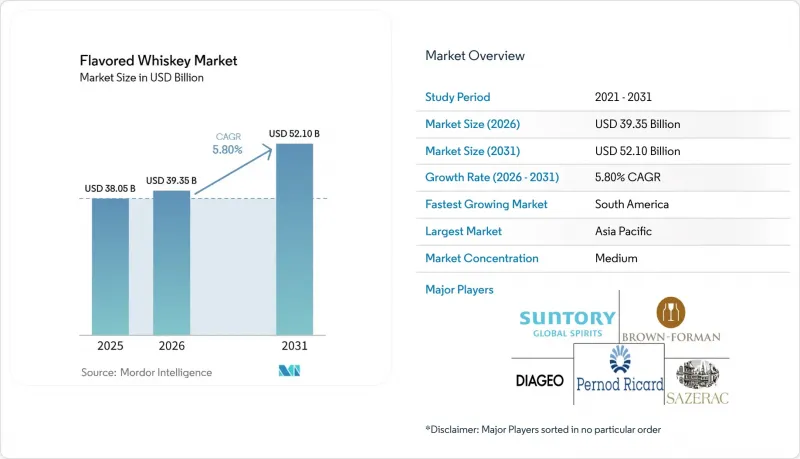

Flavored Whiskey - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the flavored whiskey market size is expected to increase from USD 38.05 billion in 2025 to USD 39.35 billion in 2026 and reach USD 52.10 billion by 2031, growing at a CAGR of 5.80% over 2026-2031.

This report is Segmented by Flavor Type (Honey, Fruity, Spiced, Botanical, Other Flavor Type), Whiskey Type (American, Canadian, Irish, Scotch, Others), End User (Men, Women), Distribution Channel (On-Trade, Off-Trade), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Global Flavored Whiskey Market Trends and Insights

Shifting Consumer Preferences Toward Innovative Flavors and Formats

Shifting consumer behaviors, increasingly linking alcohol consumption to lifestyle, identity, and sensory exploration, continue to drive the flavored whiskey market. Younger demographics, particularly Millennials and Gen Z, are prioritizing flavor experimentation over traditional brand heritage, accelerating demand for fruity, botanical, and hybrid variants. Research from the Yale School of Management highlights that purchase intent among these younger groups surges by over 20% when products are tied to social experiences, such as music festivals or summer events . In response, brands are introducing bold innovations across dessert-style, botanical, and fruit-infused expressions to capture evolving tastes. Recent launches such as Fireball's Blazin' Apple highlight how companies are leveraging familiar flavor profiles while introducing novelty to sustain consumer interest. Ready-to-drink formats are further accelerating adoption by removing preparation barriers and aligning with convenience-driven, on-the-go consumption patterns, particularly in urban markets.

Expanding Consumer Base, Including Increased Adoption Among Women

Flavored whiskey is witnessing a surge in popularity, particularly among women and first-time whiskey drinkers, who are gravitating toward smoother, fruitier, and more approachable profiles. This demographic shift is expanding the category, with flavored variants acting as gateway expressions that reduce the intensity typically associated with traditional whiskey. Brands are adopting inclusive, lifestyle-driven marketing strategies that emphasize mixability, versatility, and social consumption occasions. Honey-flavored expressions, in particular, have gained strong traction among female consumers due to their smoothness and cocktail adaptability. Products like Jack Daniel's Tennessee Honey continue to exemplify this trend, reinforcing accessibility while maintaining brand familiarity. Additionally, the rise of women-led whiskey clubs and tasting events is fostering organic advocacy and repeat purchases, especially among urban, educated consumers. This evolving consumer base is reshaping brand narratives away from heritage-focused messaging toward more experiential and inclusive positioning, strengthening long-term engagement with the flavored whiskey category.

Strong Consumer Preference for Traditional Whiskey Variants

Traditional whiskey consumers, particularly purists in bourbon, Scotch, and Irish whiskey segments, continue to resist flavored variants, viewing added flavors as a dilution of authenticity and craftsmanship. Regulatory frameworks reinforce this stance; for instance, the Scotch Whisky Association prohibits flavor additions beyond caramel coloring, effectively excluding flavored expressions from the Scotch category and strengthening the divide between tradition and innovation. This resistance is most pronounced among older, high-value consumers, creating a strategic dilemma for producers balancing growth among younger cohorts with the need to protect legacy brand equity. As a result, companies are increasingly adopting portfolio segmentation strategies, where core brands remain unflavored while separate sub-brands or extensions carry flavored offerings to minimize reputational risk. Industry signals, such as record-breaking sales of premium unflavored whiskies like Macallan and continued demand for age-statement single malts from Glenfiddich, highlight enduring loyalty to traditional expressions. This dynamic limits premiumization potential and often leads retailers to position flavored variants outside high-end categories, constraining their role primarily to casual consumption and experimentation rather than gifting or investment-grade purchases.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Experiential and Innovative Marketing Strategies

- Premiumization and Rising Demand for High-Quality Flavored Whiskies

- Health Concerns Related to Sugar Content in Flavored Whiskies

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, honey-flavored variants continue to lead the flavored whiskey segment, accounting for approximately 35.30% of total revenue. Their dominance is driven by strong consumer preference for smooth, sweet, and approachable profiles that bridge traditional whiskey with enhanced drinkability. Products like Jack Daniel's Tennessee Honey exemplify this appeal, maintaining strong traction across key markets due to their versatility and established brand equity. However, this dominance is gradually being challenged as consumer palates evolve beyond simple sweetness.

Fruity flavors are emerging as the fastest-growing segment, projected to expand at a CAGR of 7.25% through 2031. This growth is fueled by increasing demand for vibrant, cocktail-friendly profiles and innovations such as cinnamon-apple hybrids that introduce layered complexity. These offerings cater to younger consumers seeking experimentation and novelty in their drinking experiences. Meanwhile, spiced whiskeys retain a stable but mature position, while botanical variants, featuring herbal, floral, and tea-infused notes, are gaining traction among more sophisticated consumers. The "other flavors" category, including chocolate, coffee, and dessert-inspired expressions, is also expanding through limited-edition releases that drive trial and occasion-based consumption.

In 2025, American whiskey continues to dominate the flavored whiskey market, accounting for approximately 33.45% of segment revenue. This leadership is underpinned by the strong heritage of bourbon and rye, alongside the global reach of brands like Jack Daniel's and Jim Beam, which have successfully extended into flavored variants through established distribution networks and loyal consumer bases.

Irish whiskey is emerging as the fastest-growing segment, projected to expand at a CAGR of 6.10% through 2031. This growth is driven by favorable tariff structures and a global perception of Irish whiskey as smooth and approachable, qualities that align well with flavored expressions. Products such as Jameson Orange exemplify this trend, gaining traction among cocktail-oriented consumers, particularly in high-growth regions like Asia-Pacific. Scotch whisky remains constrained in the flavored segment due to regulatory restrictions from the Scotch Whisky Association, which prohibit flavor additives beyond caramel coloring, limiting its participation in this category. Meanwhile, Canadian whisky holds a stable position, supported by strong retail presence and flavored portfolios, while other categories, including Japanese, Indian, and emerging regional whiskies, represent nascent but promising opportunities driven by provenance and storytelling.

Geography Analysis

In 2025, the Asia-Pacific region leads the flavored whiskey market with a 33.10% share, driven by strong consumption growth in countries like India and China. India, in particular, stands out with rising whiskey demand and exports, while younger urban consumers increasingly favor flavored variants for their mixability and social appeal. Japan, traditionally a purist market, is gradually embracing limited-edition flavored innovations, while Southeast Asian countries such as Vietnam, Indonesia, and Thailand present high-growth opportunities due to low penetration and openness to experimentation.

South America is the fastest-growing region, projected to expand at a CAGR of 8.90% through 2031. Growth is fueled by rising disposable incomes and a cultural shift toward spirits in markets like Brazil, Argentina, and Chile. The region's relatively low resistance to flavored variants supports strong trial and adoption, although challenges such as currency volatility and distribution fragmentation persist.

North America remains a mature and significant market, supported by the dominance of American whiskey-based flavored variants, though growth is moderating due to saturation and increasing health consciousness. Europe faces regulatory and cultural constraints, particularly in traditional whiskey markets, while the Middle East and Africa represent emerging opportunities, with growth concentrated in urban centers. Overall, regional dynamics highlight the need for localized strategies that balance expansion in high-growth markets with stability in mature regions.

- Brown-Forman Corporation

- Beam Suntory Inc.

- Sazerac Company Inc.

- Diageo plc

- Pernod Ricard SA

- Bacardi Limited

- Campari Group

- Heaven Hill Brands

- William Grant & Sons Ltd

- Edrington Group Ltd

- Constellation Brands, Inc.

- MGP Ingredients, Inc.

- Remy Cointreau Group

- Buffalo Trace Distillery

- Wild Turkey Distilling Co.

- Catoctin Creek Distilling Company

- Ole Smoky Distillery

- High West Distillery

- Westward Whiskey

- New Riff Distilling

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shifting Consumer Preferences Toward Innovative Flavors and Formats

- 4.2.2 Expanding Consumer Base, Including Increased Adoption Among Women

- 4.2.3 Adoption of Experiential and Innovative Marketing Strategies

- 4.2.4 Premiumization and Rising Demand for High-Quality Flavored Whiskies

- 4.2.5 Growth of Craft and Artisanal Whiskey Segments

- 4.2.6 Increasing Integration of Flavored Whiskies in Cocktail Mixology

- 4.3 Market Restraints

- 4.3.1 Strong Consumer Preference for Traditional Whiskey Variants

- 4.3.2 Premium Pricing Constraints on Flavored Whiskey Products

- 4.3.3 Health Concerns Related to Sugar Content in Flavored Whiskies

- 4.3.4 Regulatory and Compliance Challenges Across Key Markets

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Flavor Type

- 5.1.1 Honey

- 5.1.2 Fruity

- 5.1.3 Spiced

- 5.1.4 Botanical

- 5.1.5 Other Flavor Type

- 5.2 By Whiskey Type

- 5.2.1 American

- 5.2.2 Canadian

- 5.2.3 Irish

- 5.2.4 Scotch

- 5.2.5 Others

- 5.3 By End User

- 5.3.1 Men

- 5.3.2 Women

- 5.4 By Distribution Channel

- 5.4.1 On-Trade

- 5.4.2 Off-Trade

- 5.4.2.1 Specialty/Liquor Stores

- 5.4.2.2 Other Off-Trade Stores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 France

- 5.5.2.3 United Kingdom

- 5.5.2.4 Spain

- 5.5.2.5 Netherlands

- 5.5.2.6 Italy

- 5.5.2.7 Sweden

- 5.5.2.8 Norway

- 5.5.2.9 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Vietnam

- 5.5.3.7 Indonesia

- 5.5.3.8 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Nigeria

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Brown-Forman Corporation

- 6.4.2 Beam Suntory Inc.

- 6.4.3 Sazerac Company Inc.

- 6.4.4 Diageo plc

- 6.4.5 Pernod Ricard SA

- 6.4.6 Bacardi Limited

- 6.4.7 Campari Group

- 6.4.8 Heaven Hill Brands

- 6.4.9 William Grant & Sons Ltd

- 6.4.10 Edrington Group Ltd

- 6.4.11 Constellation Brands, Inc.

- 6.4.12 MGP Ingredients, Inc.

- 6.4.13 Remy Cointreau Group

- 6.4.14 Buffalo Trace Distillery

- 6.4.15 Wild Turkey Distilling Co.

- 6.4.16 Catoctin Creek Distilling Company

- 6.4.17 Ole Smoky Distillery

- 6.4.18 High West Distillery

- 6.4.19 Westward Whiskey

- 6.4.20 New Riff Distilling

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK