PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061962

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061962

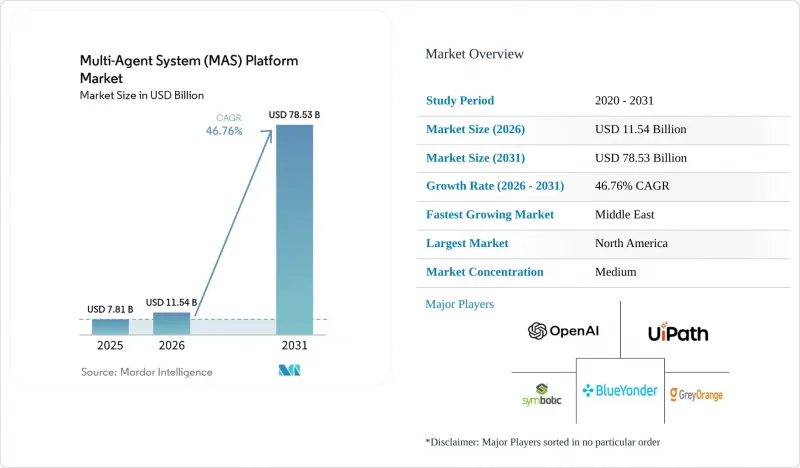

Multi-Agent System (MAS) Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the multi-agent system platform market size is projected to expand from USD 7.81 billion in 2025 and USD 11.54 billion in 2026 to USD 78.53 billion by 2031, registering a CAGR of 46.76% between 2026 and 2031.

This report is Segmented by Platform Type (Agent-Development Frameworks, Orchestration Platforms, Simulation and Digital-Twin Suites, and More), Deployment Mode (Cloud, and On-Premises/Edge), End-Use Industry (Manufacturing, Supply-Chain and Logistics, and More), Application (Workflow and Process Orchestration, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Multi-Agent System (MAS) Platform Market Trends and Insights

Cloud-Native Multi-Agent System Deployment Boom

Kubernetes-compatible orchestration platforms let developers scale from dozens to thousands of agents without rewriting infrastructure. Microsoft's AutoGen and LangGraph Cloud, both launched in 2025, introduced declarative templates that turn YAML descriptions into running clusters. Elastic compute and managed networking shorten proof-of-concept cycles, while hyperscalers bundle discounted inference accelerators that lock customers into their ecosystems. Financial institutions and logistics operators report faster time-to-value once cluster management is offloaded, reinforcing the positive feedback loop that is lifting the multi-agent system platform market.

Warehouse-Automation Demand for Multi-Robot Orchestration

Fulfillment centers now optimize fleet-level productivity rather than individual robot features. Locus Robotics coordinates more than 6,000 autonomous mobile robots across 300 warehouses, cutting order-cycle time by 25% compared with manual picking. Symbotic earned USD 593.3 million from 42 Walmart distribution centers in fiscal 2024, underlining commercial willingness to invest when orchestration delivers double-digit throughput gains. Edge-resident agents avoid cloud latency, and simulation-based pretraining accelerates commissioning, positioning warehouse automation as a durable growth driver.

Scarcity of Multi-Agent-System-Ready Talent and Standards

LinkedIn's 2025 AI Talent Gap Report showed that 68% of enterprises struggle to hire engineers skilled in inter-agent communication and distributed reinforcement learning, stretching median recruitment cycles past 90 days. Fragmented standards complicate onboarding because vendors must support multiple ontologies, while global professional development pipelines lag behind demand. The shortfall inflates salaries and extends implementation timelines, slowing adoption.

Other drivers and restraints analyzed in the detailed report include:

- Convergence of Large-Language-Model-Based Agents and Reinforcement-Learning Frameworks

- Declining Edge-AI Costs Enabling On-Device Agents

- Expanded Cyber-Security Attack Surface at Agent Level

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Autonomous-agent software-as-a-service offerings are forecast to grow at 47.37% between 2026 and 2031. This significant growth reflects the increasing buyer preference for turnkey subscription models that simplify the complexities of distributed systems. These models are driving the multi-agent system platform market size for SaaS well above historical norms, as businesses seek scalable and efficient solutions. Orchestration platforms, which maintained a 34.63% revenue share in 2025, highlight the strong position of incumbents among vendors that provide reliability, durability, and exactly-once execution capabilities.

Pure-play frameworks continue to attract engineering-led organizations due to their flexibility and customization potential. However, the steep learning curve associated with consensus mechanisms and failure detection has limited their broader adoption. Simulation suites, such as NVIDIA Omniverse, achieved a USD 1 billion annual run rate in fiscal 2025, emphasizing the growing demand for virtual validation of policies before physical deployment. This trend underscores the importance of simulation in reducing risks and optimizing performance in real-world applications. Competitive pressure from enterprise-software incumbents bundling agents into CRM and ERP suites is expected to compress standalone platform margins. Nevertheless, vertical specialization and tailored solutions can help mitigate the effects of commoditization, enabling vendors to maintain a competitive edge.

Cloud retained 72.58% of the revenue share in 2025, primarily due to its ability to scale elastically and simplify operations. This dominance highlights the growing preference for cloud-based solutions in the multi-agent system platform market. However, on-premises and edge configurations are projected to achieve a significant compound annual growth rate (CAGR) of 47.21% through 2031. This rapid growth is expected to narrow the market share gap between cloud and other configurations. The increasing adoption of on-premises and edge solutions is driven by the need for localized data processing, particularly among manufacturers and hospitals. These entities aim to comply with stringent data protection regulations, such as the European Union's General Data Protection Regulation (GDPR), which imposes penalties for cross-border data transfers.

Advancements in technology, such as quantized models and cost-effective inference chips, have enabled robots, point-of-sale devices, and industrial sensors to operate agents at a significantly reduced cost-less than one cent per million tokens. This affordability has expanded the accessibility of multi-agent systems across various industries. Additionally, hybrid topologies that combine on-device perception loops with cloud-based planning synchronization offer substantial latency benefits while maintaining centralized oversight. These hybrid systems are particularly advantageous for applications requiring real-time decision-making and operational efficiency. To support such deployments, platforms like Microsoft Azure IoT Edge and AWS Greengrass have introduced orchestration extensions. These enhancements simplify the management of split deployments, ensuring seamless integration between edge devices and cloud infrastructure.

Geography Analysis

North America captured 41.38% of 2025 revenue, driven by hyperscaler product launches and early adoption in logistics and finance. OpenAI and AWS's USD 38 billion infrastructure partnership underscores regional commitment to scaling hybrid-agent workloads. Additionally, the U.S. defense programs that coordinate autonomous vehicles and logistics chains have further legitimized the technology for commercial buyers, encouraging broader adoption across industries. Europe emphasizes data sovereignty and algorithmic transparency, with automotive and industrial automation leaders in Germany piloting agent-based scheduling systems that align with the AI Act. GDPR limitations are also fueling demand for localized deployments, as businesses seek to comply with stringent data protection regulations. Government funding initiatives and university-led research projects continue to drive innovation in the region, ensuring a steady contribution to the overall growth of the multi-agent system platform market.

The Middle East is forecast to record the fastest regional CAGR at 47.11% between 2026 and 2031. Large-scale projects like Saudi Arabia's NEOM and the United Arab Emirates' Dubai Digital Twin are integrating agents for energy management, mobility, and waste management. Sovereign wealth funds in the region are not only supplying capital but also mandating cutting-edge sustainability targets, creating a fertile environment for vendors to innovate and expand. Asia-Pacific benefits from China's significant investments in smart-city infrastructure, Japan's well-established robotics industry, and India's abundant software development talent.

Singapore's agent-driven eco-district serves as a performance benchmark for regional planners, showcasing the potential of agent-based systems in urban development. South America and Africa, while smaller markets today, are demonstrating early adoption in sectors such as mining, agriculture, and telecommunications. In these regions, agents are being used to optimize resource allocation and improve operational efficiency, even in areas with limited infrastructure, highlighting their adaptability and growth potential.

- OpenAI LLC

- UiPath Inc.

- GreyOrange Inc.

- C3.ai Inc.

- Fetch.ai Foundation Pte Ltd.

- Mindsmiths d.o.o.

- CrewAI Inc.

- Swarms AI Inc.

- HASH.ai Ltd.

- Algovera DAO Ltd.

- Emergence AI Inc.

- AgentVerse Technologies Ltd.

- Temporal Technologies Inc.

- Instadeep Ltd.

- Locus Robotics Corp.

- Blue Yonder Group Inc.

- Manus AI

- Onomatic LLC

- Softeon Inc.

- Symbotic Inc.

- Camunda Services GmbH

- Airt Inc.

- Relevance AI Pty Ltd.

- Anthropic P.B.C.

- Cognizant Technology Solutions Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-Native MAS Deployment Boom

- 4.2.2 Warehouse-Automation Demand for Multi-Robot Orchestration

- 4.2.3 Convergence of LLM-Based Agents and Reinforcement-Learning Frameworks

- 4.2.4 Declining Edge-AI Costs Enabling On-Device Agents

- 4.2.5 Token-Incentivised Open MAS Protocols

- 4.2.6 Emergence of Agent-Alignment Toolkits for Safety-Critical Industries

- 4.3 Market Restraints

- 4.3.1 Scarcity of MAS-Ready Talent and Standards

- 4.3.2 Expanded Cyber-Security Attack Surface at Agent Level

- 4.3.3 GPU and Inference-Chip Supply-Chain Volatility

- 4.3.4 Energy-Efficiency Pressure from ESG Investors

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE & GROWTH FORECASTS (VALUE)

- 5.1 By Platform Type

- 5.1.1 Agent-Development Frameworks

- 5.1.2 Orchestration Platforms

- 5.1.3 Simulation and Digital-Twin Suites

- 5.1.4 Autonomous-Agent SaaS

- 5.1.5 Other Platform Type

- 5.2 By Deployment Mode

- 5.2.1 Cloud

- 5.2.2 On-Premises / Edge

- 5.3 By End-Use Industry

- 5.3.1 Manufacturing

- 5.3.2 Supply-Chain and Logistics

- 5.3.3 Healthcare and Life-Sciences

- 5.3.4 BFSI

- 5.3.5 Smart Cities and Infrastructure

- 5.4 By Application

- 5.4.1 Workflow and Process Orchestration

- 5.4.2 Multi-Robot Coordination

- 5.4.3 Decision-Support and Planning

- 5.4.4 Simulation and Digital-Twin Modelling

- 5.4.5 Autonomous Trading and Fin-Ops

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Qatar

- 5.5.5.5 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 OpenAI LLC

- 6.4.2 UiPath Inc.

- 6.4.3 GreyOrange Inc.

- 6.4.4 C3.ai Inc.

- 6.4.5 Fetch.ai Foundation Pte Ltd.

- 6.4.6 Mindsmiths d.o.o.

- 6.4.7 CrewAI Inc.

- 6.4.8 Swarms AI Inc.

- 6.4.9 HASH.ai Ltd.

- 6.4.10 Algovera DAO Ltd.

- 6.4.11 Emergence AI Inc.

- 6.4.12 AgentVerse Technologies Ltd.

- 6.4.13 Temporal Technologies Inc.

- 6.4.14 Instadeep Ltd.

- 6.4.15 Locus Robotics Corp.

- 6.4.16 Blue Yonder Group Inc.

- 6.4.17 Manus AI

- 6.4.18 Onomatic LLC

- 6.4.19 Softeon Inc.

- 6.4.20 Symbotic Inc.

- 6.4.21 Camunda Services GmbH

- 6.4.22 Airt Inc.

- 6.4.23 Relevance AI Pty Ltd.

- 6.4.24 Anthropic P.B.C.

- 6.4.25 Cognizant Technology Solutions Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment