PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061959

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061959

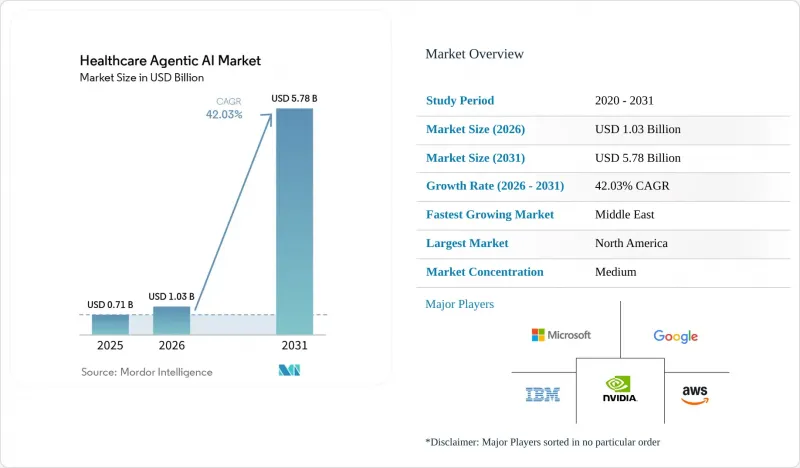

Healthcare Agentic AI - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the healthcare agentic AI market size is expected to grow from USD 0.71 billion in 2025 to USD 1.03 billion in 2026 and is forecast to reach USD 5.78 billion by 2031 at 42.03% CAGR over 2026-2031.

This report is Segmented by Offering (Platforms, and More), Deployment (On-Premise, and More), Application (Clinical Decision Support and Diagnostics, and More), End-User (Hospitals and Health Systems, and More), Technology (Large-Language-Model Agents, Multi-Modal Autonomous Agents, Reinforcement-Learning Agents, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Healthcare Agentic AI Market Trends and Insights

Rising Adoption of LLM-Based Clinical ChatGPT Tools

In 2026, health systems began integrating LLM-based clinical tools into daily workflows instead of limiting them to pilot settings. OpenAI launched OpenAI for Healthcare in January 2026, partnering with 8 leading U.S. health institutions and using GPT-5.2 models developed with input from 260 physicians across 60 countries. The April 2026 release of ChatGPT for Clinicians expanded verified access for medical users and introduced a clinical benchmark through HealthBench Professional. Major vendors, such as Microsoft, are incorporating healthcare agent orchestration into their core product roadmaps. By late 2025, Microsoft introduced healthcare-specific AI models, a Healthcare Agent Orchestrator in Microsoft Foundry, and a healthcare AI marketplace. As verified AI tools gain acceptance, agentic AI in healthcare is transitioning from innovation budgets to operational spending.

Increasing Shortage of Nursing Staff Driving Agent Assistants

Workforce pressure is driving demand for virtual nursing and task-support agents. A study using U.S. labor data projects 194,500 annual registered nurse job openings through 2033, with non-metropolitan areas potentially facing an 11% shortage by 2038. Many automated tasks, such as patient summaries and outreach coordination, are tied to nurse workflows. Mayo Clinic demonstrated scalability by deploying its AI-powered Nurse Virtual Assistant to over 9,600 nurses in inpatient and emergency units by September 2025. This practical approach allows health systems to reclaim staff time without overhauling care models, keeping hospitals invested in agentic AI despite tight capital budgets.

Data Privacy and HIPAA Compliance Complexities

Privacy requirements continue to hinder deployment despite rising demand. Agentic systems handling protected health information create multiple control points, increasing complexity, especially for multi-state health systems navigating HIPAA and state privacy laws. The growth of national interoperability infrastructure further underscores the need for governance, as broader data exchange underscores the importance of secure access controls and auditability. Consequently, the agentic AI in the healthcare market favors vendors with clear data handling rules, secure integration, and robust oversight of third-party model layers.

Other drivers and restraints analyzed in the detailed report include:

- Payer Mandates for Prior Authorization Automation

- Integration of Multi-Modal Sensing in Remote Monitoring Devices

- Algorithmic Bias Risks Leading to Regulatory Scrutiny

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software agent platforms accounted for 41.82% of the healthcare agentic AI market share in 2025, driven by their integration into EHR-linked workflows, which increases switching costs. Microsoft and Oracle have advanced healthcare AI orchestration within their enterprise stacks, boosting recurring software revenue without requiring hardware replacement. Integration services remain vital as many provider networks operate mixed EHR and imaging systems.

Edge devices and specialized hardware are expected to grow fastest in the agentic AI healthcare market, with a 42.63% CAGR through 2031, driven by the need for local inference in imaging and monitoring where cloud latency affects clinical response. Philips and NVIDIA highlighted this trend in May 2025 by collaborating on an MRI model that leveraged NVIDIA infrastructure, including MAISI and VISTA-3D, for scan planning and automated detection. This development establishes a distinct hardware layer between medical equipment and cloud software subscriptions.

Cloud-based deployment accounted for 52.38% of the healthcare agentic artificial intelligence market in 2025. That lead reflects the fact that health systems can scale new AI functions faster when they do not need heavy upfront local infrastructure. Cloud-first deployment also aligns with the commercial strategy of major platform vendors, which aim to have AI services sit within existing enterprise relationships across data, productivity, and clinical systems. On-premise models still matter in markets and institutions where data sovereignty rules and internal governance standards remain stricter than what a cloud-only setup can easily satisfy.

Hybrid edge-cloud deployments are projected to grow at a 42.58% CAGR through 2031, balancing real-time local inference for triage and monitoring with centralized model updates. CHU de Montpellier's 2026 Alliance Sante IA program, a EUR 14.9 million (USD 16.8 million) initiative, used sovereign local computing for AI deployment across 16,000 hospital professionals. National interoperability growth further supports hybrid models by enabling data coordination across sites without centralizing all inference, making hybrid architecture a key design shift in the agentic AI healthcare market.

Geography Analysis

North America accounted for 44.74% of the agentic AI market share in healthcare in 2025, driven by widespread EHR adoption, robust cloud infrastructure, and a dynamic healthcare software ecosystem. Federal policies, such as CMS's tightened prior authorization timelines and expanded interoperability, further accelerated adoption. By early 2026, HHS reported TEFCA had facilitated nearly 500 million health record exchanges, strengthening data movement for agent workflows. The region's primary challenge lies in addressing privacy, governance, and update control concerns as adoption scales.

Europe ranked second in 2025, following a compliance-driven approach emphasizing data governance, transparency, and sovereign deployment for high-risk clinical AI. The European Commission's COMPASS-AI initiative, launched in October 2025, supports the safe adoption of technologies in areas such as oncology and remote care. For instance, CHU de Montpellier is developing sovereign AI infrastructure, attracting interest from 15 additional hospital centers. Europe's market is expected to prioritize local control and audit-compliant architectures over rapid cloud-only rollouts.

The Middle East is projected to grow at a 42.89% CAGR through 2031, the fastest regional growth rate, fueled by state-backed health transformation programs integrating AI-enabled care delivery. Asia-Pacific is also emerging as a key region, with China's National Healthcare Security Administration launching the Personal Medical Insurance Cloud initiative in March 2026 to integrate data for 1.33 billion insured individuals. Workforce pressures, telehealth expansion, and large public digital programs are driving adoption in both regions.

- Microsoft Corporation

- Google LLC

- Amazon.com, Inc.

- IBM Corporation

- NVIDIA Corporation

- Oracle Corporation

- GE HealthCare Technologies Inc.

- Siemens Healthineers AG

- Koninklijke Philips N.V.

- Epic Systems Corporation

- Cerner Corporation

- Nuance Communications, Inc.

- Medtronic plc

- Intuitive Surgical, Inc.

- Tempus Labs, Inc.

- PathAI, Inc.

- Butterfly Network, Inc.

- Viz.ai, Inc.

- Insilico Medicine, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of LLM-Based Clinical ChatGPT Tools

- 4.2.2 Increasing Shortage of Nursing Staff Driving Agent Assistants

- 4.2.3 Payer Mandates for Prior Authorization Automation

- 4.2.4 Integration of Multi-Modal Sensing in Remote Monitoring Devices

- 4.2.5 Shift Toward Value-Based Care Incentivizing Automation

- 4.2.6 Venture Capital Funding Surge in Healthcare Agentic Start-ups

- 4.3 Market Restraints

- 4.3.1 Data Privacy and HIPAA Compliance Complexities

- 4.3.2 Algorithmic Bias Risks Leading to Regulatory Scrutiny

- 4.3.3 Lack of Standardized Interoperability Frameworks

- 4.3.4 Limited Clinical Validation Evidence for Autonomous Agents

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Software Agent Platforms

- 5.1.2 Integration and Customization Services

- 5.1.3 Edge Devices and Specialized Hardware

- 5.2 By Deployment Mode

- 5.2.1 Cloud-based

- 5.2.2 On-premise

- 5.2.3 Hybrid

- 5.3 By Application

- 5.3.1 Clinical Decision Support and Diagnostics

- 5.3.2 Patient Engagement and Virtual Nursing

- 5.3.3 Operational and Administrative Automation

- 5.3.4 Drug Discovery and Research

- 5.3.5 Remote Monitoring and Tele-health

- 5.4 By End-User

- 5.4.1 Hospitals and Health Systems

- 5.4.2 Ambulatory / Specialty Clinics

- 5.4.3 Payers and Insurance

- 5.4.4 Pharmaceutical and Biotech Companies

- 5.4.5 Patients (Direct-to-Consumer)

- 5.5 By Technology

- 5.5.1 Large-Language-Model Agents

- 5.5.2 Multi-Modal Autonomous Agents

- 5.5.3 Reinforcement-Learning Agents

- 5.5.4 Rule-based / Expert Agents

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Microsoft Corporation

- 6.4.2 Google LLC

- 6.4.3 Amazon.com, Inc.

- 6.4.4 IBM Corporation

- 6.4.5 NVIDIA Corporation

- 6.4.6 Oracle Corporation

- 6.4.7 GE HealthCare Technologies Inc.

- 6.4.8 Siemens Healthineers AG

- 6.4.9 Koninklijke Philips N.V.

- 6.4.10 Epic Systems Corporation

- 6.4.11 Cerner Corporation

- 6.4.12 Nuance Communications, Inc.

- 6.4.13 Medtronic plc

- 6.4.14 Intuitive Surgical, Inc.

- 6.4.15 Tempus Labs, Inc.

- 6.4.16 PathAI, Inc.

- 6.4.17 Butterfly Network, Inc.

- 6.4.18 Viz.ai, Inc.

- 6.4.19 Insilico Medicine, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment