PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061996

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2061996

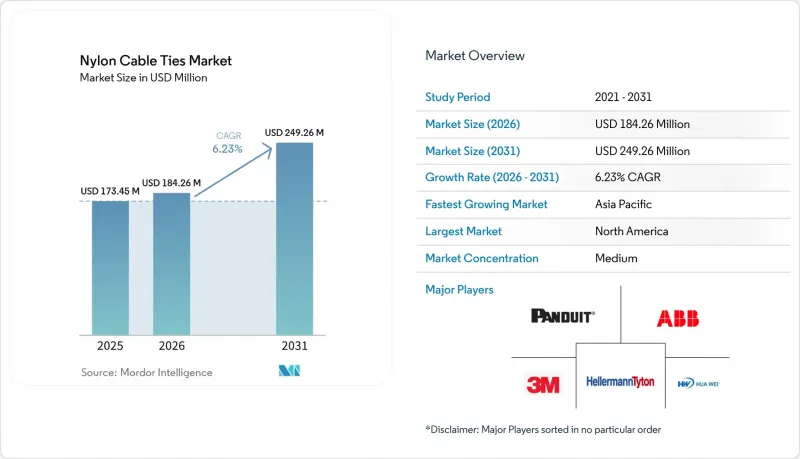

Nylon Cable Ties - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

According to Mordor Intelligence, the nylon cable ties market size is expected to grow from USD 173.45 million in 2025 to USD 184.26 million in 2026 and is forecast to reach USD 249.26 million by 2031 at 6.23% CAGR over 2026-2031.

This report is Segmented by Type (Nylon 6, Nylon 6, 6, and Others), Application (Electrical and Electronics, Automotive, and Construction, and More), Distribution Channel (Direct Sales, Distributors/Wholesalers, and Online Retail/E-Commerce), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Nylon Cable Ties Market Trends and Insights

Expansion of Global Construction and Infrastructure Pipelines

Megaprojects across Asia-Pacific and the Middle East continue to specify large volumes of ties for electrical runs in transit systems, commercial towers, and utility grids. India's National Infrastructure Pipeline targets USD 1.4 trillion of spend through 2025, creating sustained pull for commodity grades while rewarding suppliers that can stage inventory near job sites. China's Belt and Road contractors procure ties for export builds in Southeast Asia and Africa, extending price competition beyond domestic markets. Demand often arrives in surges, forcing manufacturers to balance overtime production with the risk of post-project inventory corrections. Distributors respond by shortening purchase commitments, which raises working-capital requirements for converters. The net effect is a structurally higher safety-stock level at plants serving project business.

Rising Uptake in Electric Vehicle Wire-Harness Assemblies

Battery-electric cars require 30%-50% more ties than internal-combustion models because high-voltage cabling, sensor looms, and coolant lines occupy greater real estate. Harnesses run at 600 V to 1,000 V and heat components beyond 150°C, so automakers insist on Nylon 6,6 ties that pass ISO 19642 thermal-aging tests up to 12,000 hours. HellermannTyton's swivel mount, introduced in February 2025, rotates 360 degrees, easing routing around moving parts without overstressing the tie. Tier-1 harness makers such as Yazaki and Aptiv consolidate supplier lists to ensure traceability and RoHS compliance, which tightens entry conditions for regional converters. As global EV output scales, tie suppliers able to certify materials for continuous 175°C exposure enjoy premium pricing and multiyear volume contracts.

Availability of Reusable Alternative Fastening Systems

Hook-and-loop products such as VELCRO ONE-WRAP capture share in data centers and consumer electronics where cables move often, and landfill costs weigh on purchasing mandates. Operators report 40% lower consumable spending across a three-year refresh cycle, even though reusable ties carry higher upfront prices. Color coding, adjustability, and the absence of sharp cut tails improve worker ergonomics and equipment safety. Nylon ties retain primacy in high-vibration or high-temperature environments such as under-hood automotive, yet the volume shift toward reusables in light-duty applications trims baseline growth for single-use nylon.

Other drivers and restraints analyzed in the detailed report include:

- Cost-Effective and Easy-Install Versus Metallic Fasteners

- Offshore Wind and Solar Farms Need UV/Weather-Resistant Ties

- Feedstock Price Volatility for Caprolactam and Adipic Acid

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cost-focused builders still favor Nylon 6 for indoor wiring where ambient temperatures stay below 85°C. High-volume SKUs for consumer devices, lighting fixtures, and residential panels keep Nylon 6 in the lead at 45.23% of 2025 revenue. Specialty blends and bio-based formulations occupy a niche but attract research and development spend as brands chase low-carbon materials. Regulatory moves against halogenated flame retardants accelerate the pivot to phosphorus-based systems, raising formulation complexity and rewarding compounders with accredited labs.

Nylon 6,6 accounted for a smaller share than Nylon 6 in 2025, yet is projected to grow at a 6.97% CAGR through 2031. The Nylon cable ties market size for Nylon 6,6 is forecast to climb as under-hood EV temperatures demand continuous service to 175°C. OEM engineering standards such as QC/T 1037 require thermal aging that Nylon 6 often cannot pass without additives, steering specifications toward Nylon 6,6. Recycled grades introduced by HellermannTyton in October 2024 combine circular-economy credentials with tensile strengths up to 535 N, commanding a 10%-15% premium over virgin material.

Geography Analysis

North America maintained 25.32% of 2025 revenue owing to data-center construction in Virginia, Texas, and Oregon, plus EV ramps in Michigan and Mexico. Operators increasingly specify RFID-enabled ties for real-time tracking, a niche that local suppliers fill with short lead times. Caprolactam price volatility and Asian import competition squeeze margins, pushing converters toward feedstock integration. Canadian offshore wind pilots call for marine-grade stainless ties that satisfy DNV and UL 62275 rules.

Asia-Pacific leads growth at 7.32% CAGR through 2031, powered by China's integrated caprolactam capacity and India's infrastructure push. Chinese converters undercut Western prices on commodity grades, yet domestic brands also move upscale with RFID-ready and UV-resistant lines as export users demand certifications. India's metro and highway expansions consume bulk packs, but price sensitivity slows adoption of premium formulations. Japan and South Korea favor certified materials for automotive exports, reinforcing regional demand for Nylon 6,6. Southeast Asian nations such as Vietnam attract harness production relocations, supporting local stocking models.

Europe grows more slowly because natural-gas and electricity prices remain elevated post-2022, lifting polymerization costs. Buyers import more Asian resin and semi-finished ties, although stringent sustainability agendas spur interest in post-industrial recycled Nylon 6,6. North Sea wind farms, data centers in Ireland and the Nordics, and German automotive wire harnesses still anchor demand for high-spec grades. South America and Middle East-Africa remain small but gain momentum from Brazilian automation investment and Saudi Arabia's NEOM project, where UV-stable and high-temperature certifications are mandatory despite tight budgets.

- 3M

- ABB Ltd

- Advanced Cable Ties Inc.

- AFT Fasteners

- Ascend Performance Materials

- Avery Dennison Corporation

- Cablecraft Motion Controls

- Essentra plc

- HellermannTyton Group

- Hogert Technik

- HUA WEI INDUSTRIAL CO., LTD.

- KAI SUH SUH ENTERPRIES CO., LTD

- Panduit Corporation

- SapiSelco s.r.l.

- Southwire Company, LLC.

- TE Connectivity

- Weidmuller Interface

- Yueqing Huada Plastic Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of global construction and infrastructure pipelines

- 4.2.2 Rising uptake in Electric vehicle wire-harness assemblies

- 4.2.3 Cost-effective and easy-install versus metallic fasteners

- 4.2.4 Offshore wind and solar farms need UV/weather-resistant ties

- 4.2.5 Adoption of RFID-enabled smart ties for predictive maintenance

- 4.3 Market Restraints

- 4.3.1 Availability of reusable/alternative fastening systems

- 4.3.2 Feedstock price volatility (caprolactam and adipic acid)

- 4.3.3 Migration to automated harness-wrapping robots reducing tie consumption

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Nylon 6

- 5.1.2 Nylon 6,6

- 5.1.3 Others

- 5.2 By Application

- 5.2.1 Electrical and Electronics

- 5.2.1.1 Consumer Electronics Wiring

- 5.2.1.2 Data-centre Cabling

- 5.2.2 Automotive

- 5.2.2.1 ICE Vehicles

- 5.2.2.2 Electric Vehicles

- 5.2.3 Construction

- 5.2.3.1 Commercial Buildings

- 5.2.3.2 Residential Buildings

- 5.2.4 Industrial Manufacturing

- 5.2.5 Consumer Goods and DIY

- 5.2.6 Renewable Energy Installations

- 5.2.7 Others

- 5.2.1 Electrical and Electronics

- 5.3 By Distribution Channel

- 5.3.1 Distributors/Wholesalers

- 5.3.2 Direct Sales

- 5.3.3 Online Retail/E-Commerce

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 ABB Ltd

- 6.4.3 Advanced Cable Ties Inc.

- 6.4.4 AFT Fasteners

- 6.4.5 Ascend Performance Materials

- 6.4.6 Avery Dennison Corporation

- 6.4.7 Cablecraft Motion Controls

- 6.4.8 Essentra plc

- 6.4.9 HellermannTyton Group

- 6.4.10 Hogert Technik

- 6.4.11 HUA WEI INDUSTRIAL CO., LTD.

- 6.4.12 KAI SUH SUH ENTERPRIES CO., LTD

- 6.4.13 Panduit Corporation

- 6.4.14 SapiSelco s.r.l.

- 6.4.15 Southwire Company, LLC.

- 6.4.16 TE Connectivity

- 6.4.17 Weidmuller Interface

- 6.4.18 Yueqing Huada Plastic Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs